“Who Could Be Next”: Top Canadian Pension Fund Sells Manhattan Office Tower For $1, Sparking Firesale Panic

New York during the inflationary surge of the late 70s and early 80s was a mythical place where one could purchase a Park avenue penthouse for $1 (while assuming the copious debt, of course). Now, thanks to the brutal bear hug of the highest interest rates in 40 years and the ongoing CRE crisis, those legendary days have made a comeback to the Big Apple, if only in the realm of commercial real estate for now.

According to Bloomberg, Canadian pension funds – which until recently had been among the world’s most prolific buyers of real estate, starting a revolution that inspired retirement plans around the globe to emulate them because, in the immortal words of Ben Bernanke, Canadian real estate prices never go down…

{kind=link}

… are finally realizing that gravity does exist. And so, the largest one among them is taking steps to limit its exposure to the most-beleaguered commercial property type — office buildings.

Canada Pension Plan Investment Board has recently done three deals at deeply discounted prices, selling its interests in a pair of Vancouver towers, and a business park in Southern California, but it was its Manhattan office tower redevelopment project that shocked the industry: the Canadian asset manager sold its stake for just $1.The worry now is that such firesales will set an example for other major investors seeking a way out of the turmoil too, forcing a wholesale crash in the Manhattan real estate market which until now had managed to avoid real price discovery.

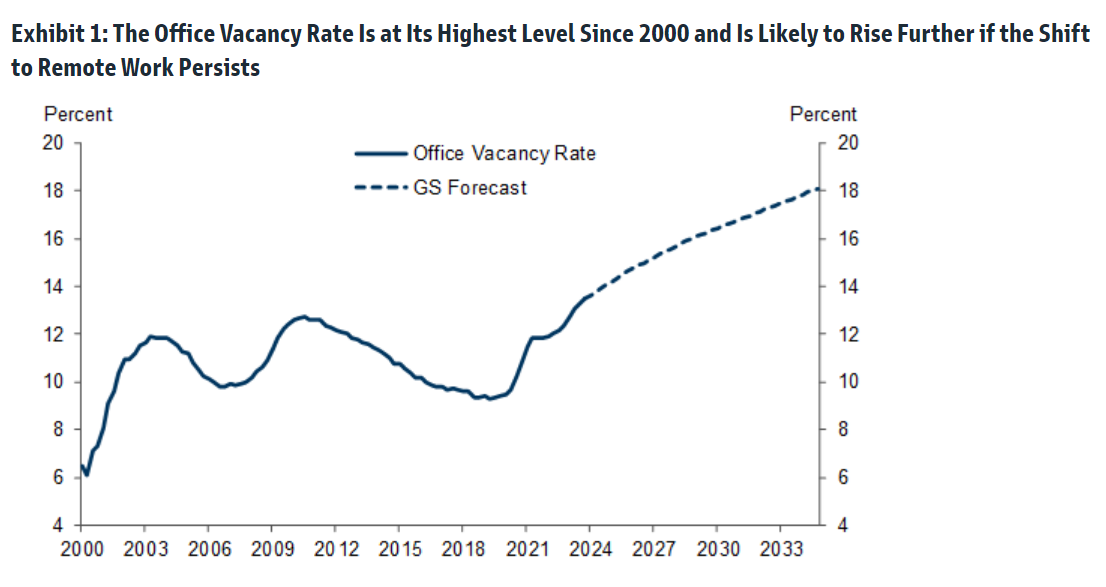

Indeed, as Goldman wrote earlier this week, while office vacancy rates are expected to keep rising well into the next decade..

