Fed ‘Dots’ Signal Major Dovish Pivot For Election Year

Tl;dr: Powell “pivoted”.

Instead of the old mantra of “don’t fight The Fed”, it appears The Fed’s new mantra is “don’t fight the market” as the Dot Plot adjusted down significantly more dovishly than expected, narrowing the gap to the market’s expectation significantly…

{kind=link}

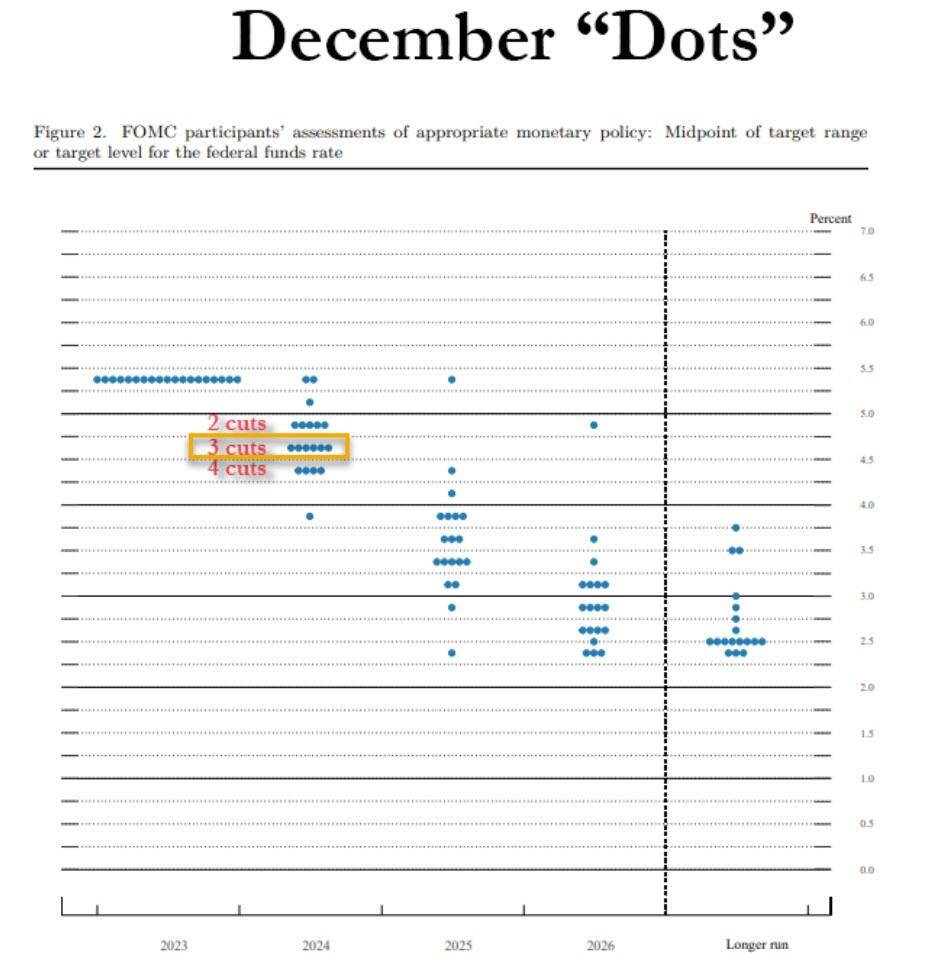

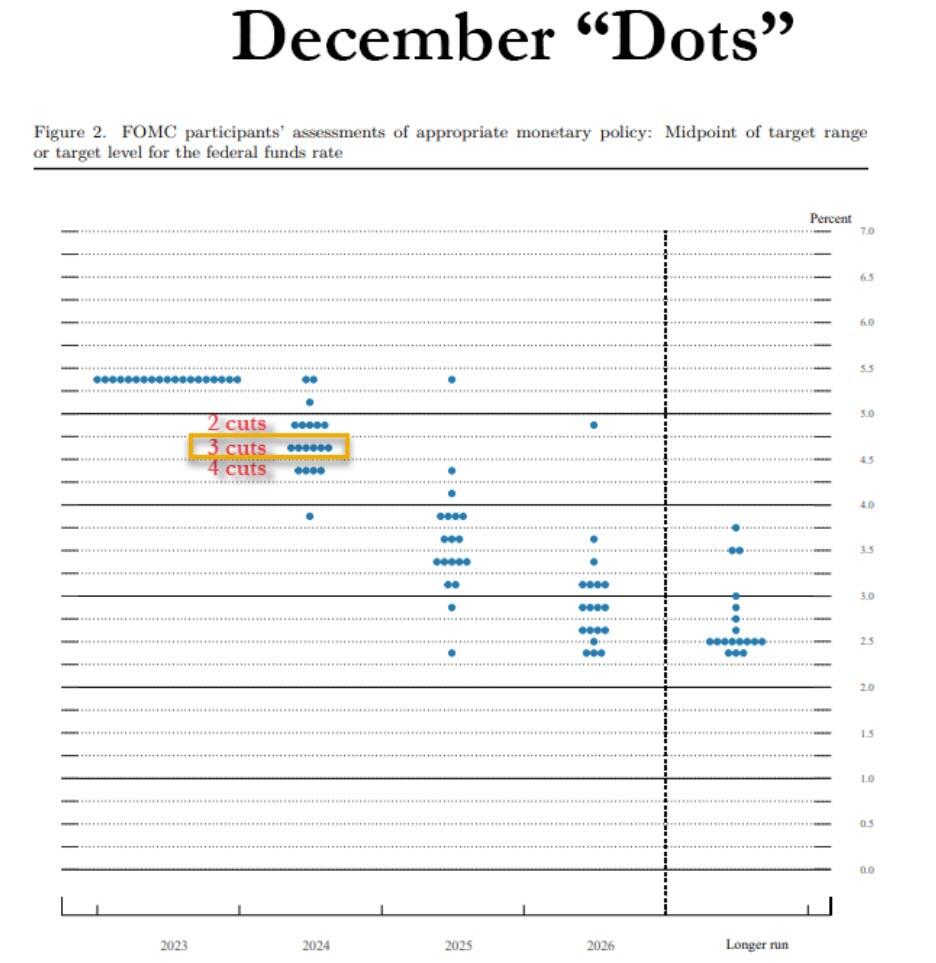

Median assessment of appropriate pace of policy:

2023 5.375% (range 5.375% to 5.375%); prior 5.625%

2024 4.625% (range 3.875% to 5.375%); prior 5.125%

2025 3.625% (range 2.375% to 5.375%); prior 3.875%

2026 2.875% (range 2.375% to 4.875%); prior 2.875%

Here’s what’s odd:

In Sept, Fed saw 2 cuts in 2024, 5 cuts in 2025

Now, Fed sees 3 cuts in 2024, 4 cuts in 2025

