Futures Slide As US Returns From Holiday And Data Deluge Looms

US equity futures are trading near session lows, tracking Monday’s slide in global markets which sent Chinese stocks to 7 month lows, after US markets were closed for Labor day yesterday. As of 8:00am, S&P futures are lower by 0.5% trading around 5630 and unchanged since mid-August even as they nearly hit a new all time high on Friday, while Nasdaq futs lag, down 0.6% with both Mag7 and Semis are under pressure (NVDA -2.4%).Bond yields are ~2bps higher with the USD trading near session highs. Commodities are weaker with all 3 complexes coming for sale; gold and natgas are relative bright spots. Today’s macro data focus is on ISM-Mfg and construction spending as we have a heavy data week capped with Friday’s NFP which is likely the determinant for the Fed cutting 25bps or 50bps. Friday also has the last 2 Fedspeakers before the Fed’s blackout window.

{kind=link}

In premarket trading, Nvidia fell more than 2% in premarket trading as most members of the Magnificent Seven technology stocks lost ground. Boeing dropped 3% after Wells Fargo downgraded the stock to underweight, giving the planemaker a rare negative analyst rating. Wells Fargo also cut its price target to a Street low. Here are the other notable premarket movers:

Dyne Therapeutics (DYN) tumbles 32% after saying Chief Medical Officer Wildon Farwell is stepping down from the role; the company also announced clinical data from the Phase 1/2 trial of DYNE-251 in Duchenne muscular dystrophy

Polestar (PSNY) rises 4% after appointing Jean-Francois Mady as CFO.

United States Steel (X) falls 5% after Vice President Kamala Harris joined President Joe Biden in declaring the company should remain domestically owned and operated.

Unity Software (U) climbs 5% as Morgan Stanley turned bullish on the stock, saying there’s a clear potential for upward revisions in the video-game tool maker’s Create business.

Vaxcyte (PCVX) soars 30% after posting positive topline data from a Phase 1/2 study of VAX-31; based on the strength of the results from the study, the company has selected VAX-31 to advance to an adult Phase 3 program.

