It’s Feeling Like “Last Days Of Rome”: Market Heading For Giant Gamma-Squeeze Blow-Off Top

By Simon White, Bloomberg markets live reporter and strategist

Options-driven fever of investors fearful of missing out in a market at all-time highs is helping push stocks higher, and has the potential to culminate in a blow-off top.

FOMO is once again in evidence as both the S&P and the Nasdaq make new highs. If you fear you’re already missing out, what better strategy than to use the gearing of options to make up for lost ground?This could drive a potent self-fulfilling rally that contains the seeds of its own demise (ZH: see “”Everyone Is In The Same Trades And All-In”: Goldman Tells Clients To Get Out Of “Parabolic” Tech Stocks“).

Options are the financial crystallization of greed and fear. Buy call options when greedy; buy put options when fearful. And if you’re only somewhat greedy and not too fearful, you can sell calls or puts. Today, greed is in the ascendant and fear is in abeyance. That’s a recipe for a blow-off top.

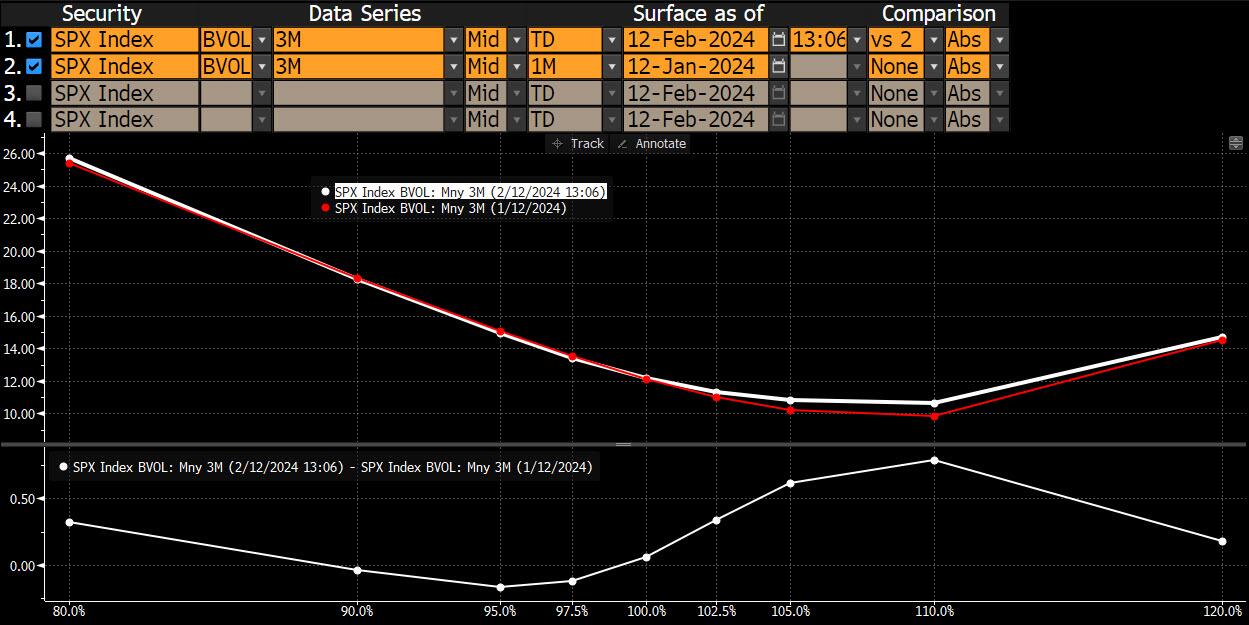

How can this happen?Over the past month, S&P call prices have risen more than put prices. The red line in the chart below is of S&P option prices by strike a month ago, while the white line is their price today.

The white line has risen more than the red line on the right-hand side of the chart, that is at higher strikes, versus at lower strikes. This shows it is likely investors are buying more calls than puts, i.e. they are increasingly taking leveraged long positions on the market with unlimited upside. Falling put/call ratios, both in price and volume terms, corroborate this. The effect is even more pronounced in tech and the Magnificent 7.

{kind=link}

This sort of action has the potential to lead to a rapid rise in stock prices that finally exhausts itself, culminating in an abrupt selloff. The reason is falling and ultimately negative gamma.

When gamma is positive, as it is more often is, the hedging behavior of option dealers – who take the opposite side of investors – represses volatility, as they must sell after the market rallies and buy after it sells off to rebalance their positions.

{kind=link}

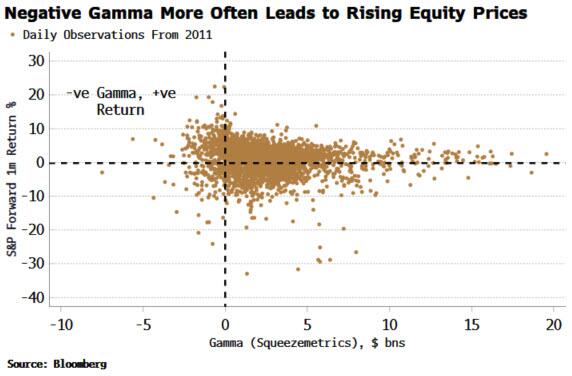

But when gamma is negative, dealers must chase prices, and volatility can quickly rise.Negative gamma is commonly associated with falling markets. Investors tend to own deeper out-of-the-money puts for protection. As the market begins to fall, these puts become more in the money and dealers must increasingly sell more of the underlying index to hedge.

