Reverse Repo Liquidity Plunges Below Key Level As Fed’s QT Stalls

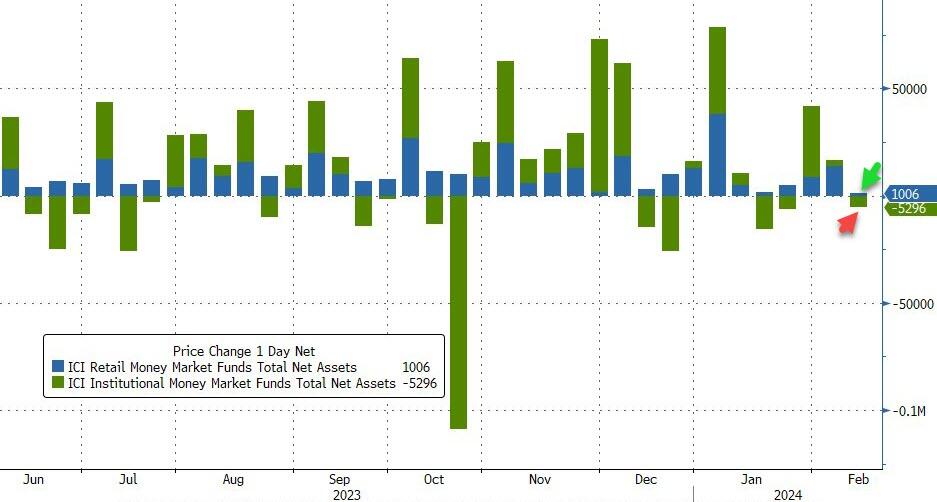

After two big weekly inflows, money market funds saw very modest outflows last week (-$4.3BN), but still hold above $6 trillion, just barely off the record highs…

{kind=link}

Source: Bloomberg

In a breakdown for the week to Feb. 14, government funds – which invest primarily in securities like Treasury bills, repurchase agreements and agency debt – saw assets fall to $4.882 trillion, a $11 billion decline.

Prime funds, which tend to invest in higher-risk assets such as commercial paper, meanwhile, saw assets rise to $1.013 trillion, a $6.55 billion increase.

The outflows were all institutional (-$5.3BN) while Retail funds saw a $1BN inflow…

{kind=link}

Source: Bloomberg

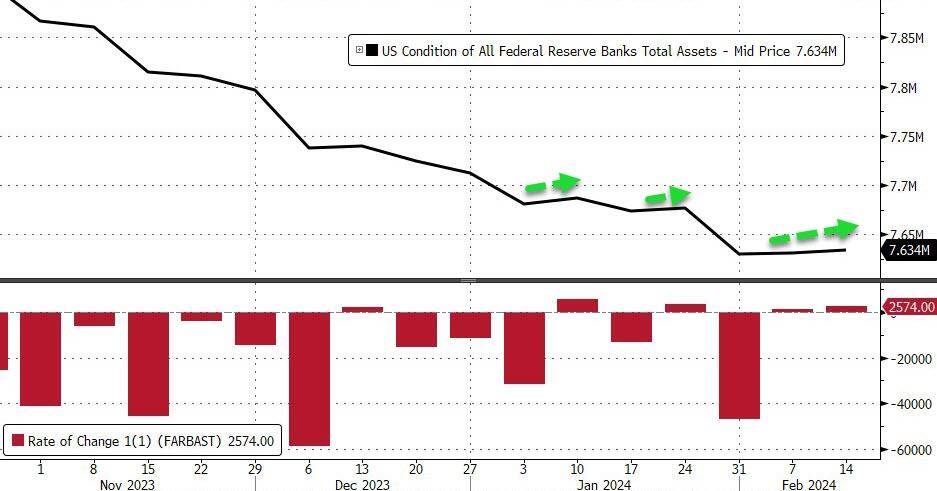

The Fed’s balance sheet expanded for the second straight week (+$2.6BN) and has risen in 4 of the last 6 weeks…

{kind=link}

Source: Bloomberg

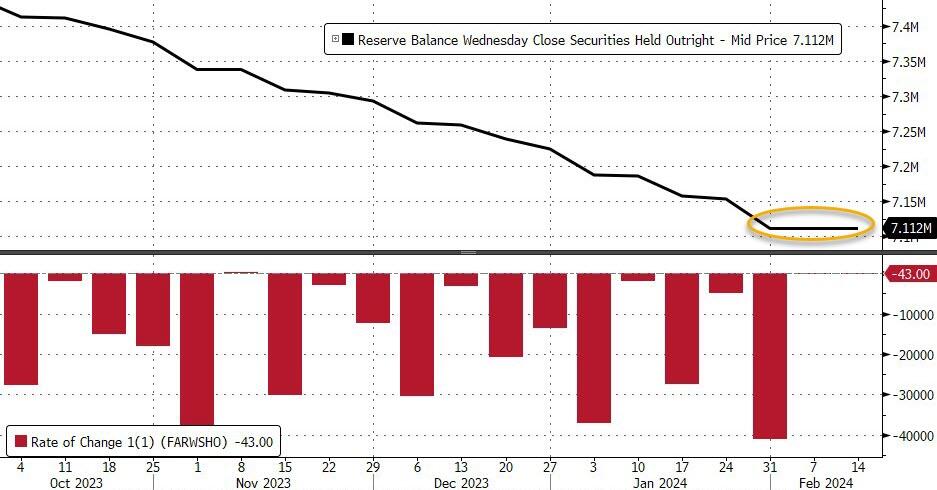

After a big drop at the end of January, The Fed’s QT has stalled in February (that is a a tiny $155 million decline in two weeks)…

{kind=link}

Source: Bloomberg

This is the smallest two-week decline in The Fed’s Securities book…

{kind=link}

Source: Bloomberg

Of course, The Fed would not stop QT without a statement and this ‘stall’ in its selling down its book is likely more of a technical event related to settlements and timing.