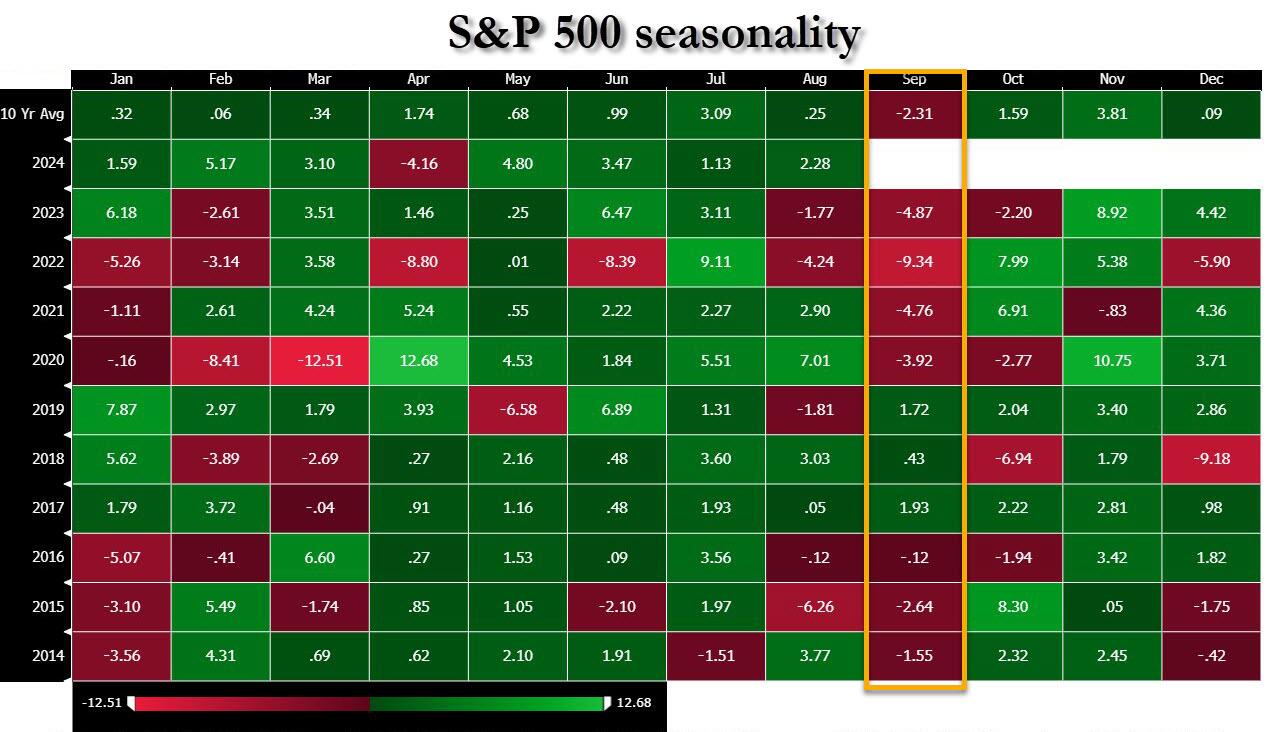

The month of September – known for being historically brutal for stocks, bonds and gold – has begun in a more benign fashion, with global equities hovering near all-time highs, although selling pressure has emerged out of the gate.

{kind=link}

In what is historically a poor month for virtually all assets, traders are bracing for fresh bouts of volatility in the runup to the anticipated start of the Fed’s rate-easing cycle this month. Swap traders are currently pricing a roughly one-in-five chance of a 50 basis-point opening cut, a decision which will be cemented by Friday’s jobs report.

The publication of US manufacturing data later Tuesday will mark the start of a busy week of economic reports (previewed here), culminating with the nonfarm payrolls report on Friday. A similar series of releases in August induced fears that the US economy was heading for a hard landing, whiplashing markets.

“Markets need to be careful what they wish for to some extent,” Daniel Murray, deputy chief investment officer and global head of research at EFG Asset Management, said in an interview on Bloomberg Television. “If rates decline by a lot, and very quickly, then that would typically signify a very weak macro environment, and that usually isn’t very good for equity markets.”

European stocks fell, tracking declines in commodities as global growth concerns sap investor sentiment. The Stoxx 600 is down 0.3%, led by losses in mining and energy names.

Earlier in the session, Asian equities traded in a narrow range following their biggest drop in nearly a month on Monday, as consumer and financial shares rose while the region’s major semiconductor-related stocks fell. The MSCI Asia Pacific Index was little changed, with Mitsubishi UFJ and Sumitomo Mitsui Financial Group among the biggest boosts while TSMC and Samsung declined. Japan’s Topix rose for a sixth straight session, its longest streak since March, boosted by banks. Volumes were thin, outside of China, with a lack of clues from overseas as US markets were closed Monday for a holiday. Chinese stocks swung between gains and losses. Equities in Asia’s largest economy have fluctuated this year amid persistent concerns over slowing growth and a weak property market, while some investors have touted their cheap valuations.

“I think currently bad news is reflected in stocks — the problem is the timing of when the recovery is going to take place,” Lorraine Tan, director of Asia equity research at Morningstar, said on Bloomberg TV. “The good news” is that consumption is not falling off a cliff, with people in lower-tier cities upgrading to more premium products, she said.

In FX, the dollar rose for a fifth day, its longest winning streak since mid-April. The Japanese yen rebounded from Monday’s fall, rising 0.7% against the greenback and to the top of the G-10 FX pile after Bank of Japan Governor Ueda reiterated the central bank will continue to raise interest rates if the economy and prices perform as expected. The Australian dollar is the weakest with a 0.7% drop.

