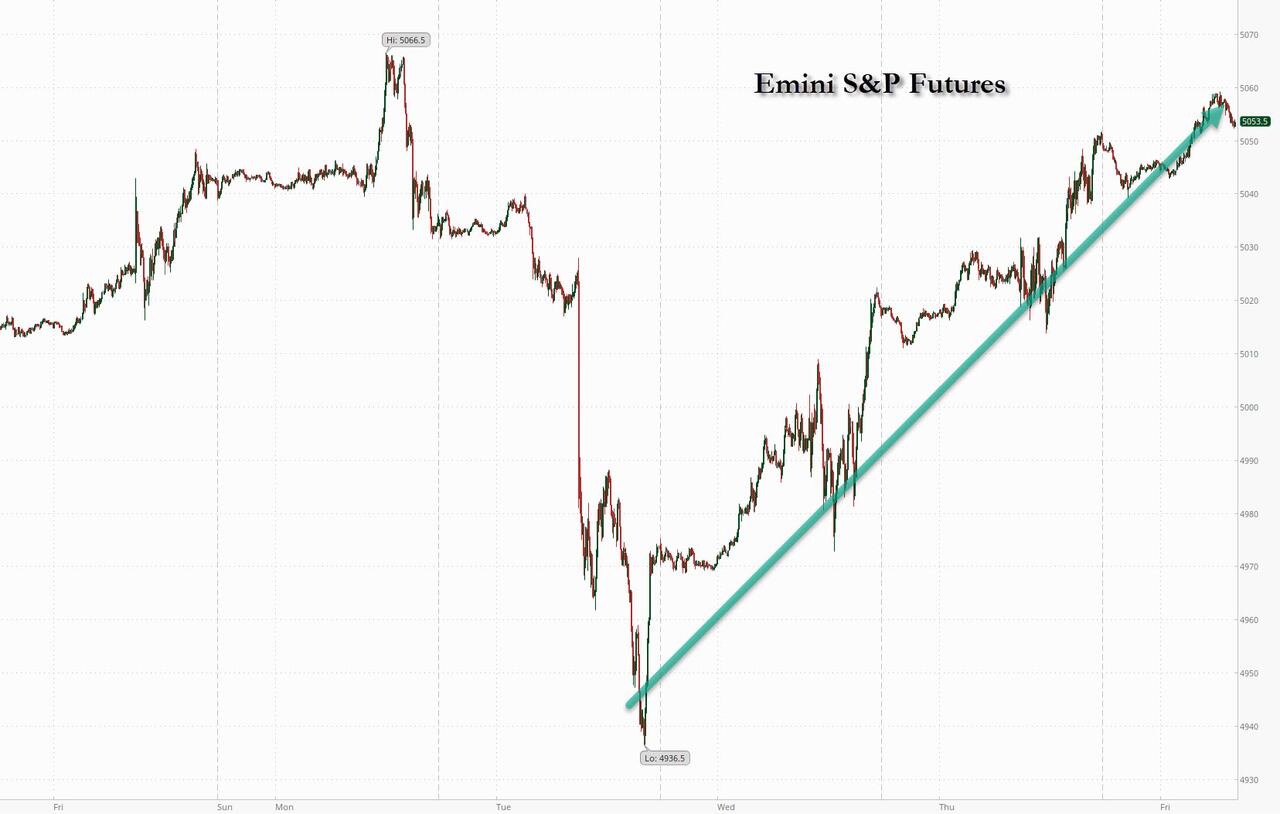

Stocks Set To Make It A Record 15 Weeks Higher Out Of 16 As Tech Surge Goes On

After stocks successfully recovered from a mid-week rout following the much hotter than expected CPI print, resulting in a burst of BTFD and flurry of 0DTE buying, on the last day of the week, S&P 500 futures were up 0.2% – amid bigger gains in European stocks …

{kind=link}

… and were on pace to dodge a weekly red candle in the process setting up a record 15th weekly gain of the past 16, as the market no longer drop. Ever. Meanwhile, the euphoria was even more ridiculous over in tech world where Nasdaq futures accelerated their silly meltup, rising 0.5%, propelled by Applied Materials rising ~13% in premarket trading while the current generation’s Gamestop, Supermicro, was up another 6% premarket, sending its RSI to a record 98.

{kind=link}

Treasuries declined, sending the 10Y yield up 3bps to 4.27% after Atlanta Fed President Raphael Bostic said there’s no rush to cut rates with the US labor market and economy still strong.

