Amazon Reverses 7% After Hours Plunge Despite Cloud Miss, Ugly Guidance

Ahead of Amazon’s earnings, UBS said that the online retailer is the “cleanest Mag7 name to own”, although in retrospect it may also be the cleanest Ma7 name to sell, which is what is taking place after hours when the stock tumbled after it missed on Q4 cloud revenue and also guided well below estimates.

First, here is a big picture of what the company reported for the just concluded 4th quarter:

EPS $1.86 vs. $1.43 q/q, beatingestimates of $1.50

Net sales $187.79 billion, +10% y/y, beatingestimates of $187.32 billion

Online stores net sales $75.56 billion, +7.1% y/y, beatingestimates of $74.71 billion

Physical Stores net sales $5.58 billion, +8.3% y/y, beatingestimates of $5.4 billion

Subscription Services net sales $11.51 billion, +9.7% y/y, missingestimates of $11.58 billion

Subscription services net sales excluding F/X +10% vs. +13% y/y, estimate +10.3%

North America net sales $115.59 billion, +9.5% y/y, beatingestimates of $114.27 billion

International net sales $43.42 billion, +7.9% y/y, beatingestimates of $44.13 billion

Third-Party Seller Services net sales $47.49 billion, +9% y/y, missingestimates of $48.02 billion

Third-party seller services net sales excluding F/X +9% vs. +19% y/y, estimate +10.2%

So far so good (with some exceptions). But where the market was disappointed was in Amazon’s AWS revenue, which missed estimates modestly:

AWS net sales $28.79 billion, +19% y/y, estimate $28.82 billion

Amazon Web Services net sales excluding F/X +19% vs. +13% y/y, estimate +19%

Turning to operating results:

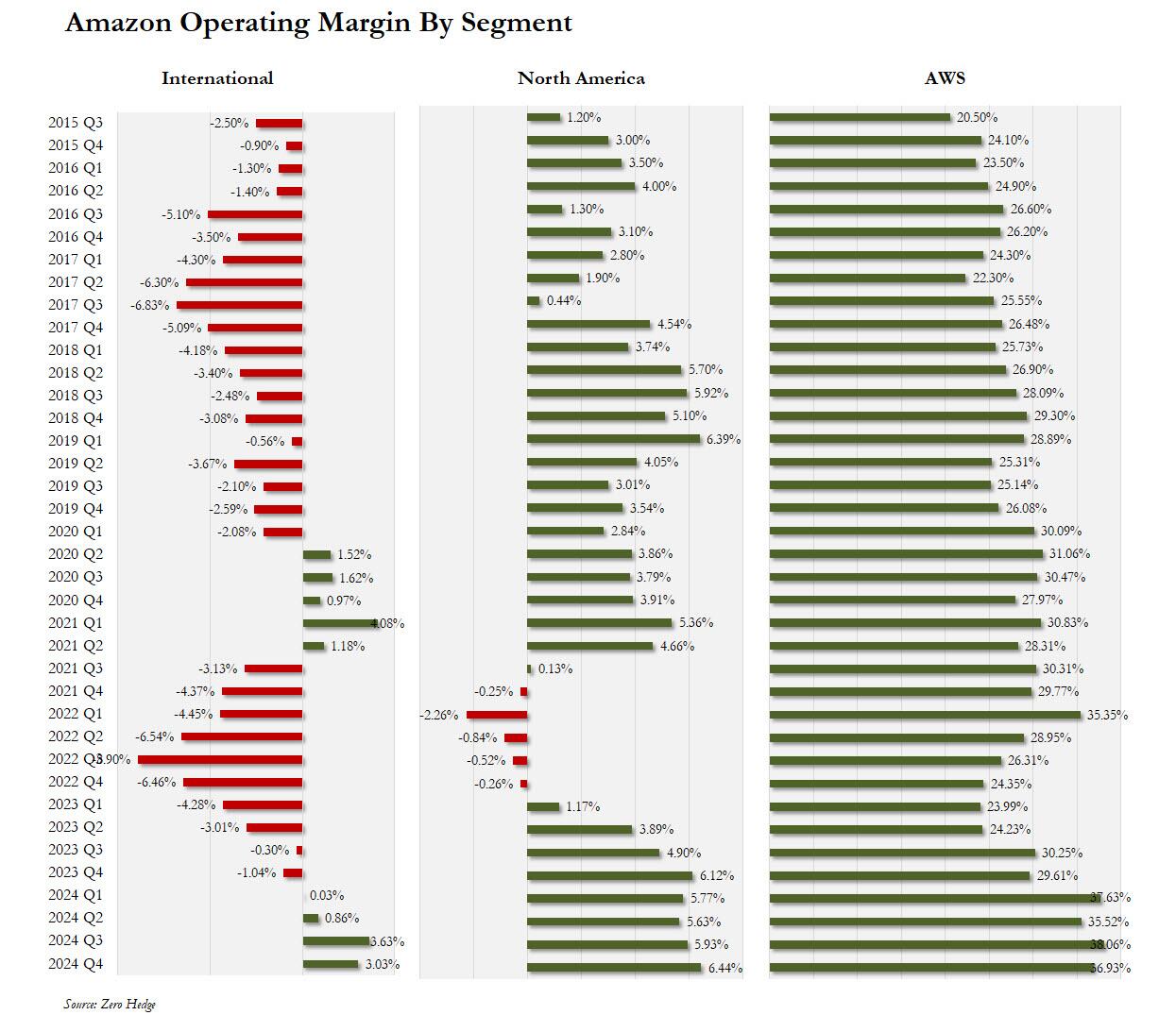

AWS operating profit 36.9%, down from 38.1% but beatingestimates of 34.7%

Operating income $21.20 billion, +61% y/y, beatingestimate $18.84 billion

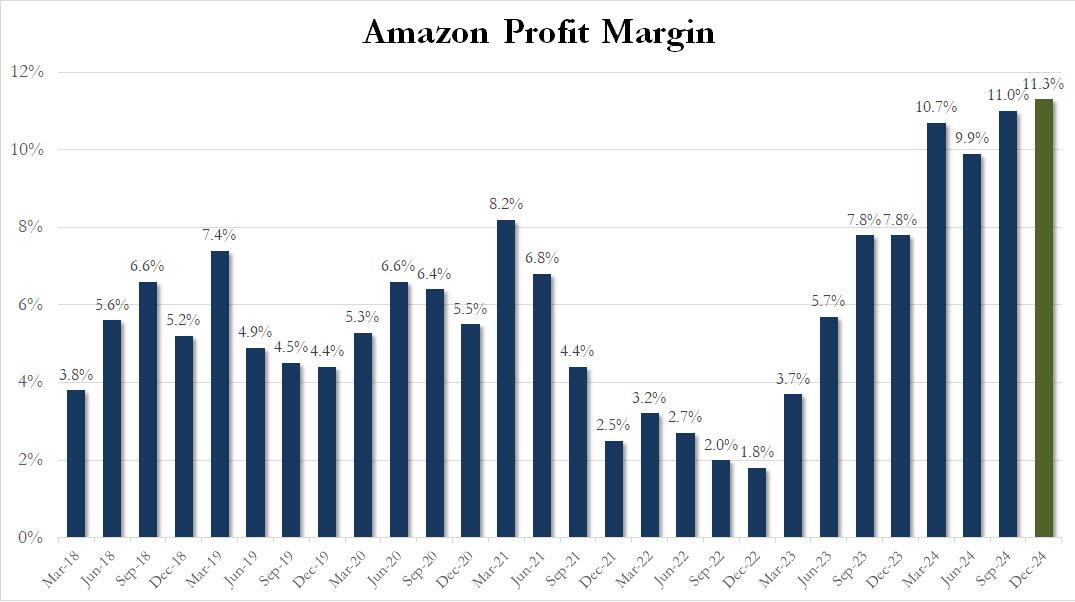

Operating margin 11.3% vs. 7.8% y/y, beatingestimate 10.1%

North America operating margin +8% vs. +6.1% y/y, beatingestimate +6.48%

International operating margin 3% vs. -1% y/y, missingestimate 3.08%

As for fulfillment expenses, these came in slightly below estimates, while the seller unit mix was slightly higher than expected:

Fulfillment expense $27.96 billion, +7.2% y/y, estimate $28.45 billion

Seller unit mix 62% vs. 61% y/y, estimate 60.2%

Of the above, the most notable highlight – as per our preview – was AWS which grew revenue by a 19% for a second consecutive quarter to $28.79BN, which however was just below the sellside estimate of $28.82BN. So maybe a little weakness here similar to Microsoft.