In rates, treasury yields were little changed vs Friday’s closing levels as US markets reopen after Labor Day holiday. Front-end lags slightly, flattening 2s10s curve, amid weakness in Japan’s front-end rates (and yen gains) after Bank of Japan Governor Kazuo Ueda reiterated the central bank will continue to raise interest rates if the economy and prices perform as expected. US 10-year yields trade around 3.91% with bunds and gilts outperforming by ~2bp on the day. US 2s10s, 5s30s spreads flatter by 0.8bp and 1.5bp as front-end and belly slightly lags rest of the curve. European bonds gain. The US session includes S&P Global and ISM manufacturing PMIs, and the investment-grade corporate bond issuance slate is expected to be heavy.

In commodities, Brent crude futures drop 1.5% to $76.40 while iron ore falls over 3% in Singapore. Goldman slashed its copper forecast for next year by almost $5,000 a ton, saying China’s increasingly disappointing economic recovery will delay an expected rebound. The same pessimism over China is also hurting iron ore, which dropped to a two-week low Tuesday after losing its hold above $100 a ton.

The US event calendar includes August S&P Global US manufacturing PMI (9:45am), July construction spending and August ISM manufacturing (10am). No Fed speakers are scheduled; Williams and Waller are slated to speak Friday

Market Snapshot

S&P 500 futures down 0.2% to 5,651.50

STOXX Europe 600 down 0.1% to 524.29

MXAP up 0.1% to 185.89

MXAPJ down 0.5% to 572.97

Nikkei little changed at 38,686.31

Topix up 0.6% to 2,733.27

Hang Seng Index down 0.2% to 17,651.49

Shanghai Composite down 0.3% to 2,802.98

Sensex little changed at 82,505.78

Australia S&P/ASX 200 little changed at 8,103.23

Kospi down 0.6% to 2,664.63

German 10Y yield down 2 bps at 2.32%

Euro down 0.2% to $1.1052

Brent Futures down 0.9% to $76.84/bbl

Gold spot up 0.2% to $2,505.21

US Dollar Index little changed at 101.70

Top Overnight News

Chinese steel exports set to hit an 8-year high this year as slowing domestic growth forces companies to seek out foreign markets, a dynamic that will escalate trade tensions between Beijing and other countries. China also opened a trade investigation into imports of certain Canadian agricultural and chemical products, a move that follows Canada’s decision to impose tariffs on Chinese autos, steel, and aluminum imports. FT / WSJ

Turkey has formally asked to join the BRICs group of emerging market countries as Erdogan feels the “center of gravity” is shifting away from developed economies. BBG

Israel sees massive worker strike as the country looks to pressure Netanyahu into striking a ceasefire deal. FT

Poland says it has a duty to shoot down Russian missiles flying over Ukraine that could be a potential threat to Polish airspace. FT

Germany’s far-right AfD has won a regional election in the country (the first time a far-right party has secured victory in Germany’s postwar history) in another sign of sinking support for the current Scholz government. FT

Harris plans to spend a massive ~$370M on advertising between now and the election, including the biggest digital ad campaign in history. FT

Growing number of Americans think the country and economy are headed in the right direction (the upward shift comes largely from Democrats, who are feeling more optimistic since Harris entered the race). WSJ

Washington prepared to make a “take it or leave it” Gaza ceasefire proposal to Israel and Hamas and is prepared to exit the negotiations if a deal isn’t struck. WaPo

Apartment rents are set to face upside risk thanks to a sharp slump in new unit construction over the last several quarters. WSJ

Intel and Japan will establish a research and development hub for advanced semiconductor manufacturing equipment in Japan: Nikkei.

Japanese firms will not be supplying Apple iPhone displays as the Co. is ending LCD usage excluding Japan Display (6740 JT) and Sharp (6753 JT) from the iPhone supply chain: Nikkei

A more detailed look at global markets courtesy of Newsquawk

APAC stocks eventually faltered and traded in the red across the board, albeit with losses somewhat limited amid cautious trade ahead of the US return and accompanying risk events, such as ISM Manufacturing today and NFP on Friday.ASX 200 saw mild pressure from its Consumer Staples and Mining stocks, but losses are cushioned by Tech, Telecoms, and Energy. Nikkei 225 was initially firmer amid the weaker JPY with the upside is led by the Industrial sector, however, gains later trimmed as the JPY gained ground. Hang Seng and Shanghai Comp were subdued and in-fitting with a broader risk tone with pressure in Real Estate continuing to be a grey cloud over the nation, whilst PBoC liquidity injections get more and more tepid.

