SuperCore Inflation Soars In January, Services Costs Re-Accelerate

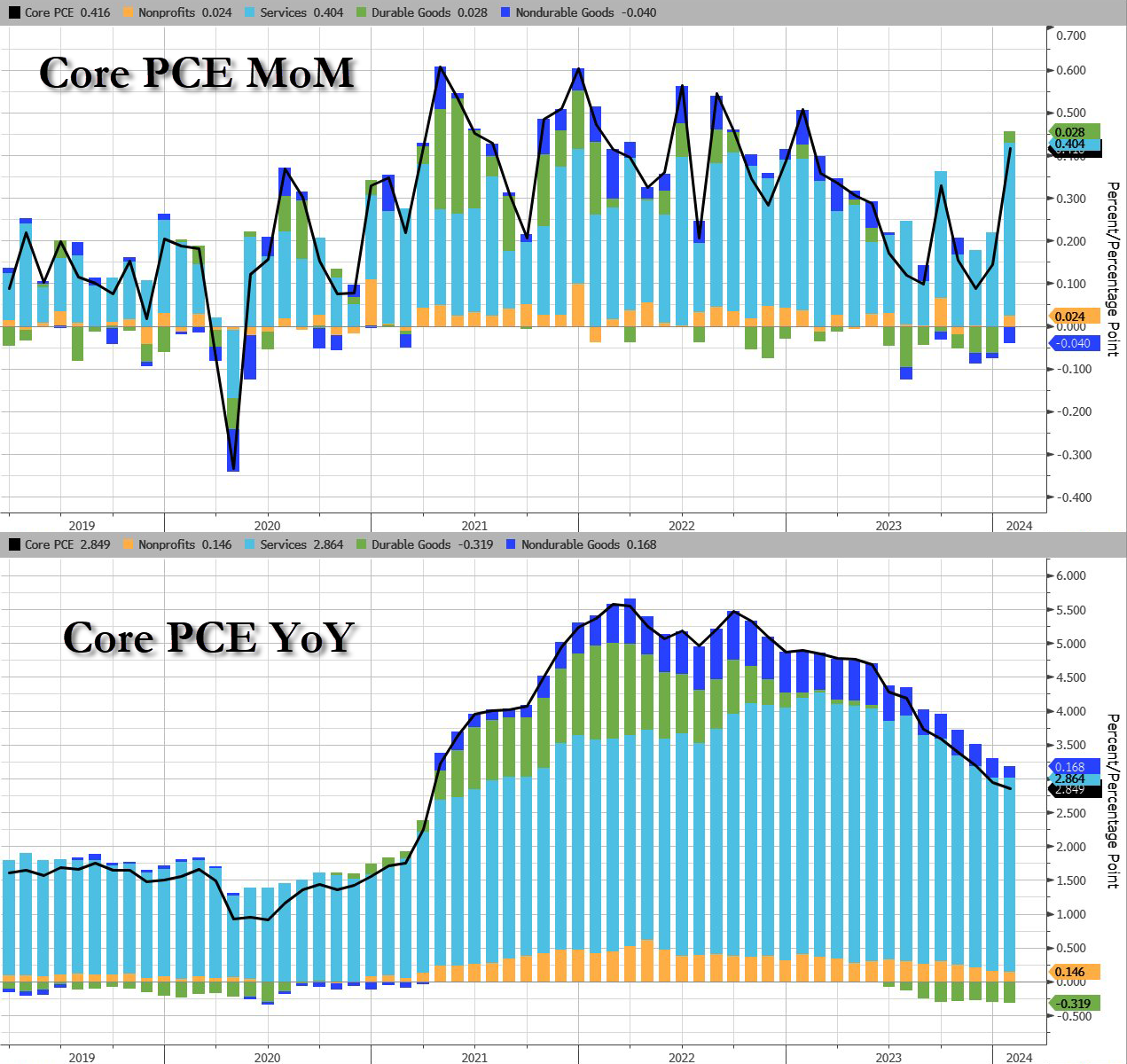

GOOD NEWS… One of The Fed’s favorite inflation indicators – Core PCE Deflator– dropped to +2.8% YoY in January (as expected) – the lowest since March 2021.