In premarket trading, Applied Materials, the largest US maker of chipmaking machinery, jumped 13% in premarket trading after giving a bullish revenue forecast that signalled some of the largest semiconductor companies are increasing their investments in new production. The update pushed up shares in European peers including Aixtron SE and ASML Holding NV. Here are some other notable premarket movers:

Bloom Energy falls 19% after the company’s 2024 revenue guidance missed the average analyst estimate.

Coinbase gains 15% after the cryptocurrency exchange reported revenue and earnings per share for the fourth quarter that beat.

DoorDash drops 7% after the company’s guidance for full-year marketplace gross order value trailed the average analyst estimate at the midpoint.

DraftKings slips 5% after company’s 4Q adjusted Ebitda missed estimates, with Morgan Stanley flagging headwinds from “unfavorable sports outcomes.”

Dropbox drops 13% after the file management software company reported fourth-quarter results that are seen as weak.

Roku falls 16% after first-quarter forecasts from the streaming-video platform company failed to impress.

SunPower tumbles 11% after the struggling rooftop solar installer announced $155 million in new financing from its majority investors — a development that will ease a cash crunch but also dilute the shares.

Toast rises 9% after the restaurant software company gave a full-year forecast for adjusted Ebitda that was stronger than expected.

Trade Desk gains 18% after the advertising technology company gave a first-quarter forecast that is much stronger than expected.

TreeHouse Foods falls 11% after the company issued net sales projections for year that trailed the average analyst estimates.

Yelp drops 9% after guiding for lower-than-expected adjusted Ebitda for 2024.

The S&P 500 climbed to its latest record high Thursday, erasing all this week’s losses, as a drop in US retail sales tempered investor worries about overheated consumer demand. Data on US producer prices later will draw higher-than-usual scrutiny after a hot consumer price index earlier this week roiled financial markets, with traders resetting their bets on Fed rate-cuts in 2024.

Meanwhile the latest bubble euphoria just won’t stop, as US equity funds registered inflows of $11 billion in the week through Feb. 14, the most in seven weeks,according to Bank of America. On the downside, breadth of the S&P 500 is currently the weakest since 2009 as the top five stocks in the index have fueled 75% of its gain so far this year, according to the Bank of America report.

“Q4 earnings have helped equities to cope with rates volatility,” said Emmanuel Cau, a strategist at Barclays Plc, in a note to clients. “Sticky US inflation keeps Goldilocks in check, but post the latest hawkish repricing, rates expectations have converged more toward the Fed forecasts.”

European stocks rise for a third day meanwhile, tracking a broadly positive session in Asia. Mining stocks led the advance in Europe that took Europe’s Stoxx 600 index to its fourth consecutive week of gains.Glencore Plc and Anglo American Plc both rose more than 3% amid optimism of a rebound in Chinese demand for metals. European commercial real estate stocks also gained after major US peer CBRE Group reported strong fourth-quarter earnings and suggested the worst was over for the downtrodden market for office leasing. Shares of CBRE, the world’s largest commercial real estate stock, jumped to the highest level in almost two years. Here are the most notable movers in Europe:

European chip-tool makers’ shares advance after their largest US peer, Applied Materials, gave a bullish revenue forecast for the current period, signaling that some of the biggest semiconductor companies are increasing their investments in new production.

European luxury stocks climb in early trading, boosted by a resurgence in Chinese travel over the Lunar New Year holiday.

Sika shares gain as much as 3.9% after the Swiss building materials group presented new guidance which reassured analysts amid weak macroeconomic trends.

NatWest shares turn higher in volatile trading Friday, rising after an initial drop following earnings. The bank downgraded its return on tangible equity target due to an expected peak in yields, but RBC says it may be trying to get bad news out of the way early.

Metso shares rise as much as 8.5%, hitting highest in almost five months, after the Finnish machinery producer said activity in Aggregates is expected to improve. Analysts see the results as positive overall, with scope for some small consensus upgrades.

Norwegian Air shares jump as much as 12%, to the highest price since May 2021, after giving a higher-than-expected forecast for 2024 Ebit. Pareto Securities notes that the airline’s 2024 pre-sale bookings are strong.

Dowlais Group shares rise as much as 5.7% after Barclays initiated coverage at overweight, saying the engineering specialist “ticks all the right boxes” when it comes to what investors are looking for in 2024.

Eni shares drop as much as 1.9% following fourth-quarter results that met expectations, with RBC saying some investors may find it disappointing that one-off income in its gas business made up for weakness elsewhere.

