Will Resurgent Inflation Savage The Tech Trade

By Simon White, Bloomberg Markets Live reporter and strategist

Equity markets are facing mounting concentration risks as just a handful of stocks drive returns. Not only that, the mainly tech-related names dominating the move are highly exposed to inflation which is on the precipice of re-accelerating. Investors face potentially steep downside, but it is possible to build a portfolio of companies well placed to weather a resurgence in price growth.

When one company’s earnings have the ability to influence the macro narrative and materially affect the $43 trillion S&P, it’s clear the threats from narrow breadth are elevated.Nvidia’s results, released on Wednesday evening, may have exceeded expectations and are on the cusp of taking the index to new highs, but that only underscores the reality the tech-heavy market leaves portfolios acutely exposed to inflation. This should be a clarion call that it’s time to act. What better time to fix the diversification roof than when the disinflation sun is still shining?

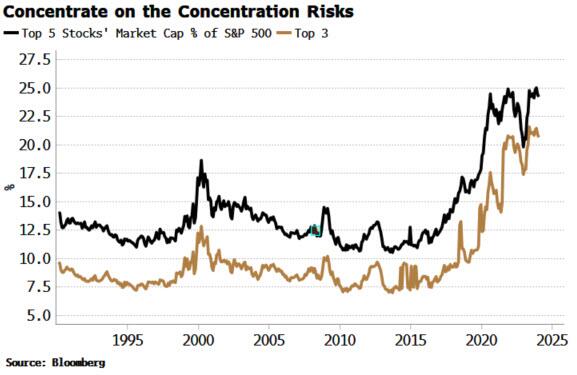

Concentration risks are at 50-year highs. The top five stocks in the in the S&P 500 now account for over a quarter of its market cap, from only about an eighth a decade ago. You have to go back to the time of the Nifty Fifty in the late 1960s and early 70s to see leadership as narrow as it is today.

{kind=link}

Back then, it was the tech titans of the day — Xerox, IBM, Polaroid– that were among the few stocks disproportionately powering the advance. And in what could prove to be an omen for the current cycle, the Nifty Fifty’s fate was sealed by rising inflation, which triggered the most brutal bear market seen since the Great Depression.

It’s even more of a problem today as tech companies have high duration, leaving them singularly vulnerable to a revival in price growth. A greater proportion of cash flows in the future leaves a stock’s total present value at risk from higher real rates.

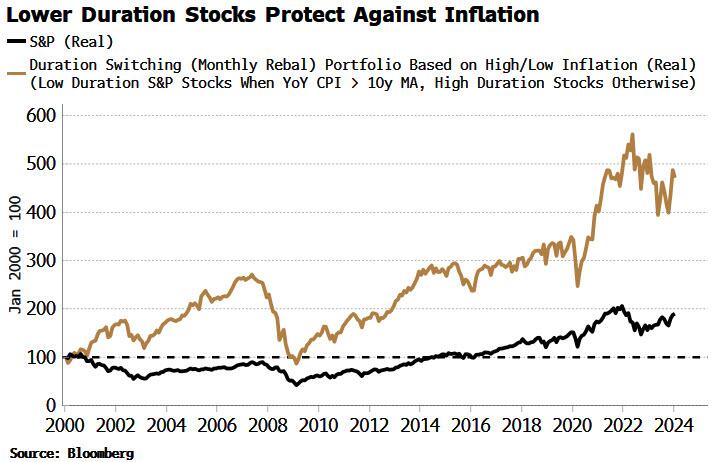

The benefits of avoiding high-duration stocks when inflation is elevated can be seen in the chart below. The blue line shows a rebalancing strategy that goes long low-duration stocks when US CPI is over its 10-year moving average, and high-duration stocks when inflation is under it (using the inverse of the dividend yield as an approximation for an equity’s duration).

As we can see, the strategy cleanly outperforms the S&P in real terms.

{kind=link}

But we can do better than that. It’s possible to build a portfolio of stocks resilient to inflation that’s not just dependent on their duration. After all, it’s a pretty blunt instrument. Ideally we want to find stocks that should do well if inflation re-accelerates (as I expect it will – see below), but is not fully reliant on that outcome.

Companies that are capital light and have strong pricing power should be well-placed to weather – if not prosper in – elevated inflation. The companies should also have demonstrated real growth over the long term.

More specifically, screen for companies with:

over $1 billion market cap

real dividend growth and sales growth

low fixed costs

strong pricing power

reasonable valuations

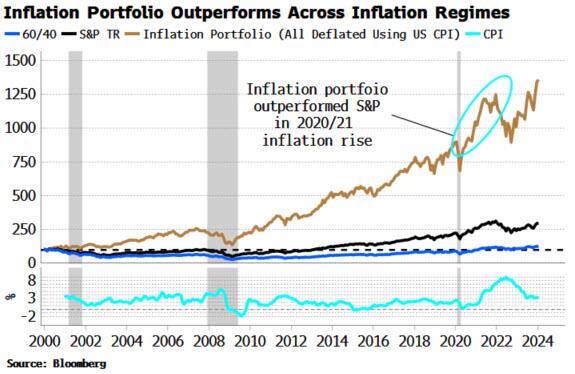

That gives us a portfolio of about 15-20 names which is rebalanced monthly. The real return of the portfolio is shown in the chart below, along with the real returns of the S&P and the 60/40 equity-bond portfolio.

