Bubbly Parts Of The Market Might Get Bubblier Still

Authored by Simon White, Bloomberg macro strategist,

The tech sector continues to drive returns in US stocks. Multiples are high, but still not quite as high as they reached on the eve of the dot-com bust, while most sectors’ earnings yield is not yet as unattractive as it was versus 10-year yields in early 2000.

Number Go Up is a recent book by Bloomberg’s Zeke Faux about crypto. The title probably originated in a 2017 post on X, formally known as Twitter, about how asinine bitcoin investing had become: “NUMBER GO UP, ME COULD HAVE HAD BIG NUMBER, GOON BAD.”

Maybe we’re not quite there in stocks, but burgeoning FOMO-ness is pushing investors to override their prefrontal cortices and engage in ever more risky behavior.

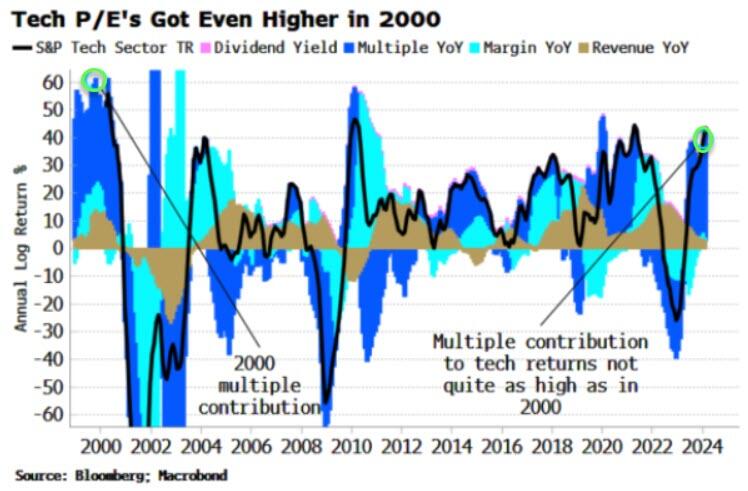

The epicenter of market froth is the tech sector. P/E multiples are the biggest driver of S&P returns currently, but not out of keeping with several periods over the past 25 years. It’s a different story with the tech sector, though, where P/Es are driving tech returns by more than they have since the run-up to the 2000 tech bust, apart from a brief period in the pandemic and in the bear markets of 2001 and 2008.

{kind=link}

Multiples were driving the majority of the sector’s returns in the late 1990s, which were running at 50%-60% on an annual basis. That’s a bit lower than today’s ~40%, but not by much.

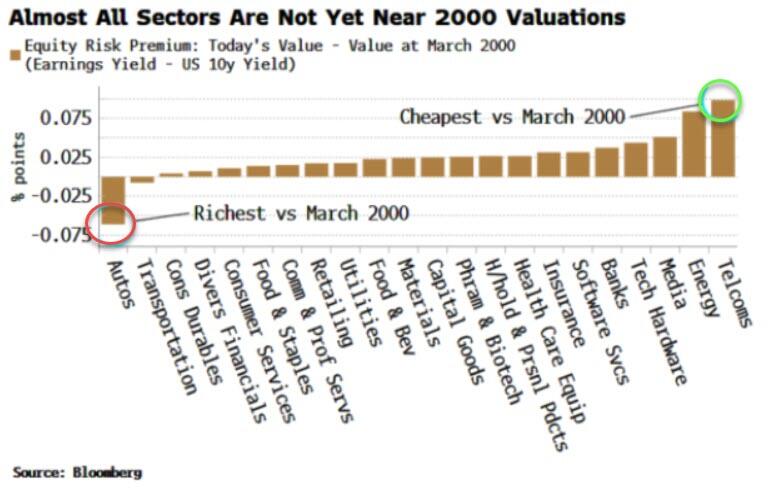

More overvaluation could also be seen in equity risk premia (ERPs) before we get near Dotcom-mania levels.

Tech sectors such as hardware and software services have among the most expensive ERPs, but those sectors remain well above the nadirs they reached in 2000. Indeed, almost all sectors, other than autos and transportation, are higher than they were back then.

{kind=link}

Historically, therefore, we could see things in the tech sector and broader market get even wilder before we see any major correction in prices. Fortunately, repressed volatility is making portfolio hedges more and more attractive,with a 5000 put on the S&P expiring at the end of the year costing a little more than 3%.

Bull markets are treacherous – or at least they should be. If you as investor are blithely long, then you’re missing something. There are several emerging parallels (broad over-valuation, high household allocation, etc) with today’s market and the Dotcom period investors should be aware of. Nonetheless, number may keep going up for now.

Tyler Durden

Tue, 03/05/2024 – 08:30