Nibe shares fall as much as 8.7%, the most since August, after the Swedish heat-pump maker’s 2024 outlook disappointed as weakening demand for its low-energy heating impact its order intake.

Umicore shares fall as much as 5.8% to their lowest intraday in eight years. The Belgian specialty chemicals firm reported second-half results Citi called “soft,” with metal prices and lower cathode volumes weighing on earnings.

Temenos shares fall as much as 9.5% in Zurich, hitting the lowest level since Thursday’s publication of a report by activist short-seller Hindenburg Research.

XP Power shares tumble as much as 41% after warning that the outlook for 2024 will fall “significantly” short of market expectations amid a slowdown in the semiconductor manufacturing equipment industry.

Earlier in the session, Asian stocks gained as Japanese equities steamed closer to their first record high in 34 years and Hong Kong stocks extended their rally to a third day.The MSCI Asia Pacific Index climbed as much as 1%, headed for its highest close since April 2022. Japan’s Toyota, Recruit Holdings and Mitsubishi UFJ Financial contributed most to the advance. The regional gauge is on course for a fourth-straight week of gains, its longest win streak in over a year. Key measures were higher in nearly every market except Taiwan.

Hang Seng climbed back above the 16,000 level with notable gains in biopharmaceuticals and property with the latter underpinned after a court dismissed liquidation petitions against Chinese developer Logan Group.

Nikkei 225 rallied and briefly approached within 100 points of its record high before reversing some of the gains.

ASX 200 was led higher by the mining sector but with the upside capped as large insurers faltered post-earnings.

Indian stocks capped off the week rising for a fourth straight day, led by a rally in automobile and healthcare stocks. The S&P BSE Sensex rose 0.5% to 72,426.64 in Mumbai, while the NSE Nifty 50 Index advanced 0.6% to 22,040.70. Most regional equity benchmarks advanced on the day, led by gains in Hong Kong and Japan.

In FX, the pound is down 0.1% having briefly gained after UK retail sales topped estimates. The yen is the weakest of the G-10 currencies, falling 0.2% versus the greenback.

In rates, treasuries were slightly cheaper across the curve, holding losses from Asia session after Fed Atlanta President Raphael Bostic said there’s no rush to cut rates with the US labor market and economy still strong. “My expectation is that the rate of inflation will continue to decline, but more slowly than the pace implied by where the markets signal monetary policy should be,”Bostic said in a speech Thursday in New York. He said policy decisions would be taken “without oppressive urgency.”

As a result, TSY yields are cheaper by 2bp-3bp across the curve with 5s30s spread flatter by around 1bp as belly and front-end underperform; 10-year yields around 4.26%, slightly outperforming bunds and gilts in the sector.According to Bloomberg, dollar issuance slate empty so far; Intel and British American Tobacco headlined a six-deal, $6.8b calendar Thursday, bringing this week’s volume to $37b. Early expectations for next week are in the $45b to $50b range, with some acquisition-related offerings possible

In commodities, oil prices decline, with WTI down 0.9% near $77.35 though near the highest close in three months as the risk-on mood in wider markets and signs OPEC+ members are complying with supply cuts overshadowed a gloomy demand outlook from the IEA. Spot gold is flat around $2,006/oz.