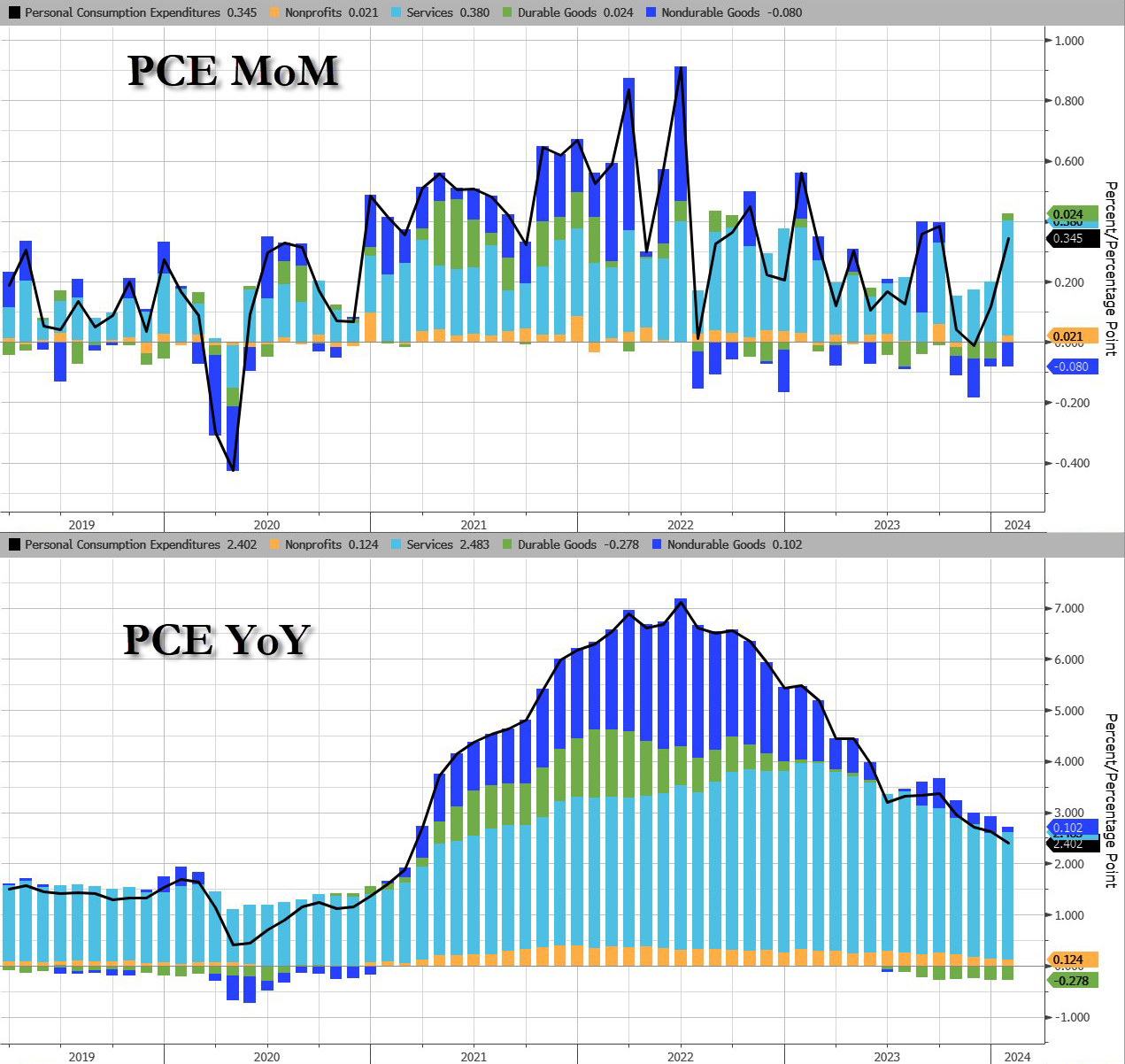

Headline PCE Deflator rose 0.3% MoM as expected, down at +2.4% YoY in January …

{kind=link}

Source: Bloomberg

BUT… Services soared on a MoM basis…

{kind=link}

However, shorter-term signals are less encouraging:

Core PCE 3M annualized rate 2.8% from 2.0%

Core PCE 6M annualized rate 2.6% from 2.2%

On a core basis, services costs jumped even more and Durable Goods costs flipped from deflation…

