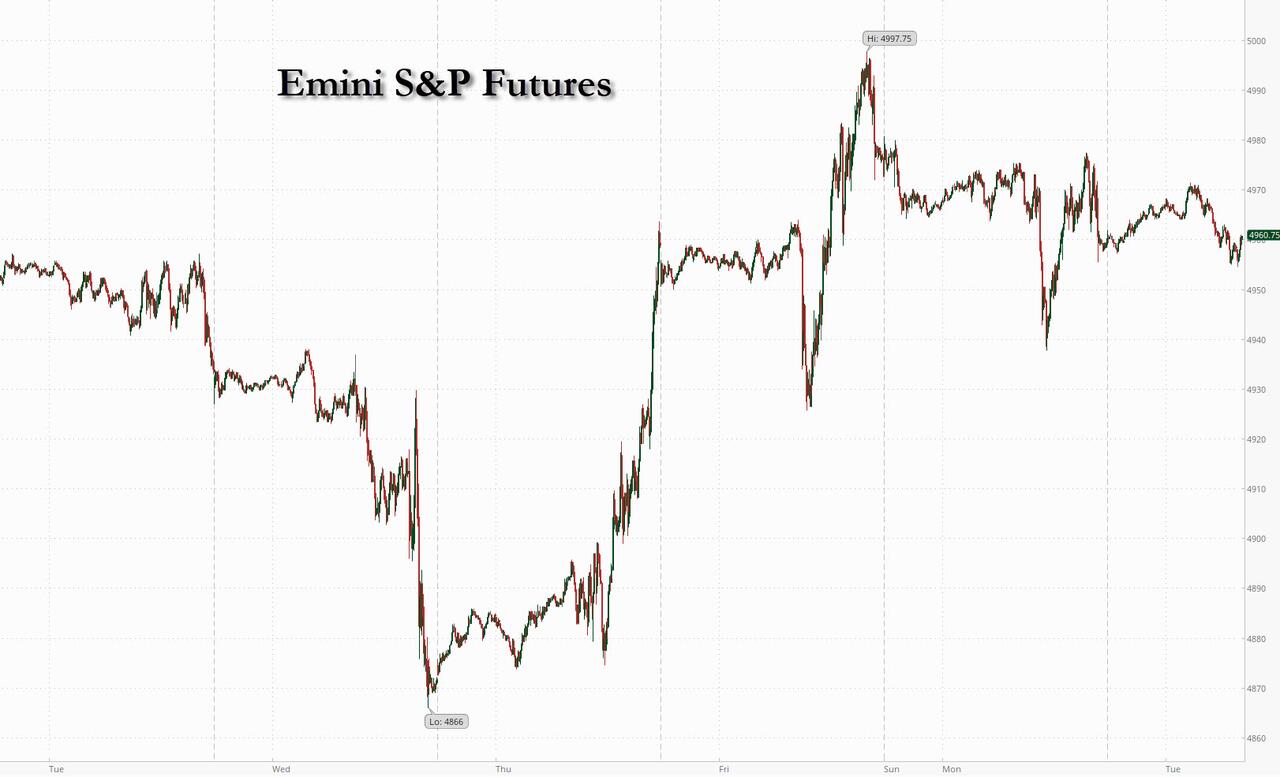

Futures Flat As Interest Rates Grind Higher After Two-Day Surge

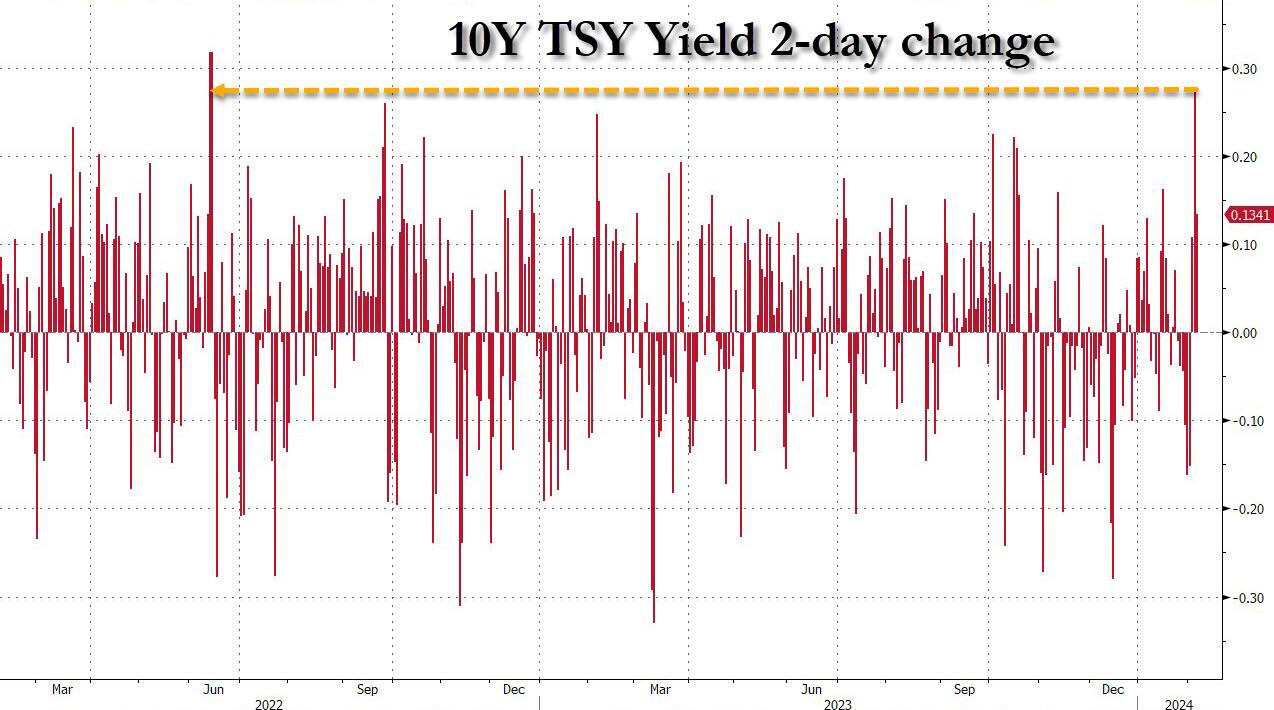

US index futures traded flat on Tuesday, with European markets fading earlier gains while Chinese stocks surged on fresh hopes of government intervention in markets, as continued euphoria about artificial intelligence lifted the shares of Nvidia though broader indexes drifted. As of 7:50am, S&P 500 futures were little changed to 4,960, as 10-year Treasuries continued their drop, if at a more modest pace, with yields rising 2bps to 4.16% after yields soared about 14 basis points in the previous session and following the biggest 2-day selloff in months. Nasdaq futures were fractionally in the red. The small uptick in Treasuries pushes US 10-year yields down 1bps to 4.15% – they rose almost 28bps in the prior two trading sessions. The dollar and gold were also flat, while oil rebounded after several days of losses.

{kind=link}

Ten-year Treasuries posted small moves after yields soared about 28 basis points in the previous two sessions.

{kind=link}

In premarket trading, Palantir surged as much as 20% after giving a higher-than-expected profit outlook on demand for artificial intelligence products. Eli Lilly rose 3% after forecasting 2024 sales ahead of Wall Street estimates as the company rolls out Zepbound, its weight-loss shot. Here are the other notable premarket movers:

Chegg shares dropped 6.6% after the online educational services company’s projections for first-quarter revenue and adjusted Ebitda fell short of consensus expectations.

Coherent shares jump 9.7% after the maker of optoelectronic components posted second-quarter results that beat expectations, with analyst positive on demand for the company’s AI-related datacom transceivers and potential for growth.

FMC shares slid 15% after the pesticide maker’s first-quarter and full-year earnings outlook trailed expectations. The company also reported fourth-quarter revenue that missed estimates.

Palantir Technologies jumped 18% after the software and analysis company reported better-than-expected fourth-quarter results as demand for its artificial intelligence products boosted sales.

