No Asset Class Is Remotely Ready For More Inflation

Authored by Simon White, Bloomberg macro strategist,

Stocks, bonds, commodities and other real assets are dramatically unpriced for a resurgence in inflation.

If fortune favors the prepared, then no market is going to have much luck.A re-acceleration in inflation is increasingly on the cards (see here), an eventuality that is materially underpriced across asset classes. That means portfolios are cheap to hedge, as well as leaving markets subject to outsized moves when they do price in inflation’s return.

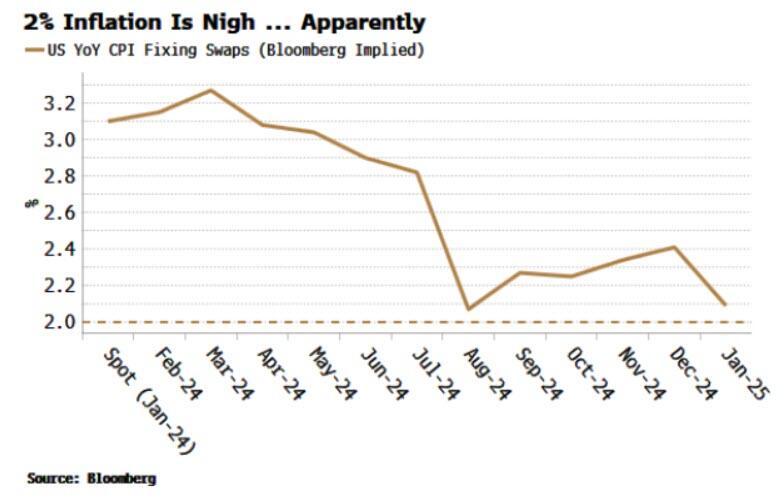

Inflation complacency can be seen clearly in one chart. CPI fixing swaps foresee a continued steady decline in headline inflation in the US back toward 2% through this year. Not only that, most of the swaps have been falling in recent months as spot inflation has eased. The implied probability of a return of inflation is dwindling to zero.

{kind=link}

But it’s not just fixing swaps predicting a return to inflation utopia. Across markets, there are indications that are not only underpricing a revival in price growth, they appear to be ignoring the possibility altogether:

nominal yields with negative inflation risk premium

real yields with low downside skew

low expectation of much higher short-term rates

high exposure to equity sectors with steep duration

low exposure to the sectors best placed to weather inflation

commodity volatility that’s very subdued

ownership in commodities that is at histrocial lows

The charts will do most of the talking. Start with nominal yields. We can decompose them (via the DKW model) into a real expected short-rate, real term-premium, expected inflation and inflation term-premium (aka risk premium).

The drop in the 10-year yield from its October high has been driven by a fall in the real expected short-rate, as well as a decline in expected inflation. But there is nothing built into the price for inflation’s volatility rising again, as it typically does when price pressures increase. In fact, the inflation risk-premium is more negative than it was in the years leading up to the pandemic.

{kind=link}

Real yields too are bereft of any risk premium for inflation. If the Federal Reserve does not immediately react to rising inflation (as happened in 2021, and I suspect will happen this year if and when inflation starts to pick back up), real yields are likely to experience downside volatility, i.e. call skew for TIPS should rise. Again there is no sign of market nerves here.

{kind=link}

As the chart above shows, TIPS call skew has tended to lead inflation over the last few years, and thus there is little in the way of rising price growth expected soon. The inflation-bond market may have this one wrong.