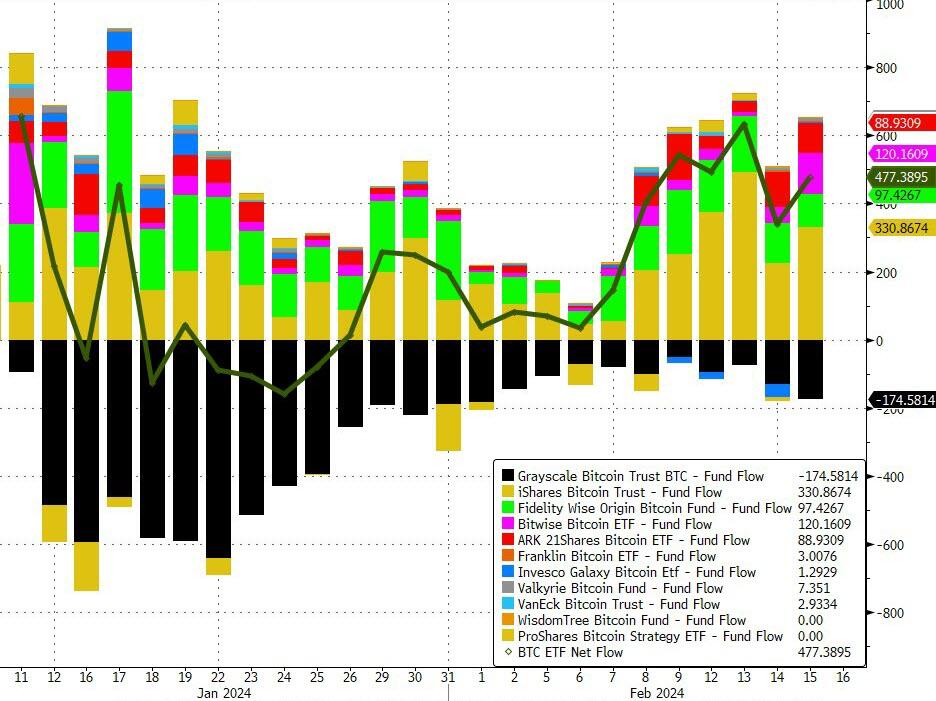

Bitcoin is firmer on the session, though still holds just shy of the USD 52k mark, as bitcoin ETF inflows just won’t stop.

{kind=link}

Turning to the day ahead, the US economic data calendar includes January PPI data, January housing starts/building permits, February New York Fed services business activity (8:30am) and February preliminary University of Michigan consumer sentiment (10am). Scheduled Fed speakers include Barkin (8am), Barr (9:10am) and Daly (12:10pm). Elsewhere we have the UK January retail sales and the Canadian International securities transactions.

Market Snapshot

S&P 500 futures up 0.2% to 5,056.25

STOXX Europe 600 up 0.6% to 491.35

MXAP up 1.0% to 170.90

MXAPJ up 1.0% to 522.12

Nikkei up 0.9% to 38,487.24

Topix up 1.3% to 2,624.73

Hang Seng Index up 2.5% to 16,339.96

Shanghai Composite up 1.3% to 2,865.90

Sensex up 0.6% to 72,466.63

Australia S&P/ASX 200 up 0.7% to 7,658.32

Kospi up 1.3% to 2,648.76

German 10Y yield little changed at 2.38%

Euro little changed at $1.0771

Brent Futures down 0.8% to $82.21/bbl

Brent Futures down 0.8% to $82.23/bbl

Gold spot up 0.1% to $2,006.25

U.S. Dollar Index little changed at 104.32

Top Overnight News

The BOJ is on track to end negative interest rates in coming months despite the economy’s fall into recession, say sources familiar with its thinking, though weak domestic demand means they may seek more clues on wages growth before acting. RTRS

China’s gov’t could dramatically expand its real estate footprint, buying up distressed projects and/or building more subsidized housing as Xi looks to put more of the industry under state control. WSJ

A resurgence in travel over China’s Lunar New Year holiday is offering some signs of a consumer spending pickup in the world’s second-largest economy as it struggles with low confidence and deflation. More than 61 million rail trips were made in the first six days of the national new year holiday, according to official reports. That was the highest in data compiled by Bloomberg News in the last five years, and it marked a 61% increase over the same vacation period in 2023. BBG

The ECB should avoid waiting too long to cut rates as it will still have flexibility over the pace and degree of policy loosening after its first move, Governing Council member Francois Villeroy de Galhau said. BBG

Federal Reserve Bank of Atlanta President Raphael Bostic said there’s no rush to cut interest rates with the US labor market and economy still strong, and cautioned it’s not yet clear that inflation is heading sustainably to the central bank’s 2% target. BBG

The space-based weapon U.S. intelligence believes Russia may be developing is more likely a nuclear-powered device to blind, jam or fry the electronics inside satellites than an explosive nuclear warhead to shoot them down, analysts said on Thursday. The intelligence came to light on Wednesday after Representative Mike Turner, Republican chair of the U.S. House of Representatives intelligence committee, issued an unusual statement warning of a “serious national security threat.” RTRS

Egyptian authorities, fearful that an Israeli military push further into southern Gaza will set off a flood of refugees, are building an 8-square-mile walled enclosure in the Sinai Desert near the border, according to Egyptian officials and security analysts. WSJ

The US House will not pass another temporary spending bill to avert a partial government shutdown when the latest deadline expires on March 1, the chamber’s No. 3 leader said Thursday. BBG

FBI informant at the center of the House GOP bribery allegations against Biden gets indicted over making false statements (the indictment claims the false statements were made due to the individual’s opposition to Biden’s candidacy). The Hill

