Banks Increase Car Loan Rejections Over $1,000 Monthly Payment Concerns

As borrowers struggle with making their $1,000 monthly car payments, banks with auto financing units are swiftly adjusting to stricter credit conditions by turning down many prospective buyers, further complicating the process for consumers to secure auto loans.

According to Bloomberg, “That’s freezing out buyers with lower credit scores who can’t afford a large down payment, while Americans with healthy finances are having more trouble than usual securing loans.”

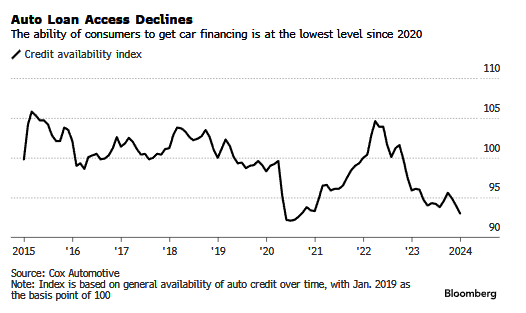

New data from Cox Automotive shows access to auto credit has tumbled to the lowest level since August 2020. The approval rate for loans is down 1.6% year-over-year.

{kind=link}

Meanwhile, data from the New York Federal Reserve shows the percentage of auto loans 90 days or more delinquent rose above pre-pandemic levels to 2.66% in the fourth quarter of 2023. That compares to 2.37% at the beginning of 2020 and a 15-year average of 2.16%.

“What people are struggling with is the level of inflation causing them to have to juggle expenses and try to stay current on their loans,” said Jonathan Smoke, chief economist for Cox Automotive.

Smoke continued: “It’s produced some very alarming statistics that indicate risk has grown in an environment in which lenders have become more risk-averse.”

This is why banks have a very cautious view of the consumer as the era of Bidenomics fails.

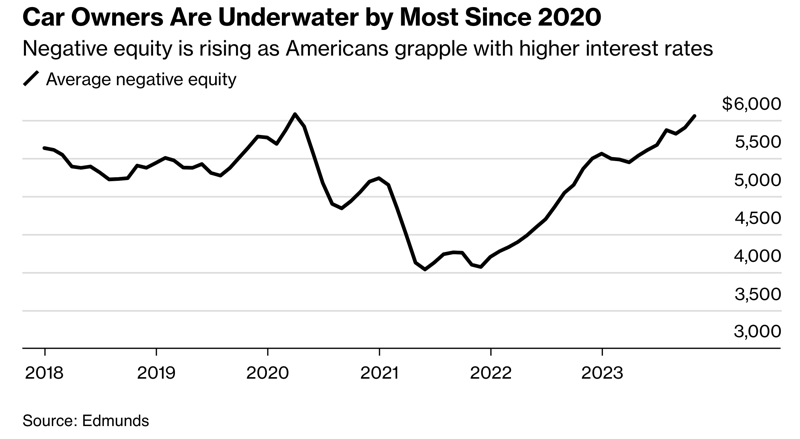

And this also comes as a recent Edmunds report showed the number of consumers with auto loans “underwater” or “negative equity” hit levels not seen since April 2020.

{kind=link}

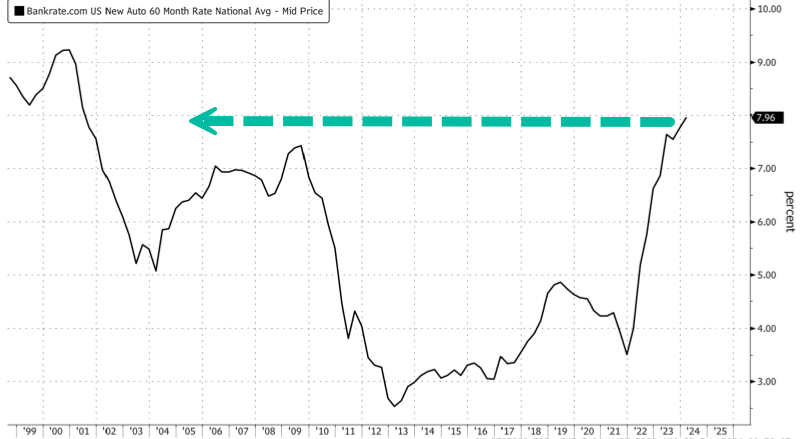

“It’s a precarious spot for many Americans, coming after a twin surge in car buying and interest rates has strained finances and fueled an uptick in automobile repossessions,” Bloomberg recently explained. The average rate for a new auto loan with a 60-month term via Bankrate data nears the 8% mark, or the highest level since the Dot Com bust.

