‘Dovish’ Powell Destroys ‘Hawkish’ Dots; Sends Stocks, Gold, & Crypto Soaring

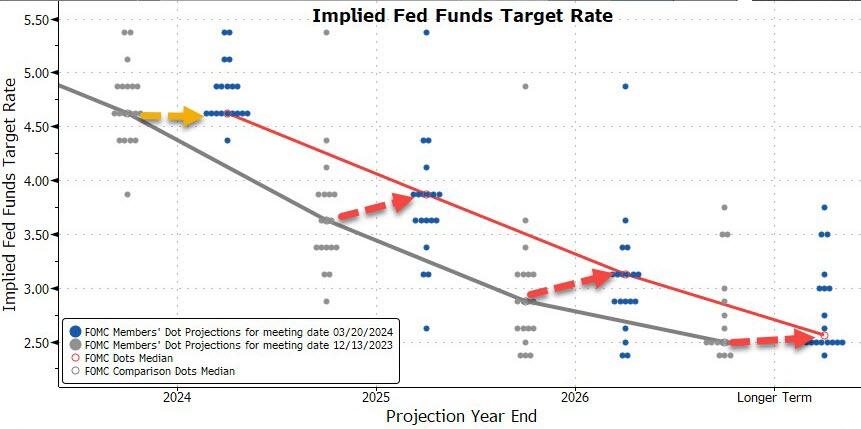

The FOMC dropped its dot-plot and it was unequivocally more hawkish than the Dec dots with 2024 flat at 3 cuts (though more voters moved towards only 50bps), but 2025 and beyond saw rate-cuts erased from the projections…

{kind=link}

Source: Bloomberg

{kind=link}

Powell reiterated his long-held view that the dot-plot does not amount to a “plan”.

Powell calls the longer run interest rate change “pretty modest”.

“I don’t think we know that,” Powell says about whether this will be a lasting trend.

However, Powell did admit rates are unlikely to be going ZIRP anytime soon:

“I don’t see rates going back down to that level but I think there’s tremendous uncertainty on that.”

If the Fed eases too much or too soon, he says, we could see inflation come back.

And if we ease too late, we could do unnecessary harm to employment.

“We want to be careful,” Powell says, stressing that “the risks are really two-sided here.”

Powell signaled balance sheet reduction will slow (less QT >> more QE):

“We did not make any decisions today. The general sense of the committee is that it’ll be appropriate to slow the pace of runoff fairly soon, consistent with the plans we previously issued.”

Powell also rather dismissed the recent jump in inflation:

“There’s reason to think that there could be seasonal effects there,”Powell says about the January CPI and PCE figures, and then says that February PCE wasn’t “terribly high.”

So, wait, the seasonally-adjusted data is showing seasonal affects now?

Powell watching every uptick in Brent until the June FOMC pic.twitter.com/ICuQffT8F3

— zerohedge (@zerohedge) March 20, 2024

So uber-dovish: Brad Conger, chief investment officer at Hirtle Callaghan & Co., weighs in:

“The FOMC was on the horns of a dilemma. January and February’s inflation readings showed that progress towards the Fed’s 2% target is stagnating at best and inflecting back up at worst.

The facts called for a hawkish adjustment to reflect the slackening progress. Instead, we got a dovish adrenaline shot — reaffirming the November pivot. The boost to financial conditions is working counter to the Fed’s price mandate. So much for Jay Powell’s presumed admiration for Paul Volcker.”

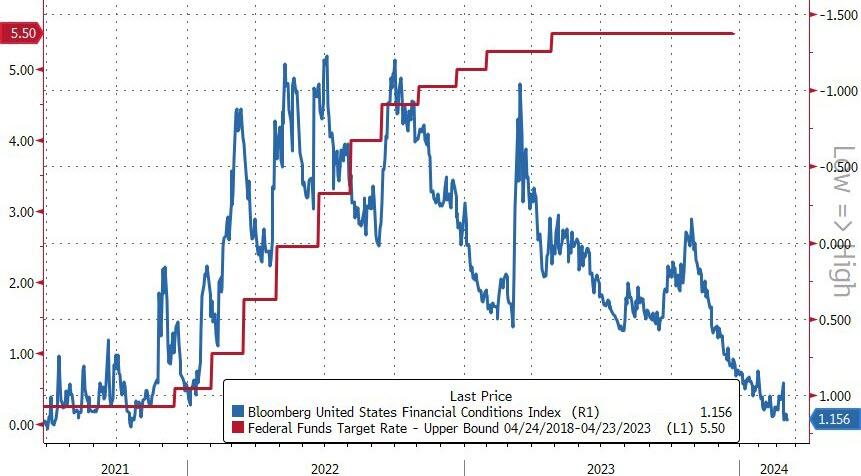

Financial Conditions are literally at the same level of ‘looseness’ as they were before The Fed hiking cycle began…

{kind=link}

Source: Bloomberg

Powell had an opening to talk down the rallies and risk assets and didn’t take it. It’s just unbelievable (except in an election year) that he didn’t even acknowledge the questioner’s characterization of financial conditions as having eased.