Earnings

Applied Materials (AMAT) – Q1 2024 (USD): Adj. EPS 2.13 (exp. 1.91), Revenue 6.71bln (exp. 6.48bln). Sees Q2 Adj. EPS USD 1.79-2.15 (exp. 1.80). Sees Q2 rev. USD 6.5bln (exp. 5.92bln). CEO says there is a reacceleration in capital investment by cloud companies; memory investment levels are normalising; fab utilisation is increasing across all device types. The DRAM market is strengthening. Sees leading-edge foundry logic being stronger Y/Y in 2024 even though some important projects are delayed. Expect NAND revenues to be up Y/Y but NAND to remain less than 10% of total wafer fab equipment spending. CFO says expect the equipment market to grow as fast or faster than semiconductors over time. (Newswires) Shares +12.7% in pre-market trade

Coinbase Global Inc (COIN) – Q4 2023 (USD): EPS 1.04 (exp. -0.01), Revenue 953.8mln (exp. 826.3mln). Q1 subscription and services revenue view USD 410-480mln (exp. 367.3mln). (Newswires) Shares +10.7% in pre-market trade

DoorDash Inc (DASH) – Q4 2023 (USD): EPS -0.39 (exp. -0.16), Revenue 2.3bln (exp. 2.24bln). FY gross order value view 74-78bln (exp. 76.54bln). FY adj. EBITDA 1.5-1.9bln (exp. 1.62bln). Q1 EBITDA view 320-380mln (exp. 360.3mln). Q1 Marketplace gross order value 18.5-18.9bln (exp. 18.57bln). (DoorDash IR) Shares -7.5% in pre-market trade

DraftKings Inc (DKNG) – Q4 2023 (USD): EPS -0.10 (exp. 0.08), Net income -44.6mln (exp. profit 39.7mln), Revenue 1.23bln (exp. 1.24bln). Monthly Unique Payers 3.5mln (exp. 3.44mln). Average revenue per monthly unique payer 116 (exp. 119.79). FY24 revenue view 4.65-4.9bln (prev. 4.5-4.8bln). FY24 adj. EBITDA view 410-510mln (prev. 350-450mln). DraftKings to acquire Jackpocket for USD 750mln. (DraftKings IR) Shares -3.5% in pre-market trade

Eni (ENI IM) – Q4 (EUR): adj. PBT 3.16bln (exp. 3.39bln), adj. Net 1.6bln (exp. 1.71bln), adj. EBIT 3.76bln (prev. 4.98bln). FY24 outlook will be provided at the 14th March capital markets day. Shares -1.7% in European trade

A more detailed look at global markets courtesy of Newsquawk

APAC stocks sustained the positive momentum from Wall St where yields softened after the US data deluge.ASX 200 was led higher by the mining sector but with the upside capped as large insurers faltered post-earnings. Nikkei 225 rallied and briefly approached within 100 points of its record high before reversing some of the gains. Hang Seng climbed back above the 16,000 level with notable gains in biopharmaceuticals and property with the latter underpinned after a court dismissed liquidation petitions against Chinese developer Logan Group.

Top Asian News

BoJ Governor Ueda said when a sustained and stable achievement of the price target comes into sight, they will examine whether to maintain various easing measures including the negative interest rate. Ueda also noted the specific means of rolling back stimulus will depend on economic conditions at the time and based on the current economic and price outlook, monetary conditions will likely remain accommodative even after ending negative rates.

Japanese Finance Minister Suzuki said a weak yen has merits and demerits, while he is concerned about the negative aspects of a weak yen and reiterated that rapid FX moves are undesirable and is closely watching FX moves with a sense of urgency.

RBNZ Governor Orr refrained from talking about the rate outlook and said they have more work to do to get inflation expectations anchored to 2%. Governor Orr said a flexible approach to inflation targeting with a medium-term focus remains appropriate and bringing levels of core inflation back in line with the bank’s 1-3% target is an important part of bringing inflation back to the 2% midpoint, while he also noted the removal of the maximum sustainable employment objective does not mean any big changes to RBNZ’s monetary policy strategy.

European bourses, Stoxx600 (+0.6%) began the session entirely in the green and continued to grind higher throughout the morning.The AEX (+1.0%) is the European outperformer, lifted by strength in semi-conductor names after US-listed Applied Materials (+13.2%) reported strong earnings after-hours; BE Semiconductor (+3.2%), ASM (+3.2%), ASML (+1.3%). European sectors hold a positive tilt, with Basic Resources leading, boosted by higher underlying base metal prices. Tech benefits in a read-across from Applied Materials results. Telecoms lags, hampered by losses in Vodafone (-1.0%). US Equity Futures (ES +0.2%, NQ +0.5%, RTY +0.1%) are mixed, with clear outperformance in the NQ, with optimism permeating within the index after Applied Materials (+13.2%) reported strong results.