{kind=link}

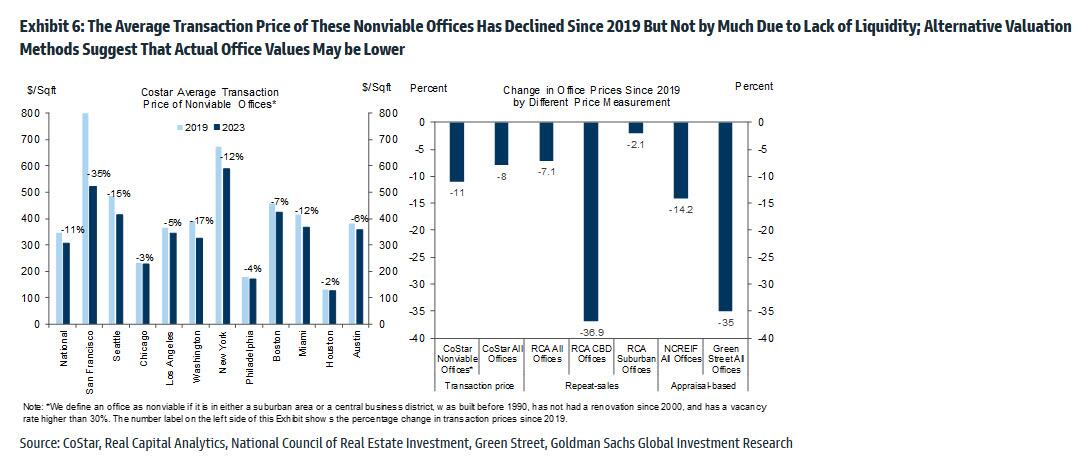

… the average price of many nonviable offices has fallen only 11% to $307/sqft since 2019 (left side of Exhibit 6). The bank goes on to note that in the hardest-hit cities, as many as 14-16% of offices may no longer be viable, and their average transaction prices have already declined by 15-35%.However, because of lack of liquidity in this market, these recent transaction prices have not yet started to reflect the current values of many existing offices.Goldman ominously concludes that “alternative valuation methods, like those that are based on repeat-sales and appraisal values, suggest that actual office values may be farlower than the average transaction price.” Well, a $1 dollar price would certainly confirm that actual office values are far, far lower (more in the full Goldman noteavailable to professional subscribers).

{kind=link}

And going back to the historic firesale, at the end of last year the Canadian fund sold its 29% stake in Manhattan’s 360 Park Avenue South for $1 to one of its partners,Boston Properties, which also agreed to assume CPPIB’s share of the project’s debt. The investors, along with Singapore sovereign wealth fund GIC Pte., bought the 20-story building in 2021 with plans to redevelop it into a modern workspace.

{kind=link}

“It’s the opposite of a vote of confidence for office,” said John Kim, an analyst tracking real estate companies for BMO Capital Markets. “My question is, who could be next?”

As office building anxiety has swept the financial world, as the persistence of both remote work and higher borrowing costs undercuts the economic fundamentals that made the properties good investments in the first place, a wave of banks from New York to Tokyo recently conceded that loans they made against offices may never be fully repaid, sending their share prices plunging and prompting fears of a broader credit crunch.

But the real test will be what price office buildings actually trade for – especially once the hundreds of billions of loan backing the properties mature….

{kind=link}

…. and until now there have been precious few examples since interest rates started rising. That’s why industry-watchers see such shocking liquidations like CPPIB’s as a very ominous sign for the market.

The Manhattan firesale isn’t the pension fund’s first sale: last month, CPPIB sold its 45% stake in Santa Monica Business Park, which the fund also owned with Boston Properties, for $38 million. That’s a discount of almost 75% to what CPPIB paid for its share of the property in 2018.The deal came just after the landlords signed a lease with social media company Snap that required they spend additional capital to improve the campus, Boston Properties Chief Executive Officer Owen Thomas said on a conference call.

Peter Ballon, CPPIB’s global head of real estate, declined to comment on the recent deals, but said the fund has continued to invest in office buildings, including a recently completed, 37-story tower in Vancouver.

“Selling is an integral part of our investment process,” Ballon said in an emailed statement. “We exit when the asset has maximized its value and we are able to redeploy proceeds into higher and better returns in other assets, sectors and markets, including office buildings.”

As Bloomberg notes, the pension fund isn’t actively backing away from offices, but it’s not looking to increase its office holdings either. And where a property requires additional investment, CPPIB might simply look to sell so it can put that cash somewhere it can get higher returns instead, said the person, who asked not to be identified discussing a private matter.

CPPIB’s C$590.8 billion ($436.9 billion) fund is one of the world’s largest pools of capital, and its C$41.4 billion portfolio of real estate — stretching from Stockholm to Bengaluru — includes almost every property type, from warehouses, to life sciences complexes, to apartment blocks.

While that scale would mitigate any potential losses from individual transactions, it also means even a small shift in CPPIB’s office appetite has the power to cause ripple effects in the market.

While the 360 Park liquidation may be shocking, it’s just the first of many: with hybrid work schedules set to depress demand for office space in the long term, and higher interest rates increasing the cost of the constant upgrades needed to attract and keep tenants, even the best office buildings may not be able to compete with investment opportunities elsewhere.

“To get even better returns in your office investment you’re going to have to modernize, you’re going to have to put a lot more money into that office,” said Matt Hershey, a partner at real estate capital advisory firm Hodes Weill & Associates. “Sometimes it’s better to just take your losses and reinvest in something that’s going to perform much better.”

Tyler Durden

Wed, 02/28/2024 – 22:40