Stock Bull Market Might Just Be Getting Started, But…

Authored by Simon White, Bloomberg macro strategist,

The rally in equities might have much further to go, based on the positive outlook for liquidity.

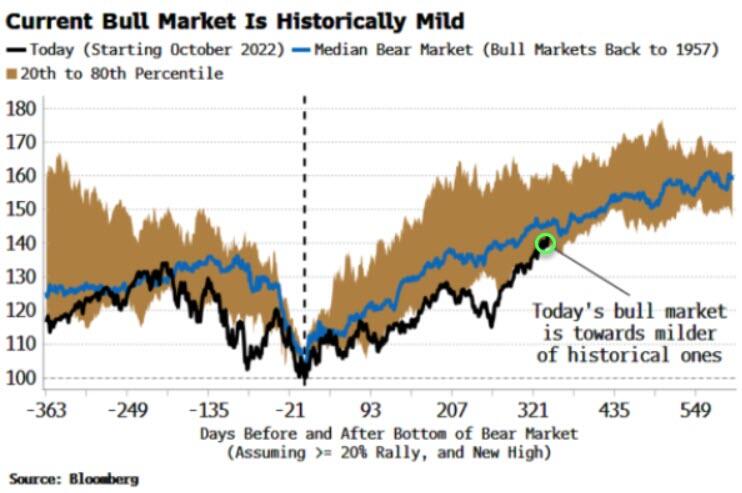

It might not seem like it after a seemingly relentless advance and fevered speculation, but the new bull market is comparatively mild versus the postwar past.

{kind=link}

Yet that could change. Excess liquidity – the difference between real money growth and economic growth – shows that the stock rally could have much further to go, turning a so-far historically below-par bull market into one that’s above the past average.

There are many reasons why this might not transpire…

As a natural cynic, I’m more comfortable when the outlook is pessimistic (no room for disappointment) versus when it is optimistic (plenty of opportunity to end up with egg on your face when things do go wrong after all). But sometimes the data just isn’t there to support a downbeat view.

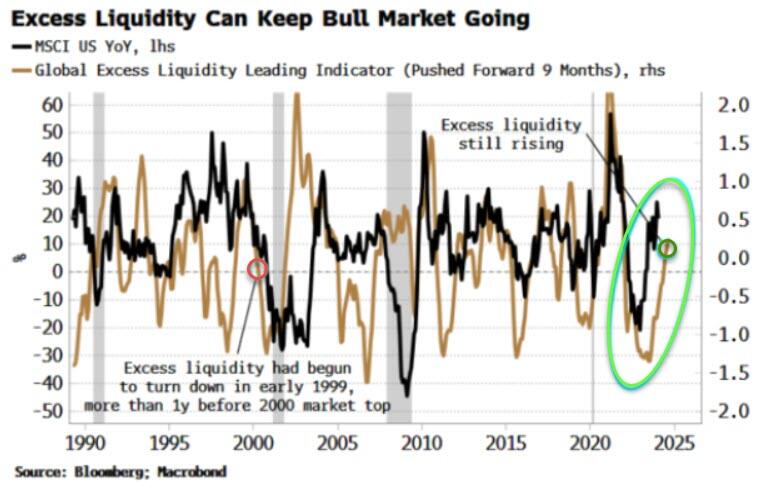

That’s the case today. One of the best medium-term drivers of stock returns is excess liquidity. It’s an intuitive measure: when money, which is created by banks and central banks, is growing faster in real terms than GDP, liquidity is left which is “excess” to the needs of the real economy, and which thus tends to find its way into risk assets.

After beginning to rise in the first half of last year, and supporting the equity rally that began in March, excess liquidity has continued to rise. It is difficult for markets to sell off significantly when there is plenty of risk-asset-supporting liquidity sloshing around the system.

{kind=link}

Fiscal and monetary policy are conspiring to keep excess liquidity climbing despite the cumulative impact of higher rates coursing through the economy.

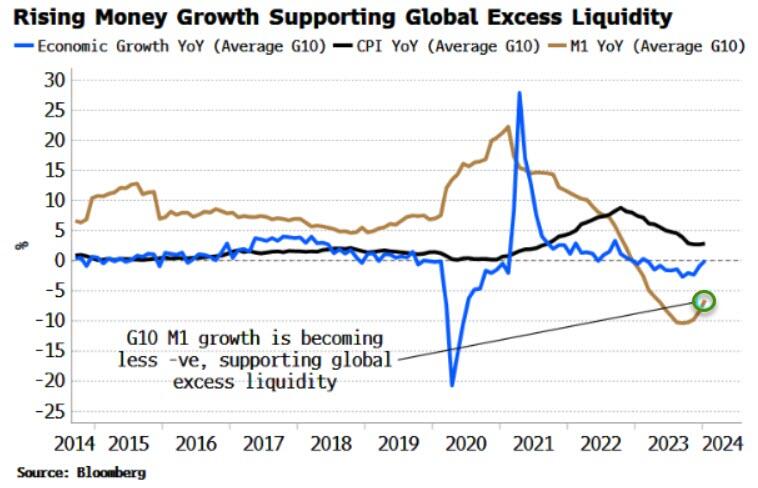

First, what has been driving excess liquidity so far?

