Water Level Projections Threaten Future Panama Canal Transits

By Tony Mulvey of FreightWaves

Dry season in Panama is in full swing, and the impacts to trade through the Panama Canal will remain challenged in the months to come. The situation in the canal, after a wetter-than-expected November, wasn’t as dire as many believed, allowing the number of daily transits to increase in January.

{kind=link}

The Panama Canal forecast 24 daily transits in January, up from 20 previously expected for January and 18 previously expected for February. Throughout fiscal year 2023, 12,638 vessels traversed the canal, a daily average of 34 oceangoing vessels moving through the canal.

In the first four months of the canal’s fiscal year 2024, there were 3,233 transits across all vessel types, with the vast majority being Panamax vessels. The run rate for fiscal year 2024 of vessels through the canal is 9,700, 23% lower than the 2023 fiscal year throughput.

While container traffic receives a lot of attention, the tanker and dry bulk market will be heavily impacted as well. Through the first four months of fiscal 2024, chemical tankers have made up 25.6% of Panamax-class vessels that have traversed the canal. Liquefied petroleum gas carriers made up 25.5% of the Neopanamax traffic through the canal.

The water levels within the Panama Canal are largely to blame, but any hope for a significant rebound in water levels to boost throughput will likely be met with a harsh reality over the next few months.

{kind=link}

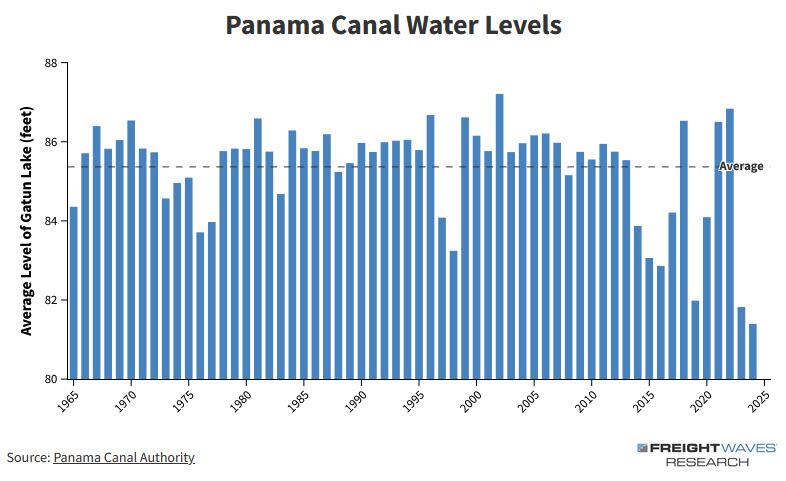

The water levels are going to remain a challenge that has the potential to continue to derail vessel throughput. Gatun Lake, the manmade lake that vessels must traverse, had water levels at 81.2 feet as of Tuesday. Water levels in this critical portion of the canal have started 2024 at the lowest level on record, dating back to 1965.

Projections are for even lower levels over the next two months, falling below 80 feet in early April.

Three of the largest five ports in the U.S. rely on shipments that navigate through the Panama Canal: the Port of New York and New Jersey, the Port of Savannah, Georgia, and Port Houston.Over the past month, these three ports combined to handle 30% of total twenty-foot equivalent unit throughput. For reference, the two largest ports in the country: the Port of Los Angeles and the Port of Long Beach, accounted for 32% of the total U.S. throughput.

Import demand has picked up steam ahead of the Lunar New Year, which will provide a boost to overall imports that are trending above last year’s levels. This boost is being felt by the East Coast ports, like Savannah, where the Ocean TEU Volume Index is up over 40% in the past month.

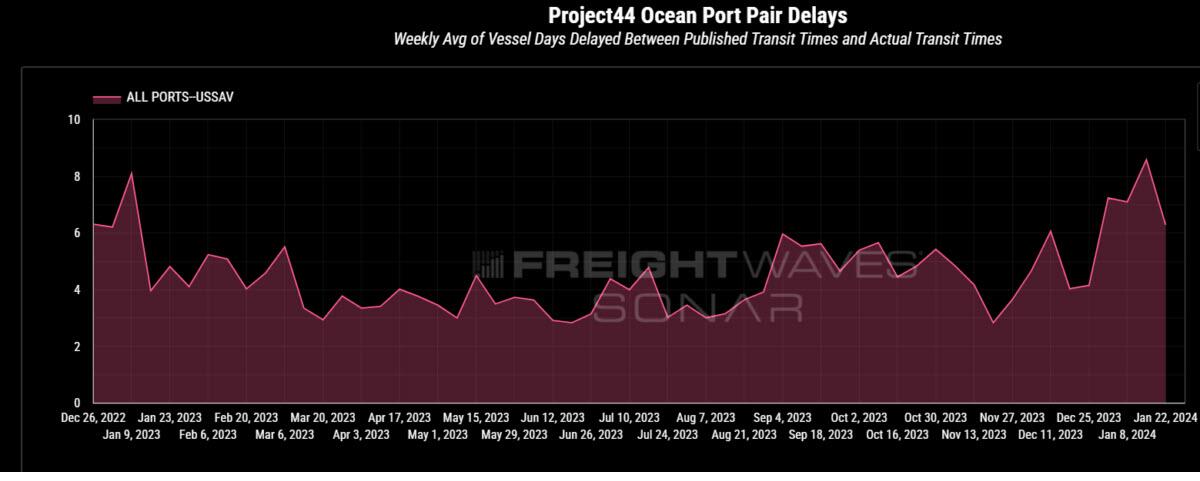

The water crisis is creating increased delays as backlogs around the canal remain.

{kind=link}

The limiting effects of the low water levels have created an additional six-day delay on average to the Port of Savannah from all ports around the globe. These delays are adding an extra day and a half to the scheduled transit times, which have also increased — nearly four days longer than they were this time last year.

These delays are even more impactful the further up the Eastern Seaboard you go. The Port of New York and New Jersey is having similar delays, around the six-day mark, but are over three days longer than they were last year.

Comparing these East Coast ports to their West Coast counterparts, the port pair delays for the Port of Los Angeles are under three days and nearly a day less than they were this time last year.

Mother Nature is outside human control, and if the water level projection holds true, the next couple of months could add to the ongoing crisis.

Tyler Durden

Thu, 02/08/2024 – 22:25