Top European News

UK opposition Labour Party won the by-elections in Wellingborough and Kingswood which were both previously held by the Tories, according to The Times.

ECB’s Villeroy said the principle of a rate cut this year seems to be a given and there is still a question of a precise calendar for a rate cut, while he added there are several reasons as to why the ECB should not wait for too long before making the first rate cut, according to an interview with L’Echo cited by Reuters.

ECB’s Schnabel says monetary policy needs to remain restrictive until can be confident that inflation will sustainably return to our medium-term target. Must be cautious not to adjust the policy stance prematurely. Productivity growth is a key determinant of medium-term inflation and real interest rates, which means it directly affects the conduct of monetary policy. Persistently low, and recently even negative, productivity growth exacerbates the effects that the current strong growth in nominal wages has on unit labour costs for firms. This increases the risk that firms may pass higher wage costs on to consumers, which could delay inflation returning to our 2% target. New estimates show that an increase in trend productivity growth by one percentage point can increase r-star by 0.6 percentage points; a higher r-star would reduce the need to embark on unconventional policy measures that often come with larger side effects.

Russian Federation Central Bank Key Rate (Feb) 16.0% vs. Exp. 16.0% (Prev. 16.0%); sees its average key rate at 13.5-15.5% in 2024 (prev. forecast 12.5-14.5%;

FX

Contained trade for DXY and within a tight 104.26-44 range, respecting yesterday’s 104.18-71 range. Upside sees the WTD peak at 104.97, as the index awaits impetus from US PPI.

EUR/USD is contained within yesterday’s 1.0724-84 range as ECB speak does little to sway price action. Any USD selling could prompt a test of 1.08 but Monday’s move above the level was unconvincing.

Following UK Retail Sales Cable initially spiked higher to 1.2605 before gains were trimmed as some desks questioned seasonality issues with the data and with the BoE focussed on wages/inflation. Downside targets include 200DMA at 1.2654.

JPY is the laggard across the majors with some noting BoJ Governor Ueda remaining dovish overnight. So far USD/JPY has printed a peak of 150.36 and is yet to threaten yesterday’s top of 150.58.

Fixed Income

Gilts gapped lower by just under 30 ticks to 97.67 at the open and then waned further to 97.56, following strong Jan. Retail Sales which speak to the signs of an upturn flagged by Bailey pre-GDP.

Bunds have been driven lower by UK Retail Sales with newsflow limited; as such Bunds have not meaningfully moved from their 133.08 session trough.

USTs are moving in tandem with EGBs/Gilts as we head towards the sessions next listed events of Fed’s Barkin and Barr who are scheduled either side of PPI; currently holding around the 109-28 trough.

Commodities

Crude prices have started ebbing lower, paring back some of the prior day’s advances, but the European morning has been quiet thus far in the run-up to the US PPI data and more Fed speak; Brent testing USD 82.00/bbl to the downside.

Muted action across precious metals but prices remain underpinned by yesterday’s Dollar pullback and overall geopolitics; spot gold is flat around yesterday’s highs (USD 2,008.34/oz).

Base metals are mostly firmer with copper among the outperformers despite an obvious catalyst but with desks citing rate cut hopes following yesterday’s US Retail Sales data.

Japan’s Cosmo Oil restarted No.1 CDU in 220k BPD Chiba refinery on Feb 14th following system issues.

Japan’s Eneos (5020 JT) shut its 153k BPD Negishi CDU on Feb 10th amid equipment failure.

Japan is said to be mulling an extension of gasoline subsidies beyond April and gradually phasing it out by summer, according to Kyodo

Azerbaijan Jan oil production 474k BPD (prev. 482k in Dec)

Geopolitics: Middle East

US President Biden raised the situation in Rafah during a call with Israeli PM Netanyahu and reiterated his view that a military operation should not proceed without a credible and executable plan for ensuring the safety of and support for civilians in Rafah. Biden also reaffirmed his commitment to working tirelessly to support the release of all hostages as soon as possible, according to Reuters.

US State Department said the US is working with Qatar, Israel and Egypt on the hostage talks to find an agreement and there are some very hard issues to be resolved, while it was also reported that US Secretary of State Blinken said he believes an Israel-Hamas hostage deal is possible.