{kind=link}

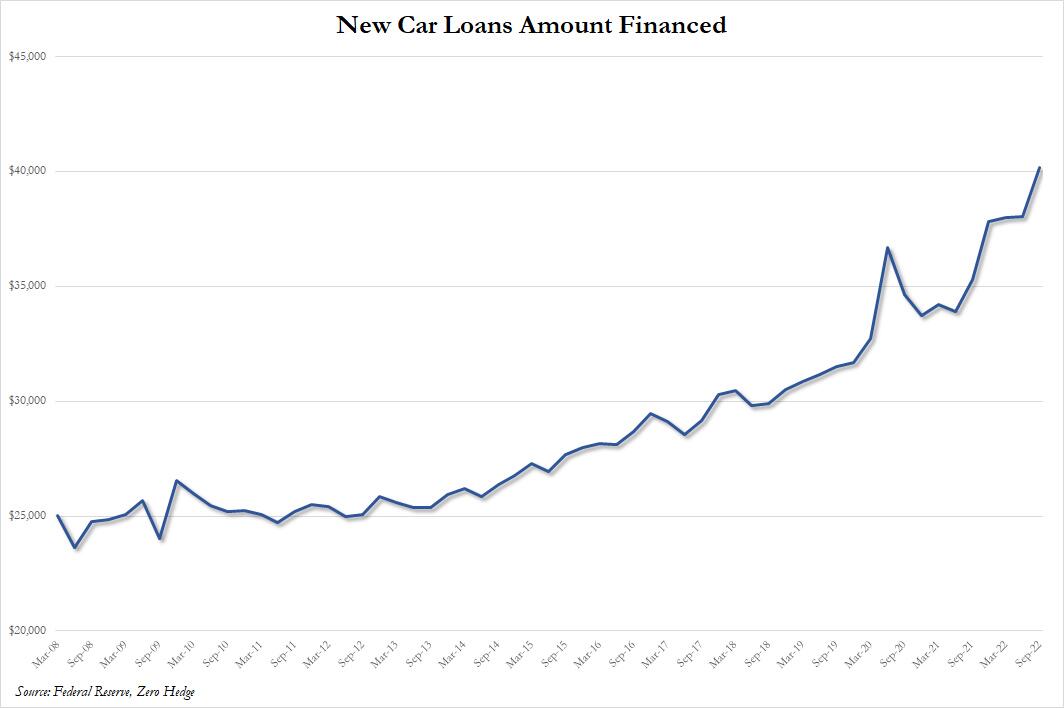

Last year, when discussing the “perfect storm” hitting the US auto market, we showed that according to Fitch, “More Americans Can’t Afford Their Car Payments Than During The Peak Of Financial Crisis“… The average new car loan has reached a record high of $40,000.

{kind=link}

And weeks ago, we penned a note showing how some dealers put consumers with likely poor credit into vehicles with payments comparable to mortgage payments of a small home.

{kind=link}

The auto financing market is preparing for a downturn as low-tier consumers increasingly struggle with $1,000 monthly payments.

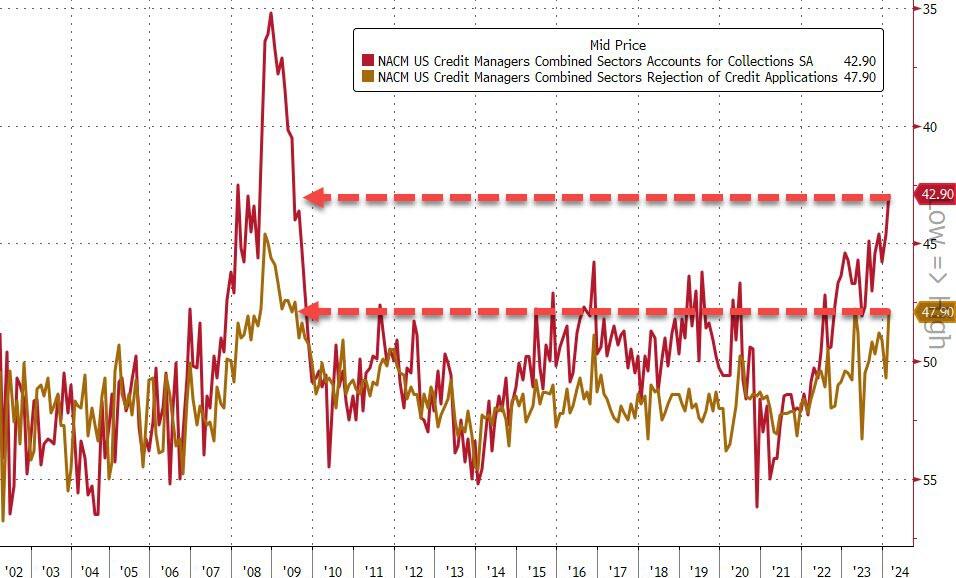

In the end-of-day market round-up on Wednesday, we shared with readers the Credit Managers’ survey that shows the rate of rejections for credit applications and the number of accounts moved to ‘collections’ is surging back to near GFC levels…

{kind=link}

… and about that ‘strong consumer’ narrative the Biden administration keeps pushing in corporate media.

Tyler Durden

Thu, 02/29/2024 – 14:20