Top Asian News

South Korean Vice Finance Minister said inflation is expected to stabilize in the lower 2% range going forward, according to Reuters.

BoK sees inflation maintaining the current stable trend for the time being, according to Reuters.

Japan says it will spend about JPY 989bln from the reserve fund to cover energy subsidies, according to Reuters

PBoC injected CNY 1.2bln via 7-day Reverse Repo at a maintained rate of 1.70%

Japanese Chief Cabinet Secretary Hayashi wishes to declare the end of inflation as soon as is possible, adds that they should not hesitate to deploy fiscal spending if required to bolster the economy.

BoJ’s Ueda submitted documents to a government panel explaining the recent policy announcement, via Bloomberg; article writes the document suggests the central bank will continue to hike if the economy/prices perform as expected.

European bourses, Stoxx 600 (-0.1%) are mixed, having opened with a generally positive bias. Indices initially traded sideways, but have slowly deteriorated as the morning progressed, currently near session lows.European sectors are mixed. Consumer Product & Services top the pile, whilst Basic Resources is the clear laggard, hampered by losses in metals prices. US Equity Futures (ES -0.4%, NQ -0.6%, RTY -0.8%) are lower across the board, as US participants return from US Labour Day holiday. The docket for today includes US PMIs (Finals) and more importantly the ISM Manufacturing data.

Top European News

ECB decisions look get more contentious once interest rates fall to about 3%, according to Bloomberg sources.

Oil Swings as Traders Weigh China Demand Against Libya Outage

Swiss Inflation Slows as SNB Prepares September Rate Cut

BBVA’s Sabadell Takeover Bid Gets Approval from UK Regulator

EU’s Merger Powers Take Hit in Illumina-Grail Court Defeat

FX

DXY was flat for most of the European morning, but has edged higher in recent trade. Currently in a 101.62-83 range. The key inflection point will be on US ISM Manufacturing data, with a particular focus on the employment components, ahead of the NFP report on Friday.

EUR is softer and trading towards the lower end of a 1.1035-72 range, and dipping below its 20 DMA. European docket is thin, with only ECB’s Nagel scheduled.

GBP is on the backfoot, in what has been yet another session free from any UK-specific catalysts. Cable currently sits in a 1.3108-85 range, a trough which marks the lowest in 7 days. BoE’s Breeden is due to speak today at 13:45BST.

The JPY is by far the best performer among G10 peers, with USD/JPY slipping below 146.00. Pressure in the pair could be attributed to Bloomberg reports which stated that BoJ’s Ueda submitted documents to the gov’t, which noted that the BoJ would continue to hike if the economy/prices perform as expected.

Antipodeans are amongst the worst performers across the G10s, given the subdued risk tone in APAC trade which led a sharp sell-off in metals prices.

CHF began the European session on the front-foot, largely attributed to its safe-haven status; however, it saw modest weakness on the back of a slightly softer inflation report.

PBoC set USD/CNY mid-point at 7.1112 vs exp. 7.1120 (prev. 7.1127)

Fixed Income

USTs are flat as we await the return of US participants from Monday’s holiday, but as focus remains on US ISM Manufacturing data later. No real follow-through from JGB pressure overnight after a relatively subdued short-dated tap. In a narrow sub-10 tick range which is at the mid-point of Monday’s 113-14 to 113-30+ band.

Bunds are essentially unchanged in a much narrower c. 20 tick range vs. the 40+ tick range seen on Monday in the wake of weekend political developments. Bunds are in a 133.27-133.48 band which is entirely within Monday’s 133.16-133.62 range.

Gilts are trading similar to the above, with the benchmark also within a slim 15-tick range which has just eclipsed yesterday’s peak to a 98.39 high.