NXP Semi shares rose 2.5% as the chipmaker reported better-than-expected fourth quarter revenue and adjusted EPS. Analysts noted that 4Q results were largely inline, while KeyBanc says that the 1Q forecast weighed down by weakness in auto and industrial segments.

Symbotic shares slumped 19% after the robotics warehouse automation company’s forecast for second-quarter adjusted Ebitda missed estimates. Additionally, the company reported first-quarter loss per share that was bigger than expected.

United Parcel Service advanced 2.5% after UBS raised its recommendation on the stock to buy from neutral. The broker said upgrade is based on expectations that management will deliver “a strong cost reduction program to support margin expansion and attractive EPS growth.”

US-listed Chinese stocks rally across the board in premarket trading Tuesday following a slew of announcements from officials in Beijing aimed at bolstering the stock market. Bloomberg reported that regulators planned to brief President Xi Jinping on the financial market as soon as Tuesday.

Varonis Systems rose 7.2% after the data security firm’s 4Q results and outlook for full-year recurring revenue beat expectations. The company said its transition to a Software-as-a-Service model should be complete by end-2026, a year ahead of its initial plan, an announcement that led several analysts to nudge up their price targets on the stock.

After last week’s FOMC which pushed back on a March (and even May) rate cut, a raft of Fed officials are set to speak this week, which may add additional insight into the central bank’s thinking. Strong US economic data has forced traders to reduce their bets on interest rate cuts and Chair Jerome Powell reiterated his wait-and-see approach in an interview on Sunday. While market pricing once made a first quarter-point Fed cut in March look like a near-certainty, those odds have now dwindled to around 10%. The Fed’s Loretta Mester and Patrick Harker are due to speak on Tuesday, with Adriana Kugler and Tom Barkin slated for the following day.