{kind=link}

Still, if revenue growth for AWS was a bit light, the 36.9% margin likely offset it, beating estimates of 34.7%, but below last quarter’s print of 38.1%. Elsewhere, North American profit rose to $25 billion, resulting in a profit of 6.44%, the highest since at least 2015 (although one wonders how much higher this number can rise). Meanwhile, international margins dipped to 3.03% from 3.63%.

{kind=link}

As a result of the jump in North American profits, Amazon’s consolidated operating margin rebounded strongly, and after dipping modestly in Q2 from the previous record, rose to a new all time high of 11.3% in Q4.

{kind=link}

However, while the above data was mixed to modestly solid, it was the company’s guidance that led to an after hours drop in the stock; that’s because the company projected profit and revenue in the current quarter both of which came in below Wall Street expectations:

Sees net sales $151.0 billion to $155.5 billion, below the estimate of $158.64 billion

Sees operating income $14.0 billion to $18.0 billion, below the estimate$18.24 billion

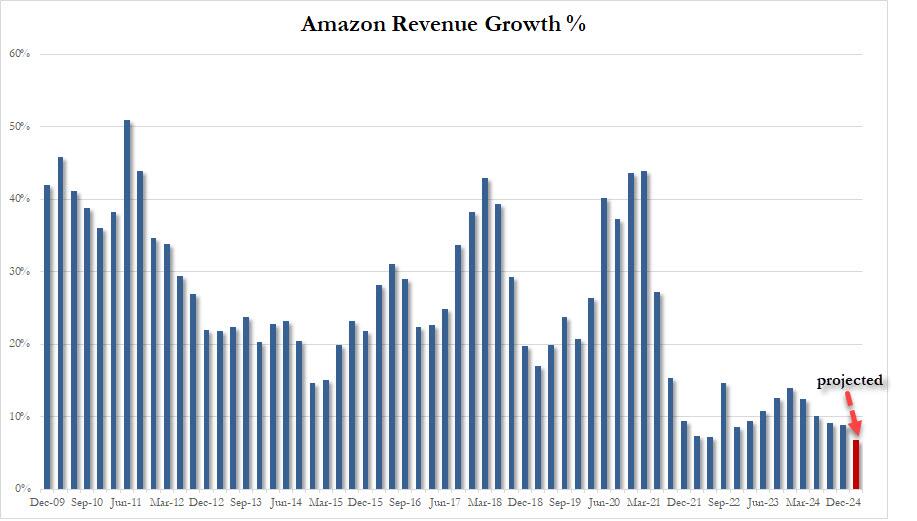

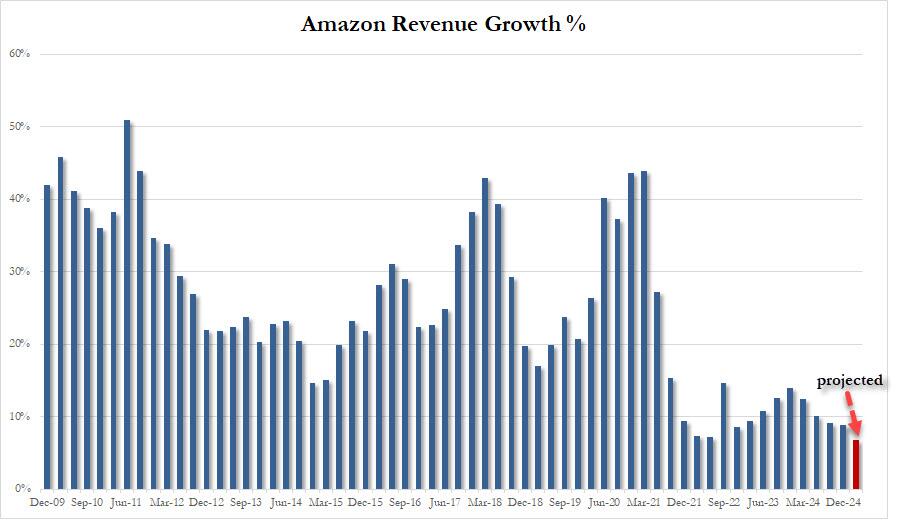

If accurate, that would mean Q4 revenue will grow at the slowest pace since the global financial crisis.

{kind=link}

And while any other day the cloud miss and ugly guidance would have been enough to send the stock tumbling – as it did for a bit, sliding as much as 7% after hours, the unprecedented retail BTFD kneejerk reaction has taken the stock after hours and remarkable pushed it back flat on the session as the market plumbs new levels of stupidity.

{kind=link}

Tyler Durden

Thu, 02/06/2025 – 16:38