Hugo Boss Slides After Slashing Outlook As Luxury Downturn Gains Momentum

Hugo Boss tumbled as much as 10% to its lowest levels since 2021 on Tuesday after the luxury German clothing manufacturer slashed its full-year outlook. The company cited sliding demand for luxury goods due to “persistent macroeconomic and geopolitical challenges” and mounting “headwinds” across two key markets, the UK and China.

The German premium-fashion company warned that its financial outlook for 2024 faces “persistent macroeconomic and geopolitical challenges that are dampening global consumer demand.”

“These headwinds contributed to a further slowdown of industry growth, affecting the top- and bottom-line performance of HUGO BOSS in the second quarter,” the company said, adding, “The overall market environment remained particularly challenging in key markets such as the UK and China.”

According to Hugo Boss’s preliminary second-quarter results and full-year outlook statement, it now expects full-year sales of up to 4.35 billion euros, down from a previous forecast of up to 4.45 billion euros.

Here are the key developments in the second quarter:

Group sales decrease 1%currency-adjusted to EUR 1,015 million as challenging macroeconomic and geopolitical conditions weigh on global consumer demand

Gross margin increases 50 basis points to 62.9% as HUGO BOSS realizes further efficiency gains in its global sourcing activities

EBIT amounts to EUR 70 million (-42%), reflecting softer sales trends and strategic investments into the business

Inventories improve by -7% amid ongoing tight inventory management, supporting strong free cash flow generation in Q2 of EUR 143 million (+137%)

“We are operating in a period of significant global macro uncertainty, which also affected our performance in the second quarter,” CEO Daniel Grieder wrote in the statement.

Grieder continued, “Although the timing of any macro recovery remains uncertain, our strategy of consistently investing in our strong brands, BOSS and HUGO, gives us confidence in our ability to continue driving above-trend growth and capturing further market share.”

Shares of Hugo Boss plunged as much as 10% in Germany on Tuesday. That’s the lowest intraday level since April 2021.

{kind=link}

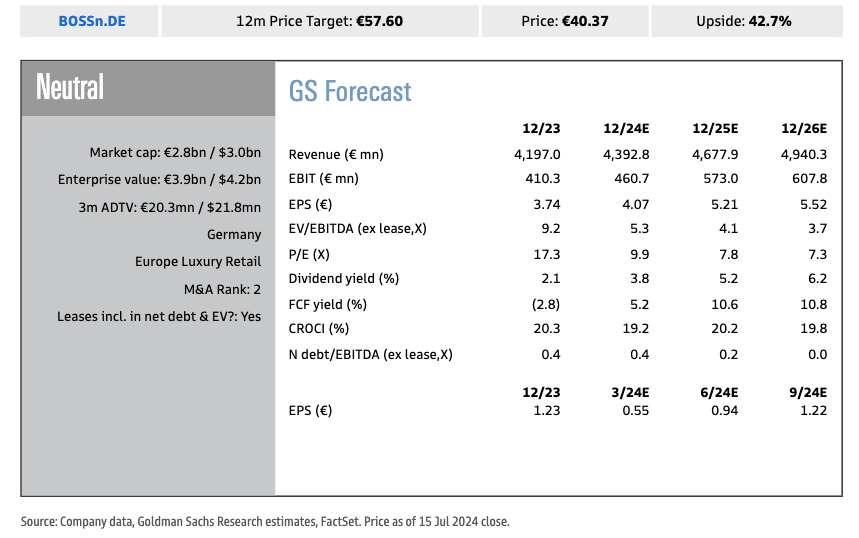

Here’s additional color on the preliminary results from Goldman’s Louise Singlehurst:

2Q24 Preliminary results – Sales -3% below, EBIT -36% light versus consensus expectations. Hugo Boss has pre-released preliminary 2Q24 results, reporting cFX sales declines of -1% (€1,015mn reported), below Visible Alpha Consensus Data (+2%) and GSe (+3%). EBIT in 2Q24 amounted to €70mn, significantly below cons/GSe of €110mn/€108mn, driven partly by the top-line miss and partly by higher than expected opex (marketing +21% YoY, brick and mortar costs +12%) with GP margins inline with expectations.By Channel:The overall composition of the result is soft, with the miss driven by online (-1000bps) and retail deterioration (-100bps), with wholesale broadly inline (-50bps). By Geography:All regions saw a deceleration in trends and drove the miss (-200-300bps lower).

