FOMC Minutes Preview: So About That Rate Cut…

Submitted by Newsquawk

SUMMARY:

The FOMC minutes will likely echo recent Fed Speak, which has pushed back on the probability of a Fed rate cut in March with the Fed stressing a gradual and patient approach. The hot January economic data (NFP, CPI, PPI) has vindicated the Fed’s efforts to push back on aggressive rate cut expectations, although many analysts highlight the recent trend down in inflation has not changed, and of course, it was just one month’s data, which also included rather soft retail sales which could pose some growth concerns.

The minutes will likely detail the reasoning on why the FOMC decided to push back on March, but it is worth highlighting the minutes only incorporate information that was available to the Fed at the time of the January 31st meeting, so the aforementioned data will not be alluded to in the minutes given it was all released in February.

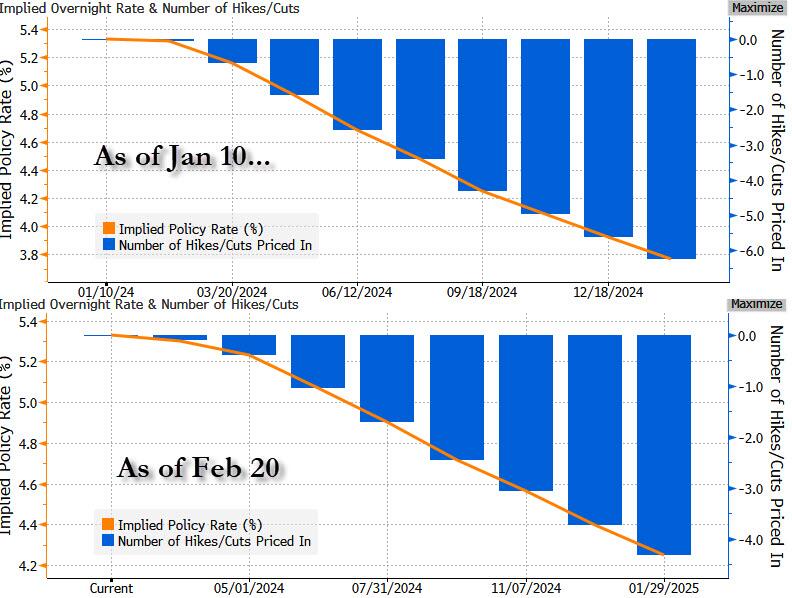

Nonetheless, the recent data has moved money market pricing to be more aligned with the Fed’s dot plot projections from December, which pencilled in three 25bp cuts in 2024 vs the three-to-four 25bp cuts the market is currently pricing – as opposed to between five-to-six earlier this year.The main question participants will be looking for clues on within the minutes will be when the FOMC expects to start the rate cut cycle, with markets fully pricing in the first cut by June, with a c. 40% probability of an earlier move in May.

{kind=link}

PRIOR MEETING:

At its January meeting, the Fed left rates unchanged at 5.25-5.5%, as expected, but made key changes to its statement, which now reflects a more balanced outlook on rate cuts vs rate hikes. The statement removed guidance that “in determining the extent of any additional firming that may be appropriate” to a more dovish/balanced view that “in considering any adjustments to the target range”, but it added a hawkish caveat that it “does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably towards 2%.”

Its description of economic growth was upgraded, now describing economic activity as “expanding at a solid pace”; its reference to the US banking system being “sound and resilient” and its commentary that tighter financial and credit conditions will likely weigh on the economy were both removed. It added a line noting that the risks to achieving its employment and inflation targets were moving into better balance.

At his post-meeting press conference, Chair Powell said the policy rate was likely at its peak for this cycle, and it would likely be appropriate to begin reducing rates “sometime this year” if the economy evolves as expected; he offered the caveat that the Fed was prepared to maintain its current policy rate for longer if needed. The Fed Chair said reducing rates too soon, or too much, could reverse the progress the central bank has made in lowering inflation, but at the same time, reducing rates too late could unduly weaken the economy. He judged inflation had “eased notably,” and that risks to achieving the Fed’s goals were moving into better balance. The Fed chief also added that low inflation readings in H2 2023 were welcome, but the central bank needs to see continued evidence in order to gain confidence that it was returning to target. Powell stated that a March rate cut was not likely, and was not policymakers’ base case.

Tyler Durden

Wed, 02/21/2024 – 12:45