{kind=link}

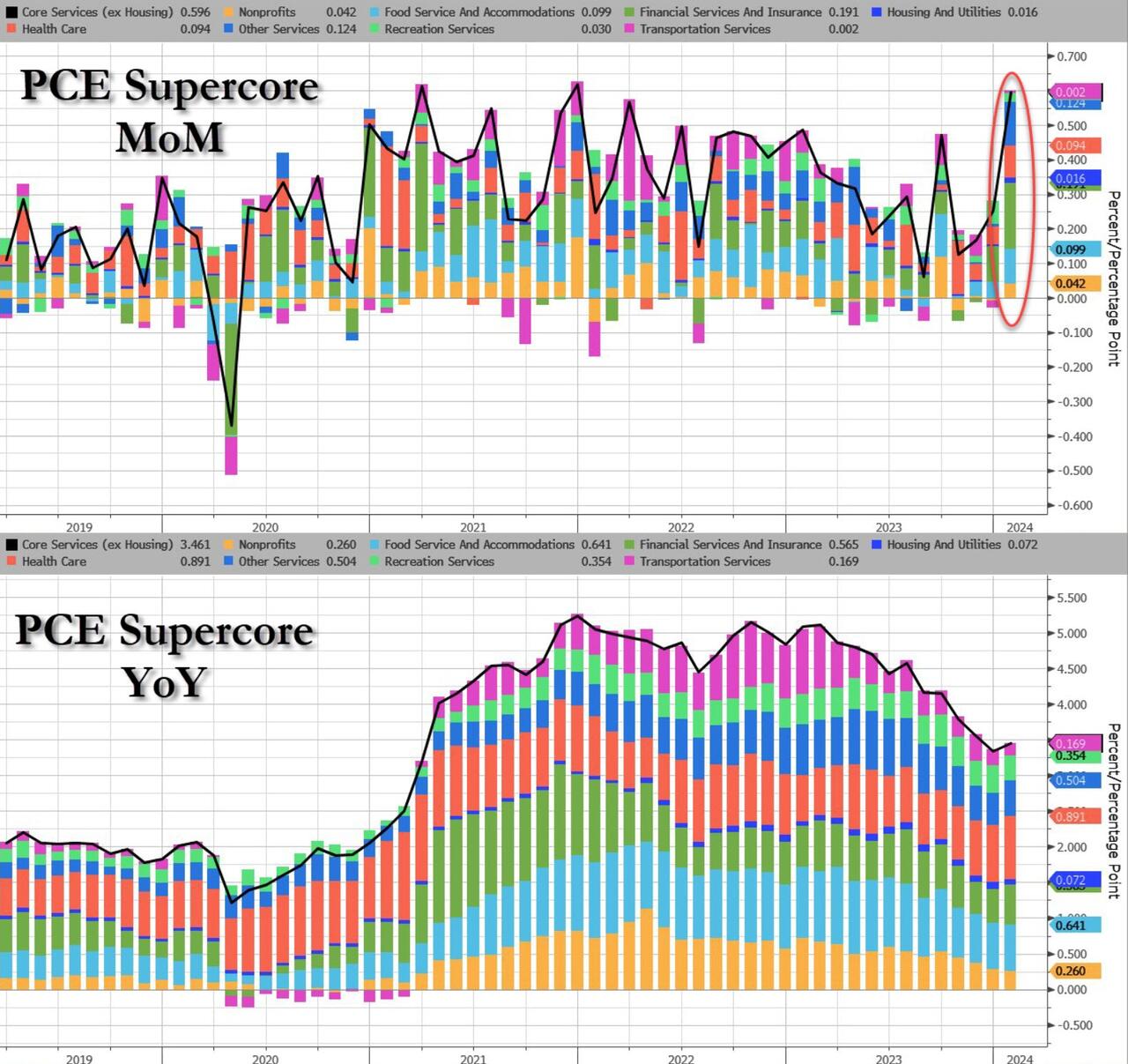

BAD NEWS… Even more focused, from The Fed’s perspective, is Services inflation ex-Shelter, and the PCE-equivalent actually ticked up on a YoY basis to 3.45%, thanks to a large 0.6% MoM jump, considerably bigger than the last few months increases…