Put another way:

In Sept, 5 Fed members expected three cuts or more

In Dec, 11 Fed members expect three cuts or more.

{kind=link}

So, is The Fed frontloading (in an election year) at the expense of 2025?

Will Powell unleash the hawknado?

* * *

Since The Fed’s last meeting (on Nov 1st), the markets have been extreme to say the least. The dollar (and gold) are lower as Bitcoin has soared higher and stocks and bonds both surged…

{kind=link}

Source: Bloomberg

For context, that 9%-plus rally in the S&P 500 is the best inter-meeting performance since June-August 2009.

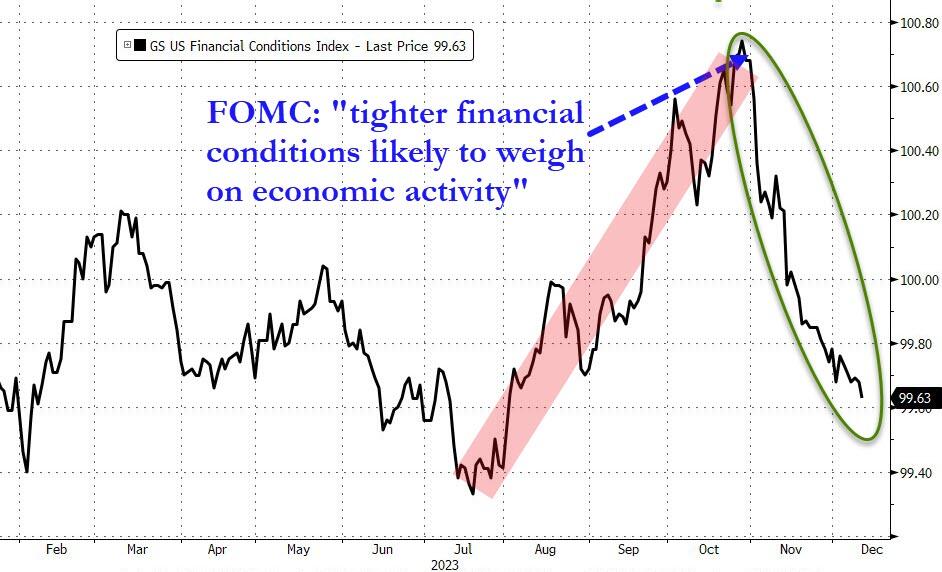

Even more extreme is the fact that the rally in bonds and stocks and decline in the dollar has sparked an almost unprecedented easing of financial conditions since Nov 1st.

