What Caused China’s Quant Quake

While it has gone largely underreported in western media, in the past week China launched a war against both quant funds and High Frequency Traders, claiming they were responsible for the market crash observed at the start of February. But maybe Beijing does have a point, after all long-term readers will recall that one of our first crusades was against none other than US HFT funds, which first we and then others (Michael Lewis) exposed for manipulating markets.

So what exactly happened, and what caused China’s quant quake?

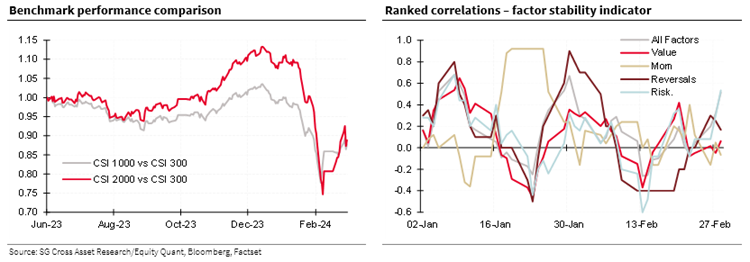

As SocGen strategist Puneet Singh explains, China did indeed go through a quant quake but this hiccup was mostly concentrated in the small- and mid-cap space. Indeed, while the CSI 1000 the CSI 2000 were down ~30% and ~34% respectively, the large cap heavy CSI 300 only lost 7.3%. The chart below left below shows that small- and mid-caps exacerbated price movements in Chinese equities.

{kind=link}

Looking at factor correlations (chart above right) clearly underscores the moves in Reversals and Risk factors (which includes vol and size). SocGen’s charts plot 5d moving average rank correlations between daily factor performance. As Singh explains, “stable correlations are inevitably required for quant strategies to work, but changes like what we saw destabilised quant models, and added to the underperformance.”

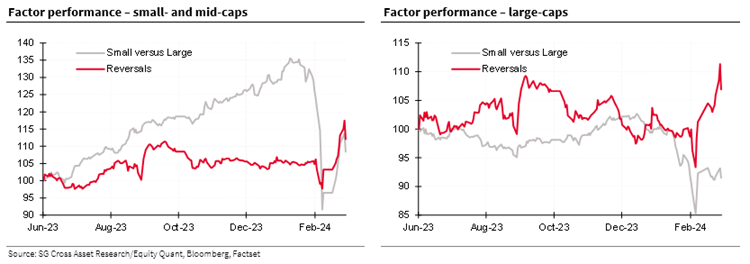

Factor performance for reversals and size in the small-mid and large cap spaces underscored the thesis: we saw small caps severely underperform large caps over the beginning of the year, with the reversal factor getting affected as well.

{kind=link}

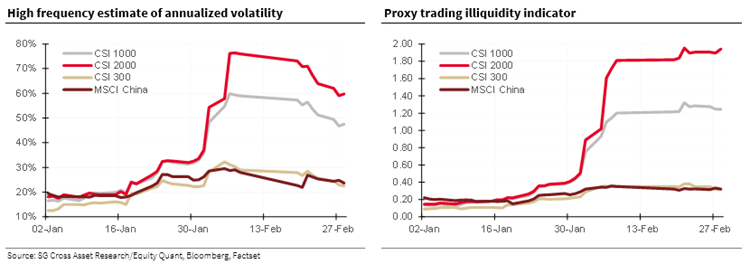

Just as was observed in the US during the August 2007 quant quake, moves of the magnitude discussed here inevitably result in spikes in volatility. Instead of using a close-to-close estimator, Socgen uses its preferred proprietary high frequency OHLC estimator (chart below left). This clearly shows how sudden the volatility pickup was in the small- and mid-cap space. This volatility spike becomes even more stark when compared to the large cap benchmarks.

Rising risks also lead to limits being triggered and risk-based unwinding of positions. In a market which is then working on a fear motive rather than profit, liquidity dries up leading to larger jumps in prices even from small trades.This is what the bank’s proxy illiquidity indicator captures (chart right below). Once again, the spike in illiquidity in the small- and mid-cap space, versus the relative calm in the large cap space potentially added to this quant quake.

{kind=link}

As Singh concludes, even as this illiquidity measure remains elevated in the CSI1000, it appears to have ticked up over the last couple of days in the CSI2000, suggesting lingering risks and perhaps more pain to come.

Tyler Durden

Thu, 02/29/2024 – 23:25