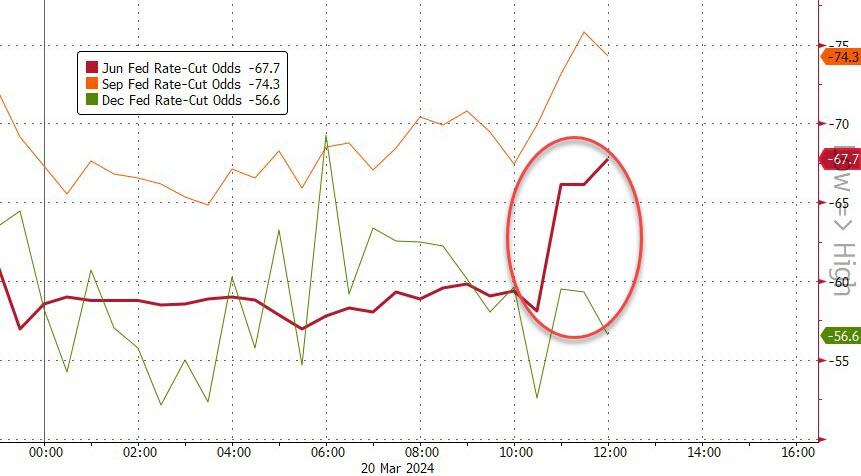

And, comically, rate-cut expectations actually (dovishly) increased today for 2024…

{kind=link}

Source: Bloomberg

The odds of a rate-cut in June jumped to 67%…

{kind=link}

Source: Bloomberg

And Powell’s dovish dance sent assets to the moon as the dollar dived…

{kind=link}

Source: Bloomberg

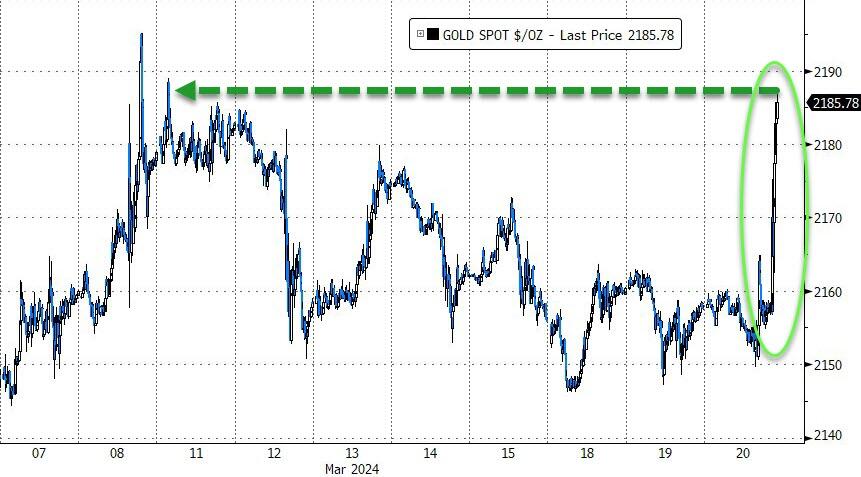

…which helped send gold soaring to a new record high…

{kind=link}

Source: Bloomberg

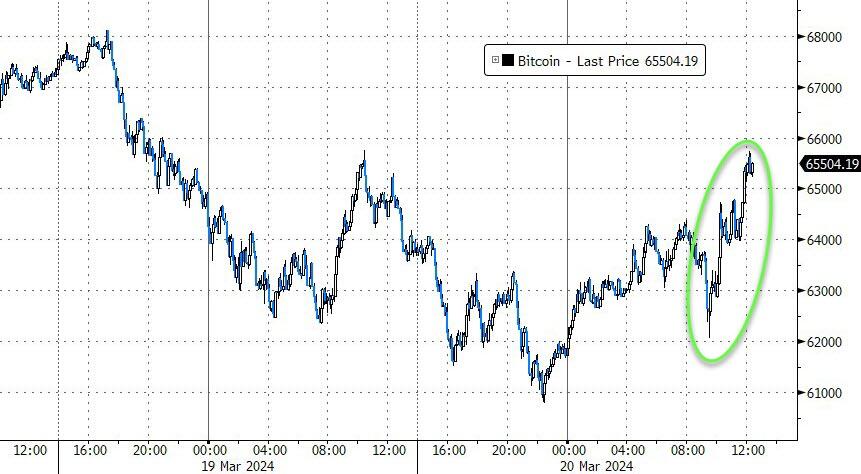

…and Bitcoin broke back above $65,000…

{kind=link}

Source: Bloomberg

Which was notable after a record net outflow from BTC ETFs yesterday…

{kind=link}

Source: Bloomberg

Stocks soared higher – new record highs for the S&P, Dow, and Nasdaq – with Small Caps exploding to one of the best day of the year so far…