FY24 EBIT guidance is -14% lower vs. prior midpoint:Given greater than expected macro uncertainty, the company has revised lower its reported sales growth guidance to +1-4% (+3-6% prior, cons. +4%, GSe +5%) with EBIT now expected to be between €350-430mn (prior €430-475mn, cons. €439mn, GSe €461mn). We note the updated midpoint is -14% below the prior midpoint or -11% below current FY24 consensus, with a wider range expected (€80mn vs. €45mn prior).

Balance Sheet / CF:BOSS has finished the period with a solid inventory position as a % of sales (-340bps YoY to 24.9%, vs. -330bps in 1Q24) supporting strong Working Capital benefits, and FCF generation (€143mn).

GS View: We expect market expectations were relatively low coming into the print on broader concerns around the premium consumer, with BOSS having underperformed in the last 1m (-8% vs. STOXX 600 +1%). However given BOSS revised expectations lower in March, followed by further market downgrades in May and now incrementally negative updates here, we see risk that normalising brand momentum and relatively thin margins continues to skew earnings risk to the downside. One positive remains the company’s ability to manage working capital, which gives greater FCF support in FY24 as the company moves towards medium term targets inventory to sales of

Singlehurst remains “Neutral” on Hugo Boss.

{kind=link}

Other Wall Street analysts offered their views on the preliminary results (courtesy of Bloomberg):

Citi (neutral)

Analyst Thomas Chauvet says quarterly sales growth was the weakest since Daniel Grieder became CEO of Hugo Boss in June 2021, and it is first time the company has cut FY guidance during his tenure

Would expect consensus for FY24 sales and Ebit to drop by 2% and 10% respectively, toward mid-point of revised guidance

There had been “three years of nearly flawless execution and delivery,” but the premium casual-wear demand environment is now more subdued

Morgan Stanley (equal-weight)

Consensus is likely to move down to at least the mid-point of the new wide range, according to Grace Smalley

This would mean about 10% downgrade to FY24 Ebit consensus expectations, with FY25 numbers also likely to “move down meaningfully”

RBC (outperform)

Analyst Manjari Dhar says new Ebit guidance is about 14% below prior guidance at the midpoint, seemingly in line with RBC’s bear case scenario

Still views Hugo Boss as a good player in the premium apparel space, but notes tougher backdrop in key markets

Deutsche Bank (buy)

While sales missed consensus by only 2% in 2Q, Ebit was “massive” miss, analyst Michael Kuhn writes

Miss essentially due to higher than expected operating expenditure

Likely no earnings growth for the company now in 2024

Oddo BHF (neutral vs outperform)

2Q Ebit significantly below expectations, writes analyst Andreas Riemann, who downgrades rating to neutral

Brick-and mortar retail and digital both had “difficult” performance

Growth continues in Americas, but declines in EMEA and APAC

The disappointing update comes as shares of Swiss watchmaker Swatch crashed the most in four years on Monday after the company reported a profit decline amid a slowdown in China. Also on Monday, trench coat maker Burberry suspended its dividend and replaced its CEO on a failed turnaround.

Meanwhile, in the luxury space, all eyes are on LVMH Moet Hennessy Louis Vuitton, who will report next week. That will be a key signal on the overall health of the luxury industry.

In the US, a consumer slowdown continues to gain momentum. We have covered this extensively in the last several months via multiple Goldman notes.

Tyler Durden

Tue, 07/16/2024 – 09:10