{kind=link}

Source: Bloomberg

Under the hood, the SuperCore, every sub-element rose MoM…

{kind=link}

Source: Bloomberg

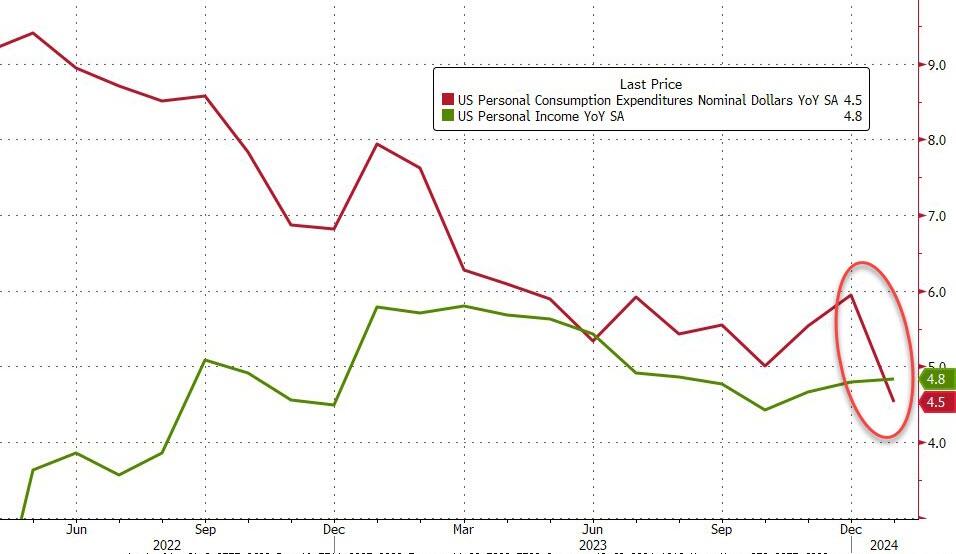

Income and Spending both increased with the former soaring 1.0% MoM (+0.4% exp) but the latter up only 0.2% (in line)…

{kind=link}

Source: Bloomberg

Most notably, spending is now rising at a slower pace than incomes on a YoY basis (spending growth at the lowest since Feb 2021)…

{kind=link}

Source: Bloomberg

On the income side, Govt wage growth slumped from a record 8.8% in Dec to 7.8% in January

Of course, private wages also dropped to 5.4% in Jan from 5.6% in Dec

{kind=link}

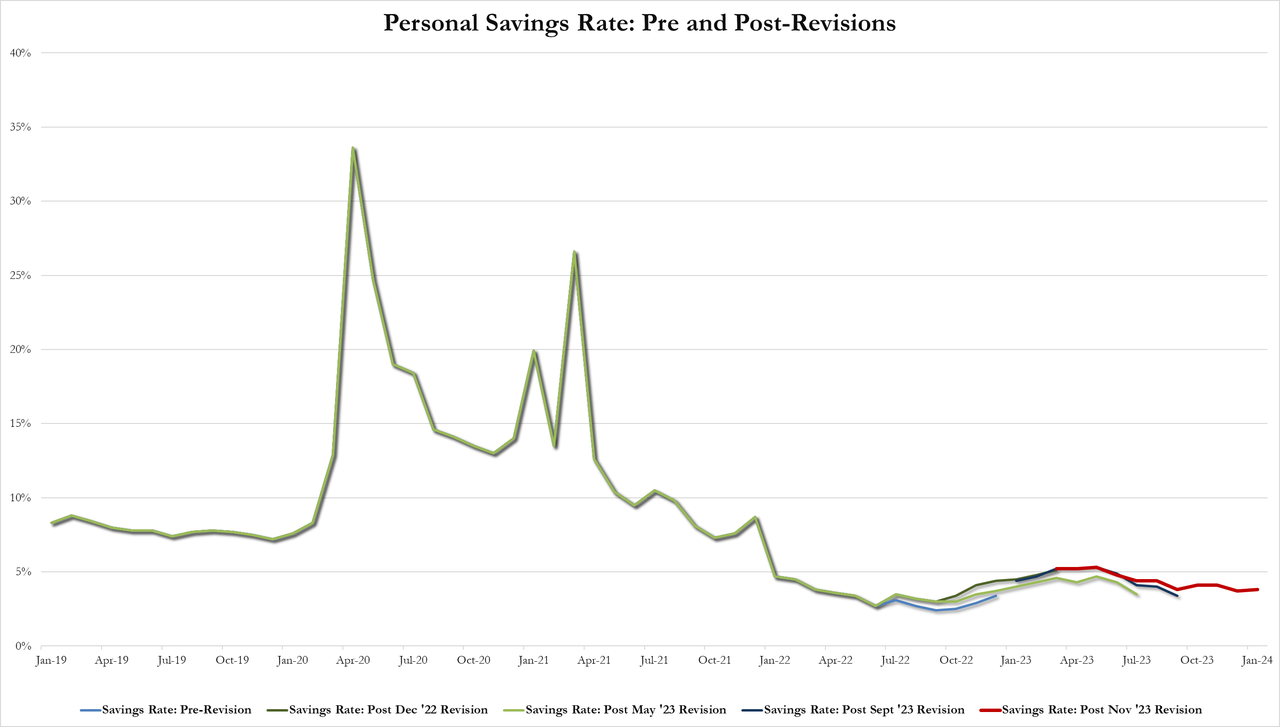

January savings rate rose to 3.8% (from 3.7%)…

{kind=link}

Finally, while the markets are exuberant at the headline disinflation, we do note that it’s not all sunshine and unicorns.The vast majority of the reduction in inflation has been ‘cyclical’…

{kind=link}

Source: Bloomberg

Acyclical Core PCE inflation remains extremely high, although it has fallen from its highs.

Is The (apolitical) Fed really going to cut rates 4 times this year with a background of strong growth (GDP) and still high Acyclical inflation?

Tyler Durden

Thu, 02/29/2024 – 08:45