China Markets Eye More Housing Support After LPR Surprise

By George Lei, Bloomberg Markets Live reporter and strategist

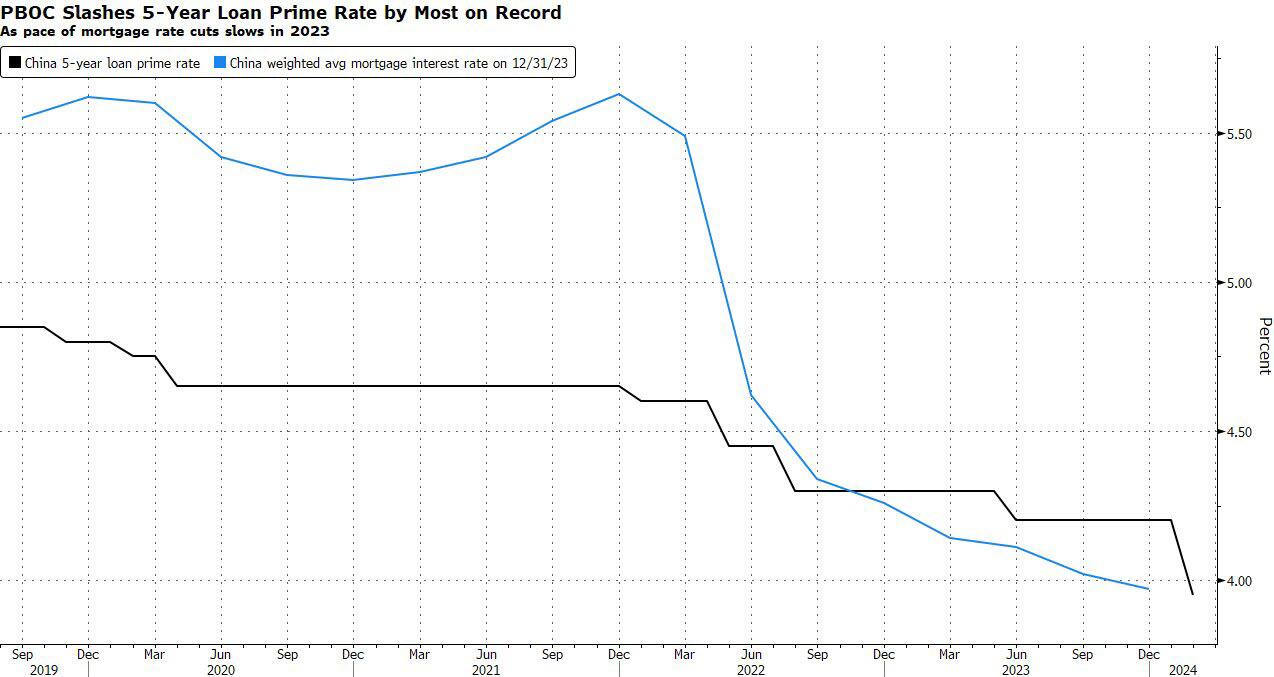

China slashed its five-year loan prime rate, a key reference for mortgages, by an unprecedented 25 basis points to a record-low 3.95% on Tuesday. While the move sends a strong signal from Beijing of aid for the property market, analysts caution that further monetary easing isn’t guaranteed and more support measures are needed for a turnaround in the housing sector.

Tuesday’s reduction signals Beijing’s continued preference for targeted easing and its desire to shore up the housing, Oxford Economics said in a research report, noting that one-year LPR, which doesn’t have any mortgage implications, is left on hold. The size of the cut reveals “a genuine concern” among policymakers that the “slow-drip of easing” implemented thus far “has had little impact,” Louise Loo, the firm’s lead economist, wrote.

While none of the 12 analysts polled by Bloomberg foresaw such a big LPR cut, the PBOC won’t necessarily lower other interest-rate benchmarks in a similarly aggressive fashion, according to JPMorgan. Uncertainty around the Fed’s next steps — with some speculation even of a hike — may prompt Beijing to pause further easing until more clarity emerges from Washington, according to Haibin Zhu, JPMorgan’s chief China economist. Any additional easing will also depend on the PBOC’s assessment of the consumer-price outlook, which appears more sanguine than that of markets, the US bank said.

Since early 2022, the PBOC has cut the five-year LPR by 70bps, while average mortgage rates have fallen by 152bp — thanks to bigger reductions early on by local banks. This is almost the same as the total reduction of 153bps in a five-year benchmark rate for all loans in 2008, but the difference is the speed of cuts, according to Pantheon Economics. Back then, mortgage rates dropped over a three-month period from October to December, resulting in a swift boost to market confidence.

{kind=link}

With mortgage rates drifting down over two years, a slow, grinding housing recovery remains the most likely scenario, Pantheon concluded. Moreover, the full effect of the LPR reduction could be limited as local lenders —now facing already thin margins — might choose to pass only a fraction of the latest cuts to potential home-buyers, wrote Ting Lu, Nomura’s chief China economist.

Beijing, therefore, will have to “do much more” to salvage housing projects and stabilize the market, the Japanese bank said. Moreover, the vast majority of borrowers will only feel the full impact of lower rates in 10 months time, Nomura noted. There are about 38 trillion yuan ($5.28 trillion) outstanding mortgages that reference the five-year LPR and by contract, rates are not going to reset until Jan. 1, 2025.

Tyler Durden

Tue, 02/20/2024 – 20:31