US VP Harris is to meet Israeli President Herzog and will meet Iraq’s PM Al-Sudani at the Munich Security Conference today, while Secretary of State Blinken is also to meet with Chinese Foreign Minister Wang at the Munich Security Conference.

“Israeli newspaper Haaretz: Officials expect to conclude a deal to exchange detainees with Hamas within Ramadan month [March]”, according to Sky News Arabia.

“Yemen said its armed forces fired missiles at a British ship passing though the Gulf of Aden on Thursday and scored a “direct hit” in their latest operation in solidarity with the Palestinians.”, according to Tehran Times.

Geopolitics: Other

Japanese Chief Cabinet Secretary Hayashi said they are aware of comments made by North Korean leader Kim’s sister but added that they cannot accept North Korea’s claim that abduction issues were solved, while there is no change to our position to resolve various issues with North Korea comprehensively.

Belarusian President Lukashenko says several Ukrainian citizens were detained on border with Belarus for transporting explosives for use in Russia and Belarus

US Event Calendar

08:30: Jan. PPI Final Demand MoM, est. 0.1%, prior -0.1%, revised -0.2%

Jan. PPI Final Demand YoY, est. 0.6%, prior 1.0%

Jan. PPI Ex Food and Energy MoM, est. 0.1%, prior 0%, revised -0.1%

Jan. PPI Ex Food and Energy YoY, est. 1.6%, prior 1.8%

08:30: Jan. Housing Starts, est. 1.46m, prior 1.46m

Jan. Housing Starts MoM, est. 0%, prior -4.3%

Jan. Building Permits, est. 1.51m, prior 1.5m, revised 1.49m

Jan. Building Permits MoM, est. 1.3%, prior 1.9%, revised 1.8%

08:30: Feb. New York Fed Services Business, prior -9.7

10:00: Feb. U. of Mich. Sentiment, est. 80.0, prior 79.0

Feb. U. of Mich. Current Conditions, est. 82.5, prior 81.9

Feb. U. of Mich. Expectations, est. 77.0, prior 77.1

Feb. U. of Mich. 1 Yr Inflation, est. 2.9%, prior 2.9%

Feb. U. of Mich. 5-10 Yr Inflation, est. 2.8%, prior 2.9%

Central Bank Speakers

08:00: Fed’s Barkin Speaks in Richmond

09:10: Fed’s Barr Speaks on Bank Supervision

12:10: Fed’s Daly Speaks at NABE Conference

DB’s Jim Reid concludes the overnight wrap

Yesterday was a busy one in terms of data, with a complicated message coming out of the releases ahead of what’s become the most important US PPI print for a while today. PPI will provide an update on some key services components of PCE inflation, including healthcare, airfares, and portfolio management. The first two of these areas saw strong increases in the CPI print earlier this week, but this often does not match the details of the PPI all that closely.

In contrast to that hot CPI print earlier this week, yesterday’s retail sales print threw a conflicting message to that we’ve become accustomed to in recent weeks. The markets largely took what was mixed data in their stride though, with the S&P 500 (+0.58%) managing to post a new all-time high, while 10yr Treasuries (-2.5bps) were well off the yield lows for the day by the close.

Onto that data, and the headline US retail sales missed to the downside, falling -0.8% month-on-month (vs -0.2% expected), and with the December reading revised down from 0.6% to 0.4%. This is the weakest report since last March and showed a broad-based cooling with nine of the 13 spending categories declining. Seasonal factors can sometimes lead to a steep fall in January after the end of the holiday season, but the details of this print and the December revision were not suggestive of this. The retail control group, which excludes vehicles, gas, food services and building materials, and has the strongest correlation with the GDP number, also fell -0.4% (vs 0.2% expected), the first decline since last March. Moreover, retail control growth was revised lower for both December (from +0.8% to +0.6%) and November (from +0.5% to +0.2%). Interestingly, non-store retailers like Amazon accounted for most of the decline in retail control. The category had been a supportive force for retail spending in previous prints.

Adding to the data weakness, industrial production for January also came in softer than expected, falling -0.1% month-on-month (vs 0.2% expected). These reports point to a potential loss of US growth momentum at the start of the year and from a weaker starting point, with the Atlanta Fed GDP nowcast for Q1 down from 3.4% to 2.9% as a result. That said, this is still very decent and other data yesterday was less downbeat. Weekly jobless claims came in modestly below expectations at 212k (vs 220k expected) even if continuing claims rose more than expected to 1895k vs (1880k expected). To continue with the flip flopping nature of the data, we also saw the US February Philadelphia Fed factory index post an upside surprise of 5.2 (vs -8.1 expected), up from -10.6. This is the first-time we’ve seen a positive reading since last August, pointing to improved industrial conditions for the district.