{kind=link}

Source: Bloomberg

This is particularly noteworthy because The Fed explicitly mentioned the fact that “Tighter financial… conditions…are likely to weigh on economic activity, hiring, and inflation” with the ‘the market is doing The Fed’s job for it’ narrative being espoused by all.

Well, all that good work by The Fed has now been undone!

And with its usual lag, the previous tightening appears to have indeed weighed down macro data…

{kind=link}

Source: Bloomberg

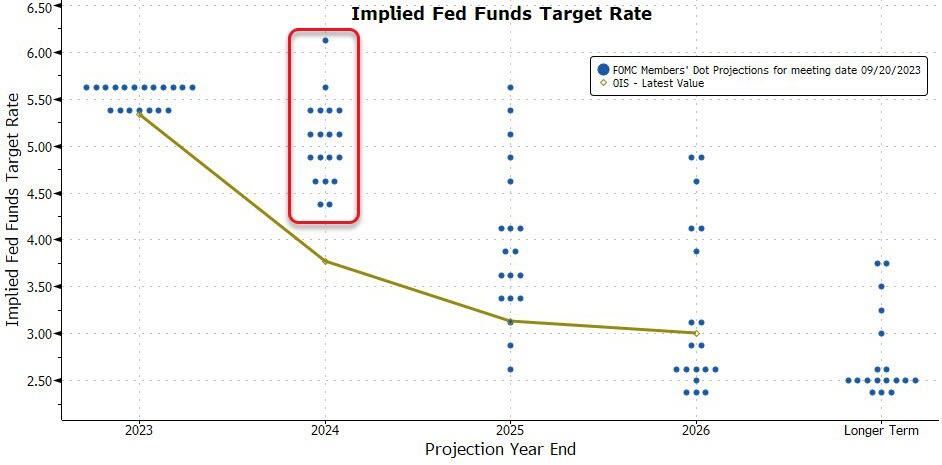

The market has pushed dramatically more dovish, pricing in 125bps of rate-cuts next year (from around 75bps at the last Fed meeting)…

{kind=link}

Source: Bloomberg

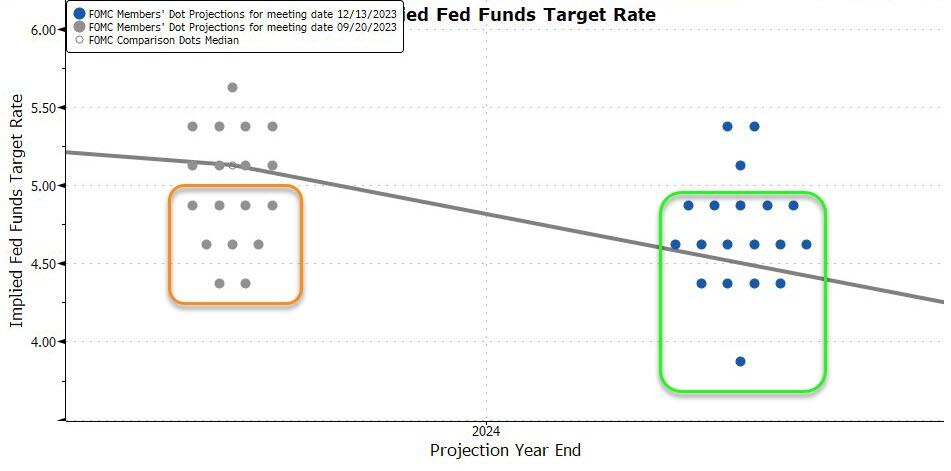

And, as we have been highlighting, this means the market is now pricing in an expectation that every single member of The Fed is wrong (too hawkish) about rates next year…

{kind=link}

Source: Bloomberg

Which leads us to the crux of today’s FOMC statement and press conference, which is – just how much will they (hawkishly) push back against the easing of financial conditions or (dovishly) adjust their dots to meet the market’s demand?

As Mohamed El-Erian noted just ahead of the statement:

Fascinating to see markets push yields further down ahead of this afternoon’s announcement/remarks.

Either they are comfortable that there will be a January 2019 repeat or are bluntly ignoring the longstanding mantra of “don’t fight the Fed”.

And so, what did we get?