Japan sold JPY 2.6tln 10-year JGB; b/c 3.17x (prev. 2.98x), average yield 0.915% (prev. 0.926%).

Books close on sale of a 2040 Gilt via syndication, orders topped GBP 107bln, via Reuters citing bookrunner

Commodities

Crude benchmarks are both significantly lower, but with differing performances given the lack of settlement in WTI, attributed to the the US Labour Day holiday. Nothing specific driving the pressure in the complex, but comes alongside incremental strength in the Dollar index. Brent’Nov as low as USD 76.05/bbl.

Spot gold is slightly firmer and has climbed back above USD 2.5k/oz after losing that figure on Monday. Strength which comes as the general risk tone remains tepid and as focus turns to US ISM Manufacturing later. Currently trading in a USD 2490-2506/oz range.

Base metals are pressured, with 3M LME Copper extending further below the USD 9.2k mark and now beginning to approach USD 9k.

Libya’s NOC declared force majeure on the El Feel oil field from 2nd September, according to Reuters.

UN hosts talks in Tripoli aimed at resolving Libya’s central bank crisis, key understandings reached, according to a statement cited by Reuters.

Goldman Sachs has cut its 2024 copper forecast to USD 10,100/ton (prev. saw 12,000/ton), due to China’s weak economic recovery. It also reduced its 2025 aluminium price estimate to USD 2,540, and remains bearish on iron ore and nickel, Bloomberg reports. The bank favours gold as a hedge, and maintained its USD 2,700 price target.

Geopolitics

“Israel Today: The security establishment is considering declaring the West Bank a zone of military security operations”, according to Sky News Arabia.

On the Israel-Hamas talks, “Sources: The US administration is not particularly optimistic about the chances of success of the new outline, even in light of the declarations made by both sides”, according to Kann News

US President Biden said they are still in the middle of ceasefire and hostage-deal negotiations, according to Reuters.

Two oil tankers, one Saudi-flagged and the other Panama-flagged, were attacked on Monday in the Red Sea off Yemen, according to Reuters sources.

China Commerce Ministry, in response to Canada’s tariffs on Chinese products, said China to initiate an anti-dumping investigation into canola imports from Canada, according to Reuters.

US event calendar

09:45: Aug. S&P Global US Manufacturing PM, est. 48.1, prior 48.0

10:00: Aug. ISM Employment, prior 43.4

10:00: July Construction Spending MoM, est. 0.1%, prior -0.3%

10:00: Aug. ISM New Orders, prior 47.4

10:00: Aug. ISM Prices Paid, est. 52.0, prior 52.9

10:00: Aug. ISM Manufacturing, est. 47.5, prior 46.8

DB’s Jim Reid concludes the overnight wrap

I’m back from the annual ritual of constantly shouting at kids for two weeks that mascarades as a holiday. Since I was last here I’ve also spent 8 hours in an online queue trying to get Oasis reunion tickets only to reach the end of it to find they’d just sold out. I’m not sure there’s been anything like it in history. So if you’ve ordered some and have two spare please let me know! If you bought them and aren’t too sure if you want to go and want to hand them over, all I can say is that the first of the two record breaking Oasis Knebworth gigs in 1996 was the worst gig I’ve ever been to. I was two-thirds of the way back in a huge field listening to the concert from the front speakers and also from the speakers half way down the field that had a delay. So the sound was terrible.

As my chances of getting tickets are sliding away, so is the memory of an incredibly strange start to August with markets completely becalmed again. But now we’ve hit September it’s back to the serious stuff with the market soon to be fully staffed again with schools fully back over the next few days. Ahead of an important payrolls print on Friday, today we see the US ISM and PMI manufacturing prints which will be interesting as both are expected to stay below 50 where they’ve been for most of the last couple of years. The headline ISM printed at 46.8 last month which was below every economists’ estimate, with the employment subcomponent (43.4) at its lowest since the initial Covid shock. This helped kick start the chain of events that culminated in the VIX printing above 65 and Japanese equity markets being down over -10% on the Monday the following week just after the weak payrolls number. So it is important to see if that ISM release was distorted or not.