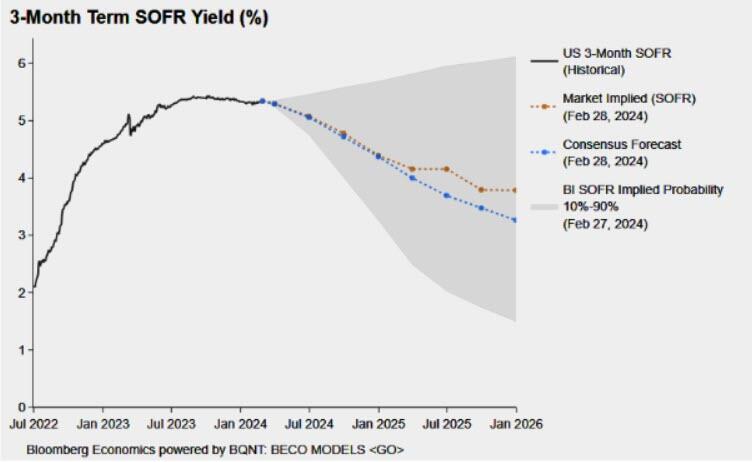

Short-term rates don’t look any better. The market is still expecting lower rates over the next year, which might make sense from a weighted-average perspective given that when things go wrong (e.g. a recession) they go violently wrong. But there is little likelihood priced in for much higher rates – the distribution for SOFR rates has a clear downwards skew.

{kind=link}

Overall, bond investors just aren’t anticipating more inflation,with the number of investors who say they are short USTs in JPMorgan’s Treasury survey plumbing its series lows.

{kind=link}

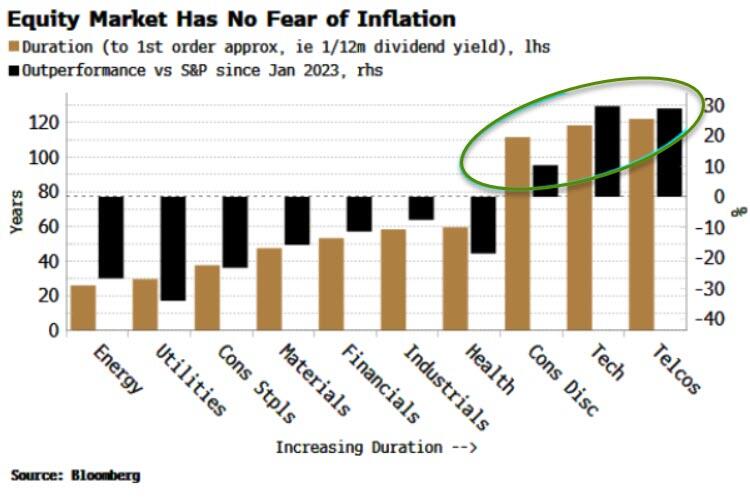

Stocks are also very much on Team Transitory (and we can make similar arguments for credit). There continues to be a bias toward high-duration sectors (which are more likely to fare worse when inflation is high), such as tech and telcos, with these strongly outperforming the index.

On the flipside, the sectors with historically the best record when inflation is elevated are those with low duration such as energy and staples, which continue to lag heavily behind.

{kind=link}

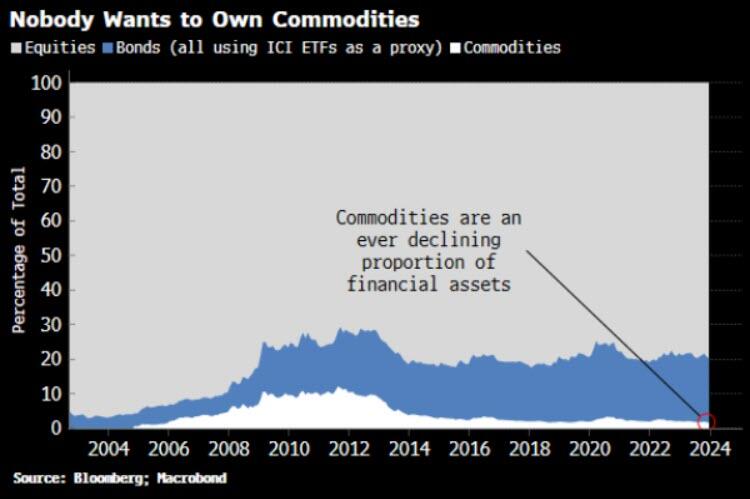

Bonds, and stocks in the main, are assets to avoid (or short) when inflation is troublesome, but commodities and other real assets are havens. But here as well, there is no sign investors are making hay while the disinflation sun is shining. Commodity ownership relative to stocks and bonds continues to fall, and now represents only a measly 1.7% of the total.