The opening equity reaction to the data was largely neutral but positive sentiment then dominated through the course of the day, with the S&P 500 (+0.58%) closing at another all-time high. This was a broad rally with banks (+2.91%) and energy stocks (+2.48%) the best performers within the S&P 500. Bank outperformance saw the KBW regional bank index rise by +3.64%, its strongest gain in two months. Small caps also posted strong gains, as the Russell 2000 (+2.45%) reached a YTD high 2 days after seeing its worst fall since June 2022. On the other hand, tech stocks underperformed, with the NASDAQ (+0.30%) and the Magnificent 7 (+0.20%) posting only modest gains.

There were some contrasting moves within the Magnificent 7. Tesla rallied +6.22% as a filing showed Elon Musk increasing his stake in the company. At the other end, Alphabet lost -2.17% on news that OpenAI was developing a web search product that could compete with Google. Nvidia also retreated -1.68% from its all-time high. For more on Nvidia, and the 2024 outlook on semiconductors, see our chartbook earlier this week here. There were some more encouraging news for chipmakers late on as Applied Materials, the largest US market of chipmaking machinery, posted upbeat sales guidance.

On the rates side, we initially saw a sizeable rally on the back of the US releases, as December 2024 Fed funds futures fell by 8bps, but this move reversed by the end of the trading session, with the amount of cuts expected by the December meeting unchanged on the day. Fed fund futures have given up another 10bps of 2024 cuts overnight, after Atlanta Fed Governor Bostic said he was “not yet comfortable that inflation is inexorably declining to our 2% objective”, suggesting it may take “some time” for this rate-cut condition to be met. As we go to print ECB Villeroy (slight dove) has just been quoted as saying that the “risk of cutting too late at least as big as too early”.

10yr Treasury yields fell by c. 3pbs immediately after the data, trading almost 7bps lower on the day, but retraced much of the decline to finish the day down -2.5bps at 4.23%, while 2yr yields were down -0.4bps, having traded -8bps down early on. This backdrop saw the broad dollar index decline for the second day in a row (-0.41%) after its three-month high on Tuesday. Overnight, yields have edged back higher with 10yr and 2yr yields both c.+2.5bps to trade at 4.255% and 4.60% respectively.

Over In Europe, fixed income sold off yesterday, as 10yr bunds rose +2.3bps, while OATs (+1.5bps) and BTPs (+0.5bps) saw more modest weakness despite dovish remarks from Malta central bank governor Scicluna, who stated he was “open to rate cut in March as inflation fades”. He is the first to throw in explicit backing for an imminent cut, but also lies clearly on the dovish end of the Governing Council.

Over in the UK, data showed that the economy slipped into a technical recession in the second half of last year, as GDP fell by a larger-than-expected -0.3% quarter-on-quarter in Q4 (vs -0.1% expected and -0.1% prev.), driven by weak consumption and net trade. This saw the expected 2024 BoE rate pricing fall intraday, but this reversed shortly after with 75bps of 2024 cuts priced by the close. The FTSE 100 rose +0.38%. Gilts were largely flat on the day, with the 10yr yield up +1.0bps.

Asian equity markets are extending overnight gains on Wall Street with Hang Seng (+2.44%) leading the way and with the Nikkei (+0.97%) hitting a fresh 34-year high and within touching distance of its all-time high level of 38,916 which was set as long ago as December 1989. Elsewhere, the KOSPI (+1.20%) and the S&P/ASX 200 (+0.68%) are also higher with markets in China remaining closed for the Lunar New Year holidays. US stock futures are fairly flat.

Early morning data showed that the unemployment rate in South Korea dropped more than expected to 3.0% in January compared to a downwardly revised +3.2% level in December. The stronger than expected data indicates that the nation’s labour market remains tight.

Briefly on commodities, oil gained yesterday even as the International Energy Agency trimmed its 2024 demand growth projection relative to January’s forecast. Brent crude rose +1.54% to $82.86/bbl, and WTI crude by +1.81% to $78.03/bbl.

Now to the day ahead. In terms of US data, we have January PPI, housing starts, building permits, the February University of Michigan survey, New York fed services business activity. Elsewhere we have the UK January retail sales and the Canadian International securities transactions. We will also hear from the Fed’s Daly and Bostic, and the ECB’s Schnabel.

Tyler Durden

Fri, 02/16/2024 – 08:13