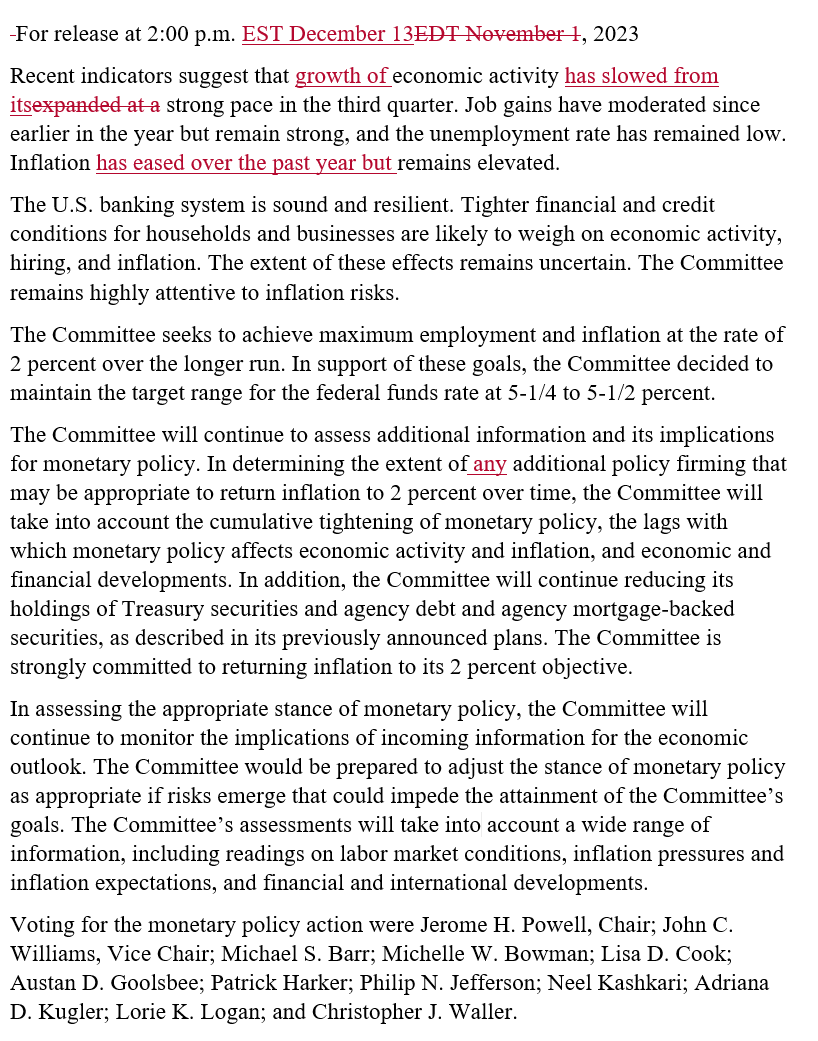

No change in policy rates as fully expected – the third consecutive meeting in this “temporary pause.”

But, then unleashed the doves in the statement:

FOMC softens stance toward further hikes by adding one word to the statement, saying officials will consider the extent of “any” additional policy firming that’s needed

Fed also acknowledges that “inflation has eased over the past year but remains elevated,” and says that economic growth has slowed from the third quarter’s “strong pace”

The dots went uber-dovish, with the median dots calling for 3 cuts, up from 2 cuts before.

Sept dots median 2024 dot was 5.1%

Dec dots median 2024 dot is 4.6%

{kind=link}

There are 5 Fed officials below that media point (seeing 100bps of cuts)…

{kind=link}

Median assessment of appropriate pace of policy:

2023 5.375% (range 5.375% to 5.375%); prior 5.625%

2024 4.625% (range 3.875% to 5.375%); prior 5.125%

2025 3.625% (range 2.375% to 5.375%); prior 3.875%

2026 2.875% (range 2.375% to 4.875%); prior 2.875%

Additionally, median projections for inflation tick down in 2024 and 2025, while unemployment forecasts are little changed, indicating Fed officials’ growing confidence they can cool price gains without big job losses.

And now we wait for Powell’s presser, which UBS wittily described as follows:

“The meeting will be followed by Fed Chair Powell delivering the full benefit of his economic insight at the press briefing (this should not take long).

Powell will try to prevent markets from expecting earlier rate reductions.

This task would be a lot easier had Powell not trashed the Fed’s reputation for forward guidance.”

Harsh but fair.

* * *

Read the full redline below:

{kind=link}

Tyler Durden

Wed, 12/13/2023 – 14:05