{kind=link}

That’s not just down to valuation effects, given commodities are now 30% lower than their 2022 peak, but due to real outflows from the asset class (using commodity ETFs as a proxy).

It could be the calm before the storm. Implied volatility in several commodities, mainly in metals, has been falling and is near 10-year lows. Lead, copper, nickel and most notably gold and silver are within ten percentage points of their vol troughs over the last decade.

{kind=link}

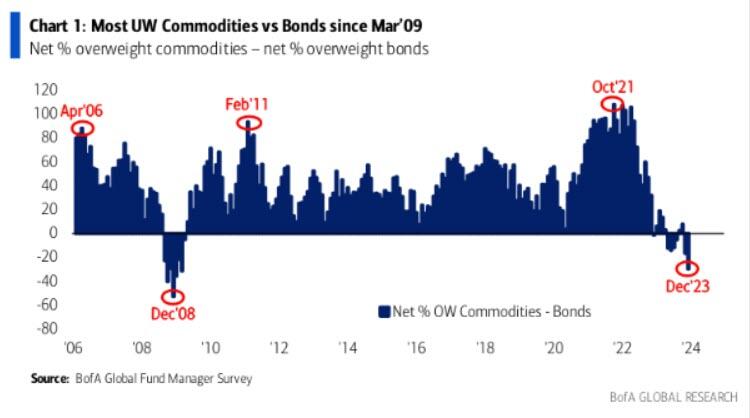

Again, why own real assets over financial assets when you think inflation is yesterday’s story?That’s reflected in BofA’s Global Fund Manager Survey from December, showing the biggest underweight in commodities versus bonds since the post-GFC equity-market bottom in March 2009.

{kind=link}

Source: Bank of America

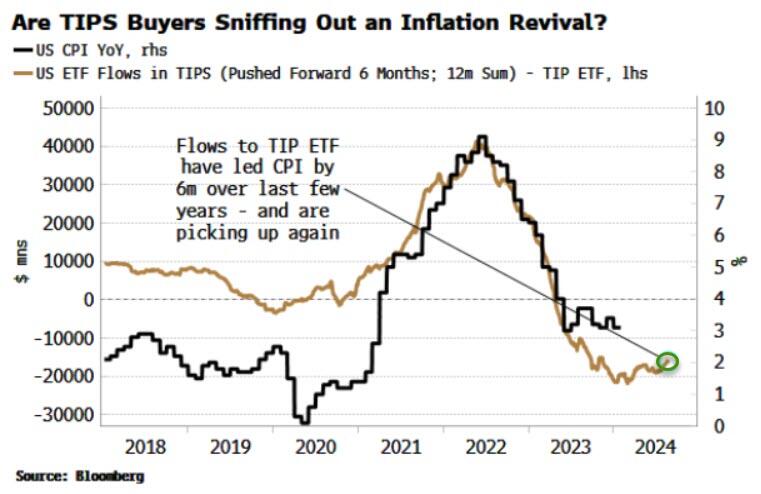

Just maybe though there is one market sensing price growth is returning and is moving to hedge it. I mentioned above TIPS skew did not appear to be anticipating an inflation-driven lurch lower in real yields. But inflows into TIPS ETFs as a whole are slowly picking up. This had a good call in the pandemic, starting to rise about three months before CPI started its ascent in 2020 (when inflation leading indicators were already rising, as they are today).

{kind=link}

Either way, there are precious few signs a re-acceleration in inflation is being priced in even as much of a tail-risk across markets. Fortune favors the hedged — and at the moment, that’s exceedingly cheap to do.

Tyler Durden

Thu, 02/29/2024 – 08:05