{kind=link}

The portfolio is designed to be forward looking — the coming years are unlikely to look like the previous decades given we are now in an inflationary regime — seeking stocks that are robust to price growth that is above its long-term average and prone to lurching higher.

It is nevertheless reassuring to see that the portfolio does well on its backtest. It has outpaced the S&P in real terms over the last quarter century. It also outperformed in the rising inflation period during the pandemic. More generally, a strategy that went long the Inflation Portfolio when inflation was elevated, and long the market otherwise, fared better than the S&P over the last 25 years.

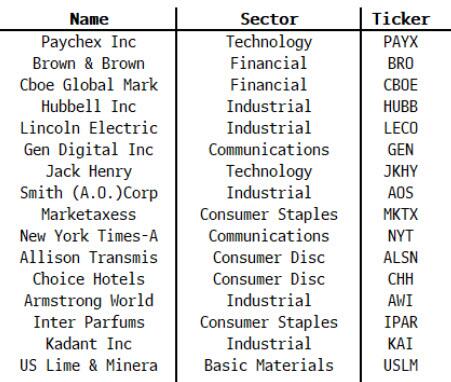

The current portfolio contains 16 names. All are good quality companies with most having reasonable valuations, the average P/E ratio being equal to the market’s. Only two are tech companies.

{kind=link}

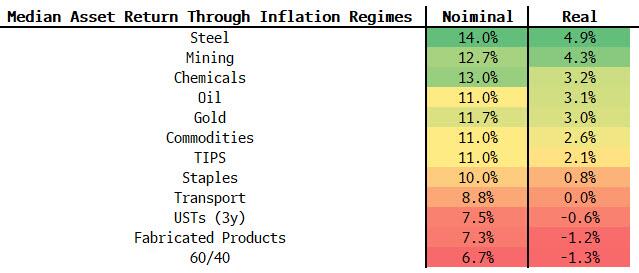

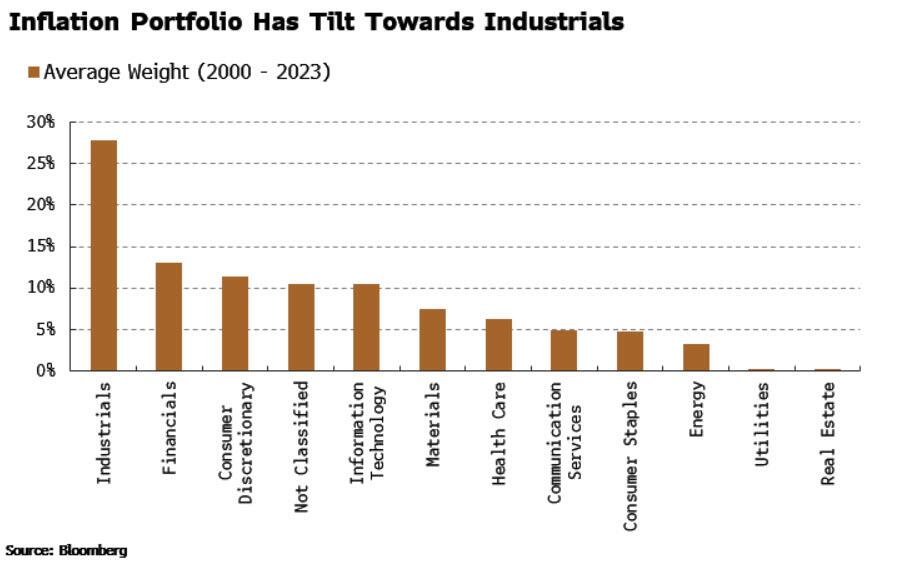

The most common grouping is industrials. Again, this is reassuring as in inflation regimes over the last five decades, the top performing sectors were steel, mining and chemicals.

{kind=link}

Through the life of the portfolio (2000-2023), industrials has had the largest average weight, followed by financials.

Banks are generally not a good holding when inflation is high as they typically lend long and borrow short, and see the real value of their assets decline more than their real liabilities. But there are several non-bank financials, such as the CBOE (in the portfolio now) and MSCI, which are quality firms with strong pricing power who stand in good stead when price growth is elevated.

{kind=link}

None of this would be necessary if inflation was going the way Team Transitory think it already has. But there is a mounting body of forward-looking indicators that expect inflation should soon re-accelerate. We may have already got a glimpse of this with the most recent hotter-than-expected CPI and PPI reports.

{kind=link}

Still, with any portfolio screening strategy there are caveats. There are turnover and price-slippage costs that could materially affect the realized return. There is also, of course, no reason why the backtested past should look like the future.

Nonetheless, the deep concentration of high-duration stocks leaves the market as exposed to inflation as it has been since the early 1970s. The potential downside justifies a different approach that tries to mitigate inflation risks without becoming overly dependent on them.After all, we may soon find that the Magnificent Seven’s name sounds just as ironic as the Nifty Fifty’s.

Tyler Durden

Thu, 02/22/2024 – 15:45