{kind=link}

Which is funny because stocks didn’t give a shit about rate-cut expectations anyway…

{kind=link}

Source: Bloomberg

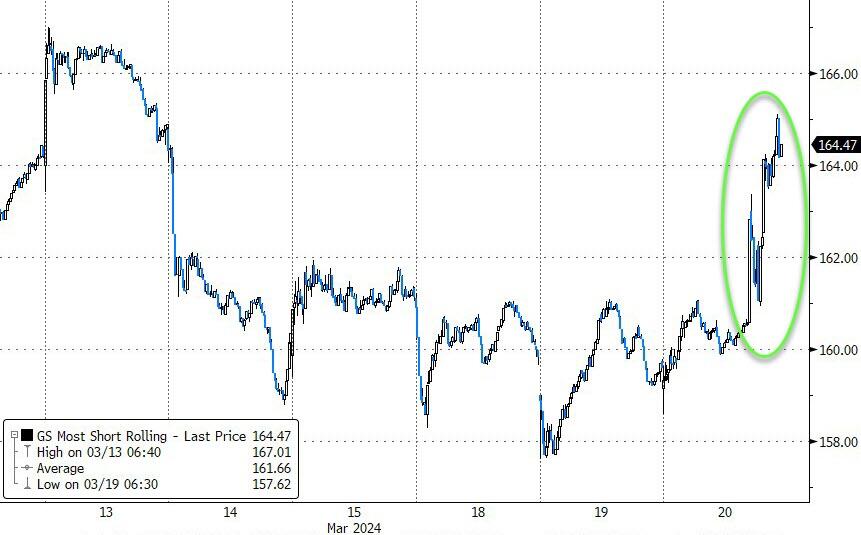

Shorts were squeezed hard today

{kind=link}

Source: Bloomberg

…and MAG7 stocks soared to a new higher record high…

{kind=link}

Source: Bloomberg

Treasury yields spiked on the ‘Dots’ then tumbled on Powell’s dovishness today led by the short-end (2Y -8bps, 30Y unch)…

{kind=link}

Source: Bloomberg

Which prompted a massive bull steepening in the yield curve…

{kind=link}

Source: Bloomberg

Despite the weak dollar and economic excitement from The Fed’s SEP, crude slipped lower on the day, back below $82 after the DOE data…

{kind=link}

Source: Bloomberg

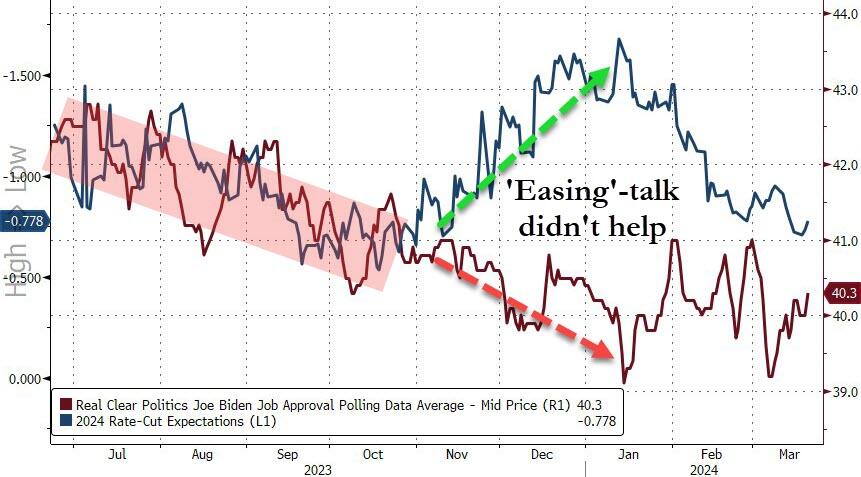

Finally, is this what The Fed fears?

{kind=link}

Source: Bloomberg

Or is a Biden loss a bigger worry?

{kind=link}

Source: Bloomberg

They tried to jawbone the big pivot/easing of rate-cut expectations and it showed no impact on Biden’s approval rating, So what next? QE?

Tyler Durden

Wed, 03/20/2024 – 16:00