ECB Rate-Cuts In Jeopardy As Disinflation Grinds To Halt

Authored by Simon Black, Bloomberg macro strategist,

Eurozone inflation data for January just came in higher than expected, as hinted by the readings in Germany, France, etc earlier this week.Euribor futures rallied a few basis points after the release (perhaps more hawkish data was expected), but the over 90 bps of interest rate cuts priced in for this year are at risk as the fall in cyclical inflation in Europe reaches its limit.

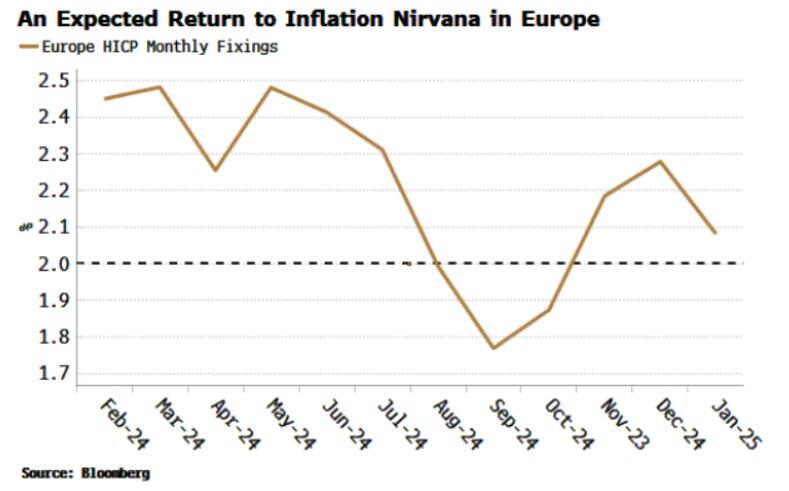

A return to an inflation eden in Europe is the base case, as with the US. Fixing swaps for Eurozone HICP anticipate it will dip back below 2% in the late summer before settling just over 2% towards year end.

{kind=link}

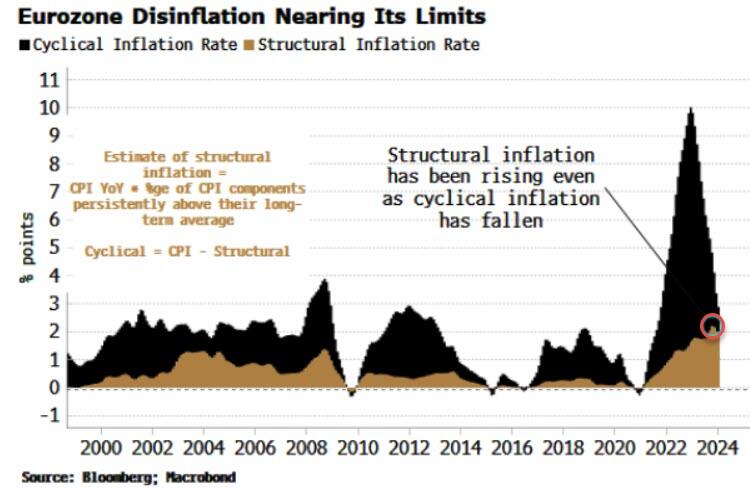

But it does not look like it will be that plain sailing.There are many ways to think about inflation, but one of the most helpful in this environment is to split it up into cyclical and structural components. We can do this by looking at all the categories in the HICP basket (there are over 400), and categorizing those that are persistently above their long-term averages as structural, and anything left over as cyclical.

Typically most of the ups and downs in headline inflation are driven by, expectedly, the cyclical component. But in this cycle, while the bulk of inflation’s fall has been driven by cyclical, structural inflation has been steadily rising.

{kind=link}

We may soon find cyclical inflation begins rising again (as it is cyclical), reinforcing still-elevated and rising structural inflation, causing the headline number to re-accelerate.

In January’s inflation report, the biggest positive monthly contributors to headline were cyclical in nature, i.e. electricity, gas and water, and food. As in the US, and across asset classes, a risk of an inflation revival is not yet being priced in European rate and bond markets.

Tyler Durden

Fri, 03/01/2024 – 08:10