The week has started quietly due to the Labor Day holiday in the US yesterday but European equities and bonds lost ground. By the close, yields on 10yr bunds (+3.7bps) were up to a one-month high, and the STOXX 600 (-0.02%) had posted a very modest decline from its record high on Friday.

One factor behind the bond selloff was actually some better-than-expected economic data from Europe, which led investors to dial back their expectations for aggressive rate cuts from the ECB. In particular, we had the final manufacturing PMIs for August, and in general there were upward revisions from the flash prints a week-and-a-half ago. In the Euro Area, the final print was at 45.8 (vs. flash at 45.6), Germany went up to 42.4 (vs. flash 42.1), and France saw a very large upward revision to 43.9 (vs. flash 42.1). So positive news relative to expectations, and by the close investors were pricing in 61bps of ECB rate cuts by the December meeting, down -1.8bps relative to the previous day.

With investors expecting slightly less dovish policy, that hurt bonds across the continent, with yields on 10yr bunds (+3.7bps), OATs (+1.5ps) and gilts (+3.7bps) all moving higher. Equities hovered either side of unchanged, with losses for the UK’s FTSE 100 (-0.15%) and Italy’s FTSE MIB (-0.15%), alongside gains for the DAX (+0.13%) and the CAC 40 (+0.20%).

Given the Labor Day holiday, US markets themselves were closed yesterday, but we did get a bit of a clue on their performance from futures. For bonds, they were consistently negative across the curve, and investors lowered the chance of a 50bp cut from 32% on Friday to 30.8% by the European close. This morning US futures are edging lower with those on the S&P 500 (-0.16%) and NASDAQ 100 (-0.34%) trading in the red. US Treasuries have recovered a little this morning versus futures yesterday and are now only around a basis point higher than Friday’s close.

Traditionally, the Labor Day holiday has been seen as the start of the home stretch towards the US election, which is taking place 9 weeks from today. Current polls and forecast models are pointing to a very tight race, with FiveThirtyEight’s projection currently giving a 57% chance of victory to Kamala Harris, and 43% to Donald Trump. The polls are similarly tight, with ReaclClearPolitics’ polling average currently giving Harris a lead of just +1.8pts, so inside the margin of error of most polls.

Given the pretty divergent proposals from the two candidates, this election is going to be one of the biggest issues for markets over the next two months. And this morning, our European economics team has put out a note (link here) looking at the economic impact of a second Trump presidency – particularly in relation to any future trade wars. They run through several trade scenarios that could be in play and how that would impact the EU and UK picture for growth and inflation. They also look at some of the policy implications that could be in consideration on both the fiscal and monetary side.

Staying on politics, one of the main developments at the weekend was the German state elections, where the far-right AfD came in first place in Thuringia, marking the first time that they’d won a state election. However, as our economists write in their post-election piece (link here), the AfD are very unlikely to enter either government, as all the other parties are expected to stick to their pledges not to enter into coalition with them. They also don’t see the results at the state level triggering early federal elections either, and their base case remains that the next federal election will be in September 2025.

Asian equity markets are trading in a narrow range amid a lack of any new catalysts after the holiday on Wall Street. As I check my screens, the Hang Seng (-0.34%), the Nikkei (-0.25%) and the KOSPI (-0.10%) are all dipping. Elsewhere, mainland Chinese stocks are mixed with the CSI (+0.07%) trading just above flat while the Shanghai Composite (-0.52%) is trading in the red.

Early morning data showed that South Korea’s inflation hit a 42-month low of +2.0% y/y in August (v/s +2.1% expected), down from +2.6% in July, mostly due to base effects, but highlighting that inflation has been stabilising more quickly than in other major economies and thus increasing the likelihood of an October rate cut.

To the day ahead, and data releases include the ISM manufacturing print for August from the US. Otherwise from central banks, we’ll hear from Bundesbank President Nagle and BoE Deputy Governor Breeden.

Tyler Durden

Tue, 09/03/2024 – 08:18