It has three main elements: inflation, economic growth and narrow money, with the latter responsible for most of the measure’s rise over the last year.

{kind=link}

But that’s not the full picture.

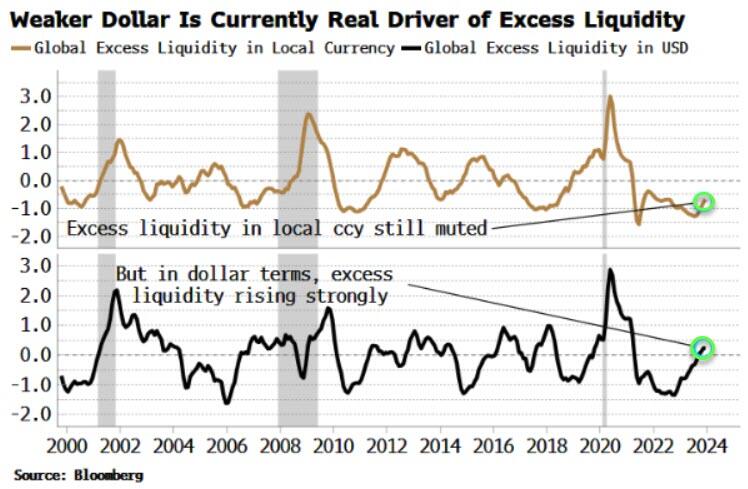

Excess liquidity is a global measure, made up of the money and economic growth of countries in the G10, in dollar terms. That means a weaker dollar boosts non-US excess liquidity.

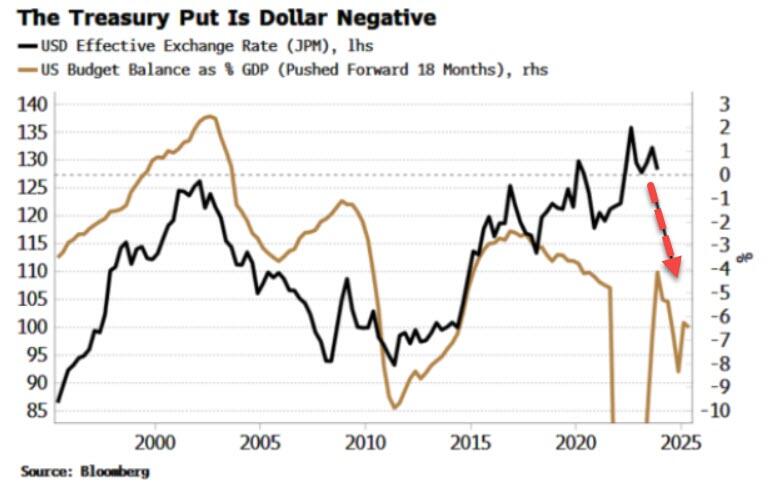

As the chart below shows, it’s the weaker dollar – down over 9% from its September 2022 highs – that has been the biggest driver of excess liquidity.

We can blame fiscal policy here. The US’s expansive deficit has been one of the most important longer-term negative influences on the dollar. There is little sign the deficit is about to improve by much, based on (no doubt conservative) Congressional Budget Office forecasts. Government finances are also unlikely to be straitened whoever the next president is, meaning the primary trend in the dollar (DXY) is likely to remain down.

