China Supercharges Stimulus With Biggest Cut In Mortgage Reference Rate On Record

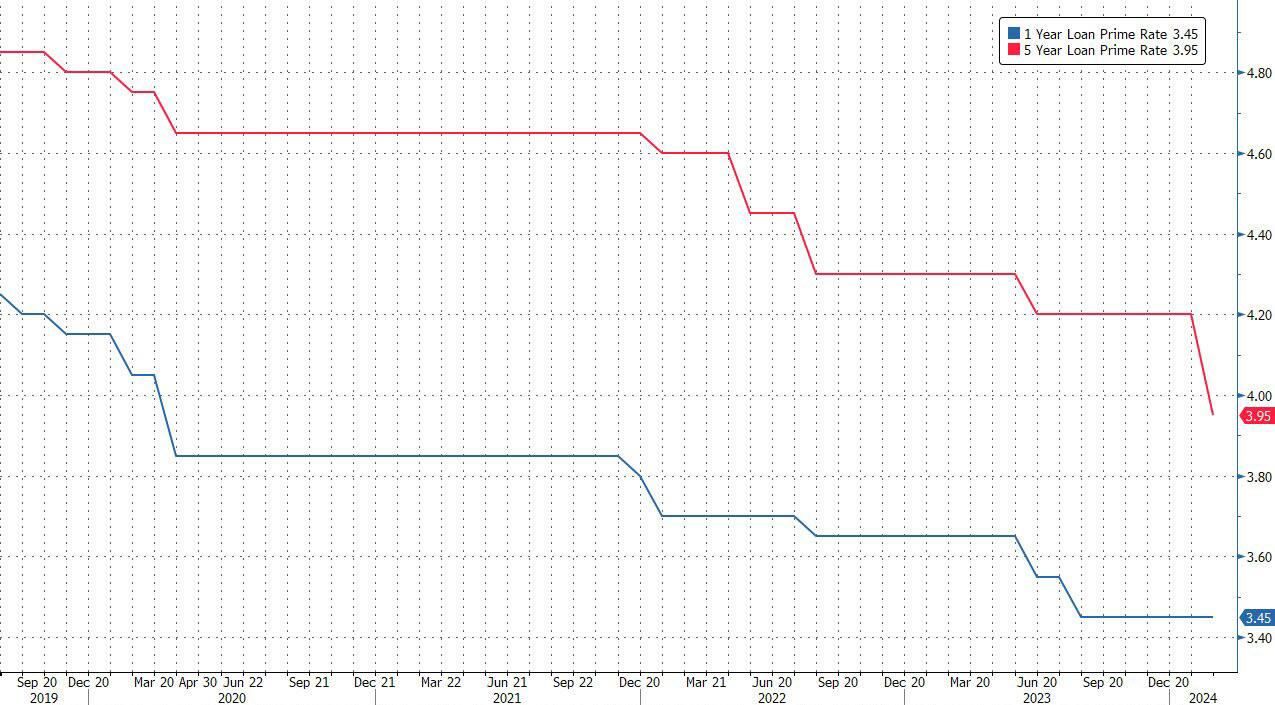

After the relentless jawboning in recent days, many were expecting some further easing today from the PBOC, and Beijing did not disappoint when China cut the 5-year loan prime rate (LPR) – which influences mortgage rate pricing – and is also known as China’s Libor (or rather SOFR since Libor no longer exists) by 25bp to to 3.95% on Tuesday, while holding the 1-year rate at 3.45%. The LPR cut is the largest since China revamped its loan pricing mechanism in 2019. China last trimmed the 5y LPR by 10bp in June 2023.

{kind=link}

As UBS notes, market sentiment should get a boost from the larger-than-expected 5y rate cut, with a Reuters poll estimating 5-15bp after the PBoC-backed Financial News reported Sunday that there’s downside room for LPRs, especially for 5y as it will support the real estate market.

Furthermore as noted earlier, Premier Li Qiang had called for “pragmatic and forceful”action to boost confidence in the economy on Monday.

Elsewhere, the PBoC kept the medium-term lending facility (MLF) rate on hold Monday. LPRs and MLFs usually move in tandem, but UBS Economist Ning Zhang had noted that a LPR cut should a bit earlier and more than MLF rate cut, thanks to previous cuts of reserve requirement ratio and deposit rates.

Commenting on the larger than expected cut, Derek Tay, head of investments at Kamet Capital Partners said that Chinese banks’ cut of a key reference lending rate for mortgages is “deeper than expected and shows that authorities are following through on their vows to boost the market and the economy.”It’s “also a relief that the authorities are proceeding as they have been foretelling regarding support for the economy and the market.”

Others were a bit more skeptical:

Hao Hong, an economist at Grow Investment:

Loan demand is very weak. So even if there is a large cut it won’t stimulate new demand plus the existing loans are still on the old rate

Now the problem is not about interest-rate levels. The real estate sector continues to ail. It is the sector that used to generate much of the loan demand. New home sales in January tanked

Willer Chen, an analyst at Forsyth Barr Asia:

It’s a “good gesture from the commercial banks but now the property problem is not about the mortgage rate”

The move may “slightly boost the property demand but would not expect much”

In kneejerk reaction, China rates are largely unchanged so far; 5y yield is down 0.5bp on the LPR cut. USDCNH is a touch lower as optimism builds. Funding remains tight with local paying interest; tom/next is around +1. The curve should continue to flatten given elevated funding which would support the front-end points while the back end should head lower.

The Shanghai Composite is fluctuating with an upward trend so far this morning, while China properties are trading higher after banks cut the key reference lending rate for mortgages by the most on record.

Tyler Durden

Mon, 02/19/2024 – 21:54