Yet more often, negative gamma leads to a rising stock market. That’s even more likely when the fear gauge is low. Why bother hedging downside if you think stocks can only go up? Demand for protection, i.e. buying puts, falls, and thus there is an absence of this source of self-fulfilling dealer selling.

{kind=link}

Instead, the opposite dynamic becomes more likely. Investors are long out-of-the-money calls, which is a potential deep source of buying by dealers, pushing gamma more negative, forcing yet more buying as the market rises.

That continues until something breaks, more often than not a rise in implied vols when the calls become in-the-money, which triggers a cascade of selling by dealers (this is due to one of the lesser-known Greeks, vanna, the derivative of the option’s delta with respect to volatility). Voila! – a blow-off top.

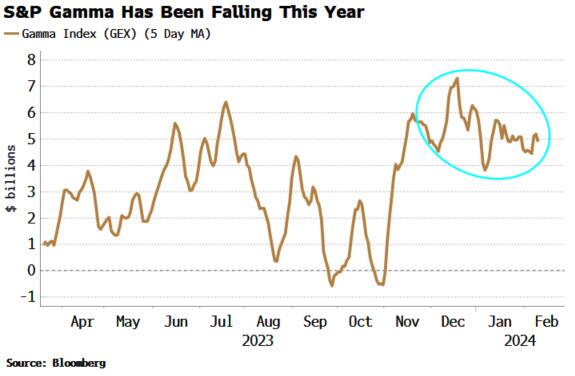

The current dynamic could have more room to run before we get there. Gamma is still positive, but it has been grinding lower [and as ZeroHedge pointed out, expect a collapse in gamma this week as “Massive “Unclenching” Looms As 90% Of Dealar Gamma To Expire By Friday“].

The call buying by investors adding negative gamma is being tempered by investors taking leveraged long positions by selling out-of-the-money puts. The first represents greed, the second a lack of fear. Both expect the market to keep rallying.

Selling puts generates some selling as dealers hedge, but as the market moves higher, investors are more likely to take profit on their positions, which necessitates the dealer buying back their hedge, pushing the market higher.

The current investor preference for selling puts and buying calls, rather than the more usual buying of puts and selling of calls, is thus the perfect recipe for a blow-off top – especially if outright greed starts to dominate and investors prefer uncapped upside to stocks, i.e. long call exposure.

As mentioned above, the tech sector and largest stocks are seeing a more magnified version of what is happening in the broad index, with investors driving up call prices relative to put prices. I thought it would be interesting to see what sectors are leading the advance when we go into a blow-off top.

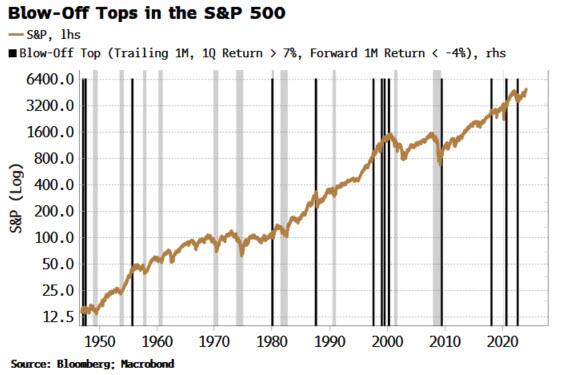

There is no standard definition for such a top other than there’s sharp rally into it and a rapid selloff after it. I defined one as being when the trailing monthly and quarterly returns for the S&P are more than 7%, and the forward monthly return is less than -4%. That gives us a not-too-numerous list of blow-off tops that contains many of the times you would expect, such as the run-up to the end of the tech bubble in 1999/2000(white bars are the tops, gray bars are recessions).

{kind=link}

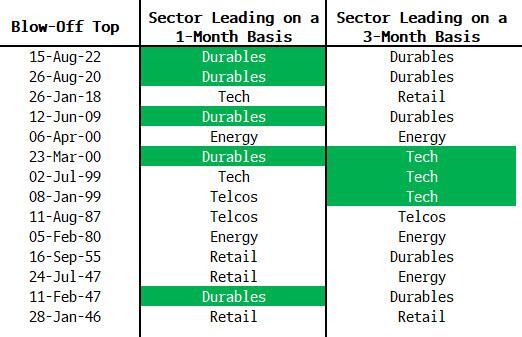

Looking at what sectors were leading on a one and three-month basis at these times (using the Fama-French definitions to get data back to 1940s) gives the table below. Interestingly, tech does not make up the majority of times as I would have expected. On a one and three-month basis, consumer durables was most commonly leading the market, followed by tech and energy, while on a three-month basis, tech is in equal second place with energy.

{kind=link}

The tech and communication services sectors have been taking turns in leading the current market (on a three-month basis), but there is little, historically speaking, to prevent another sector taking the lead in any final, capitulatory move higher.

The Nasdaq and S&P today almost meet the ex ante criteria for a blow-off top, with their trailing quarterly returns more than 7%, but their one-month returns still under 7% at ~5-6%. And various measures of equity-index breadth are not yet near extremes, suggesting the rally could keep going for now.

It is starting to feel a little “last days of Rome” as markets drive relentlessly higher, seemingly unimpeded. The underlying set-up shows that – until the barbarians break through the gates and stocks run out of luck – the grape-eating excess could reach new heights of decadence.

Tyler Durden

Tue, 02/13/2024 – 12:40