Nevertheless, it is worth paying close attention to, given the facts below.

Bank reserves at The Fed declined modestly last week as US equity market capitalization remains significantly decoupled…

{kind=link}

Source: Bloomberg

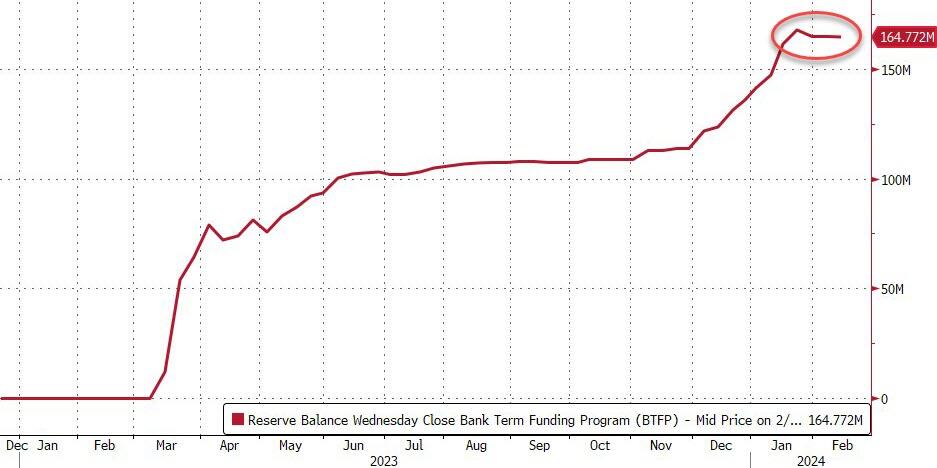

Banks usage of The Fed’s bailout facility is flat near record highs around $165BN since it cut them off from their free-money arb…

{kind=link}

Source: Bloomberg

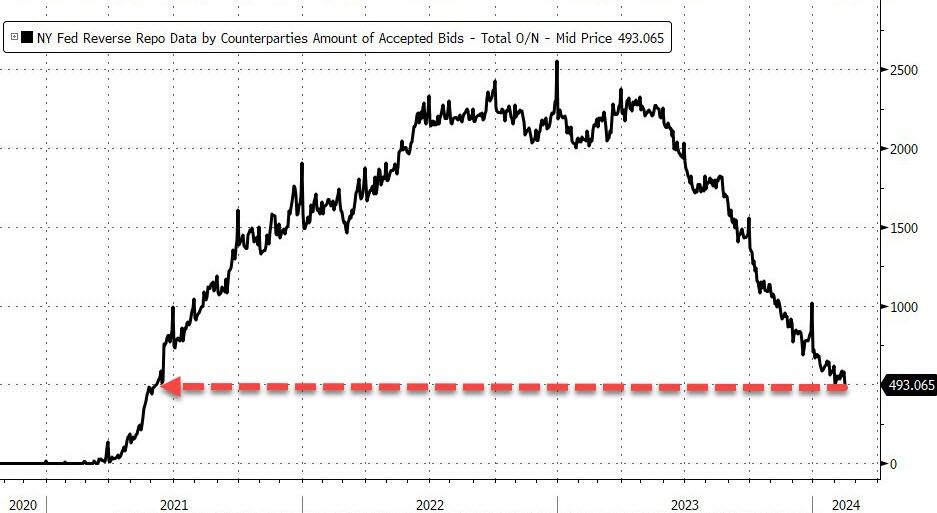

And finally, the much-needed source of liquidity at The Fed’s Reverse Repo facility plunged ($82BN) back below $500BN (to $493BN) for the first time since June 2021…

{kind=link}

Source: Bloomberg

This was the biggest non-month-end drop since October and quite a shock as RRP usage had been relatively stable recently. As Curvature’s Scott E.D. Skyrm noted:

“It’s an even greater surprise given the soft funding. RRP volume tends to drop less when GC rates are low because the 5.30% RRP rate is more competitive with market rates.”

So, this smells like some more desperate funding needs.

As a reminder, The Treasury Borrowing Advisory Committee – a panel of investors, dealers and other market participants that regularly counsels the department – noted that while most expect RRP balances to run down to zero, there are some looking for a “sustained low level” of usage, in the $200 billion to $300 billion range.

The importance of RRP levels was noted by Dallas Fed President Lorie Logan, who said in January the central bank should slow its balance sheet runoff – a process known as quantitative tightening, or QT – as reverse repo balances approach a low level.

All of which means we are right on cue for March madness… as BTFP matures and banks are forced to fund their $160BN hole through the discount window.

Tyler Durden

Thu, 02/15/2024 – 16:40