{kind=link}

{kind=link}

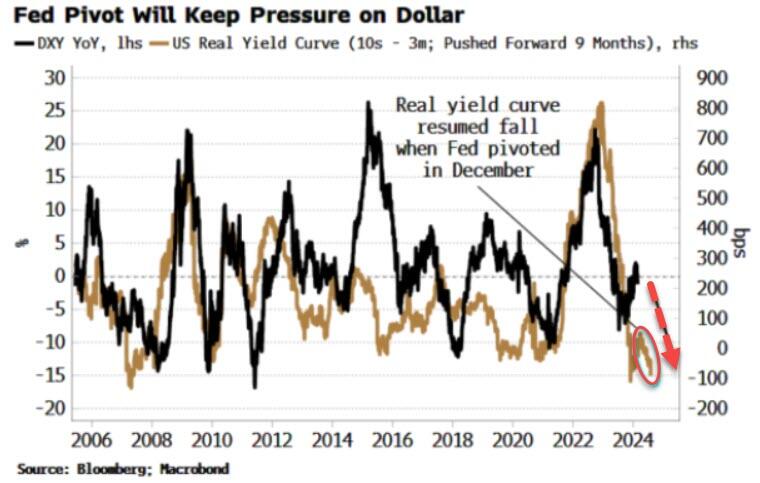

We can also blame monetary policy for the dollar’s malaise and excess liquidity’s buoyancy. The latter looked like it was about to start turning lower last year, but was saved in the nick of time by the Federal Reserve’s pivot in December.

How? On a shorter-term basis (6-9 months), the dollar is led by the real yield curve. The US currency is driven at the margin by the real return of foreign investors in long-term US assets. In the latter months of 2023, the real yield curve had been steepening, as longer-term real yields were rising more than shorter ones.

Then the Fed came with its still unfathomable pivot. Shorter-term real yields fell, but their longer-term counterparts fell by more, and the curve re-flattened. What was a strong supportive sign for the dollar returned to being a weight on it – and thus a continued tailwind for excess liquidity.

{kind=link}

It’s not just liquidity that could charge the bull market further.The absence of a US recession, which continues to look off the cards for the time being, also bolsters the case that equities should not soon face a steep selloff. Traditional recession indicators have been misleading in this pandemic-addled cycle, but it has become increasingly clear a downturn in the US is now less likely than not.

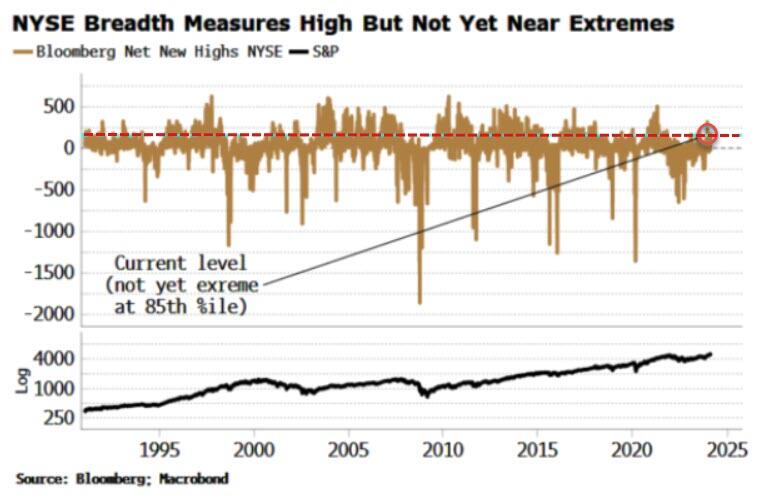

Furthermore, the rally might be on shakier legs if sentiment and technicals were overly bullish, but they are not yet historically stretched. The net number of stocks making new 52-week highs, the number trading above their 200-day moving average or their upper Bollinger band, and the advance-decline line are all high but have been higher. Moreover, sentiment is net bullish but not at extremes, while retail allocation to stocks is only at its 5-year average.

{kind=link}

Leadership is narrow, with only a handful of stocks driving the advance, but there is little historically to show that this leads to sub-par returns.And when markets eclipse new highs, as the S&P did a few weeks ago, it acts as a psychological all-clear that we are indeed in a new bull market. Whether you agree that’s justified or not, the catch-up money that floods the market creates its own momentum.

No bull market comes without risks and this one is no different. The biggest is a recession.While, as mentioned above, that does not look likely in the near term, a sudden and unanticipated economic slump (either endogenous or due to an exogenous shock) would decimate returns. Also, a bull market that does not begin either during a recession or within 18 months of one is unusual, with only one postwar example (1966).

Equities experience their largest drawdowns in recessions, and given there is little ex ante to indicate one is coming in the current environment, it would likely be particularly devastating.

A blow-off top is another risk.Even then, despite the upset one would cause, it might not be enough to kick-start a new bear market. Inflation, too, will pose a risk to stocks, but to their real returns, unless price growth’s revival is particularly abrupt or steep (bull and bear markets are, sub-optimally, based off nominal returns). A persistent bear-steepening of the yield curve would be the sign the rally is at risk.

To misquote John Templeton, bull markets are born on pessimism, but they grow on liquidity. As long as excess liquidity is supported, the market is primed to keep grinding higher, regardless of how cynical you might be.

Tyler Durden

Tue, 02/27/2024 – 14:40