“Wary sentiment from central bankers, cautious about stubborn inflation, may hold back gains again on Wall Street,” said Susannah Streeter, head of money and markets at Hargreaves Lansdown. “Policymakers still want to keep a tighter rein on demand, so high borrowing costs are likely to linger for longer.”

European stocks and US futures surrendered earlier gains while bond markets steadied after the biggest two-day selloff in months. The Stoxx 600 is little changed, with energy and bank shares among the best performers. The energy sector outperforms as BP rallies after beating profit estimates and accelerating its share buybacks. Infineon falls after guiding for lower-than-expected revenue this year and UBS drops after reporting a slightly worse-than-expected fourth-quarter loss. Here are the most notable European movers:

Shares in BP rise as much as 6.9% to the highest since November after fourth-quarter profit beat estimates and the oil major announced an accelerated buyback program. The plan to repurchase $1.75 billion of shares each quarter in the first half of the year is a “welcome positive,” RBC says.

Shares in BE Semiconductor gain as much as 4.6% to an intraday record, after Exane initiates coverage with an outperform rating and a Street-high price target, describing the chip packaging equipment maker as a “future AI enabler.”

Shares in MorphoSys jump as much as 16% to €66.58 in Frankfurt after Novartis agreed to buy the German biotech for €68 per share. The shares closed 36% higher on Monday after a Reuters report about the deal, which was confirmed after the close. Analysts say the deal fits in with Novartis’ strategy and expect a smooth integration. Novartis shares rise as much as 0.9%.

Shares in Aurubis rise as much as 5.6%, erasing earlier losses after the German metals company reported results, with Baader seeing long-term positives after a difficult year. Analysts highlighted uncertainty around management succession.

Shares in Demant gain as much as 9.2% after the Danish hearing-aid and audio-equipment maker provided an outlook for 2024 and said it will undertake a strategic review of its communications business. A sale of this asset could unlock value for shareholders, according to Jefferies analysts.

Shares in UBS decline as much as 3.4% after the Swiss lender’s fourth-quarter earnings miss disappointed analysts, even as it announced a better-than-expected dividend. The bank said it will resume share buybacks this year.

Shares in Nordic Semiconductor tumble as much as 23%, the most since 2018, after giving a first-quarter revenue forecast that was much weaker than expected. The company cited continued inventory corrections, yet Morgan Stanley analysts say the firm’s outlook, which is more pessimistic than peers, raises questions over its competitive footing.

Shares in LVMH slip as much as 0.9% as the luxury-goods maker is downgraded to hold from buy at HSBC, with analysts saying that, while the shares have seen a “well-deserved” post-results squeeze, sales growth in the first half is still expected to be muted.

Shares in Infineon fall as much as 3% after the chipmaker reduced full-year guidance, noting a slowdown of demand for automotive chips outside of China and a delayed recovery in some other segments.

Shares in Alfa Laval decline as much as 4.2%, the most since March and the biggest drop in Stockholm’s OMX 30 benchmark, after the Swedish industrial equipment firm reported disappointing 4Q figures, including a miss on earnings per share.

The biggest market moves were in Asia which advanced to head for their highest in three weeks, after Chinese equities soared on speculation authorities are planning more forceful efforts to end the rout.Regulators plan to brief President Xi Jinping on the market as soon as Tuesday. The Hang Seng China Enterprises Index jumped almost 5%, while a broader gauge of emerging market equities headed for its biggest advance this year. “While the bounce today is strong and certainly welcome, investors will probably want more concrete actions to be taken by policy makers,”said Eugene Leow, fixed income strategist at Dbs Bank Ltd. “Sentiment on Chinese assets has been in the doldrums for some time.”

The MSCI Asia Pacific Index rose as much as 0.8% amid news on measures in China to stem the stock rout, including tightening trading restrictions on domestic institutional investors and some offshore units — as well as a Bloomberg report that regulators in China plan to update the top leadership on market conditions and policy initiatives as soon as Tuesday.

The Hang Seng Index gained the most since July, and the CSI 300 advanced the most since November 2022. Central Huijin Investment, a key unit of the nation’s sovereign wealth fund, vowed to continue purchasing exchange-traded funds.

“Huijin’s purchase will guide and encourage more funds to buy and also confirms the market speculation on more state buying recently,” said Zhou Nan, investment director at Long Hui Fund Management. “There’s very limited room for further slide, but the market may continue to fluctuate before the bottom can be solidified,” he said.

In FX, the Bloomberg Dollar Spot Index is unchanged; front-end risk reversals in the Bloomberg Dollar Spot index closed at the highest level since Nov. 13 on Monday as traders turned focus to next week’s US CPI data. The Aussie tops the G-10 FX pile, rising 0.2% versus the greenback after the RBA left interest rates on hold and said further hikes could not be ruled out. The AUDUSD rose as much as 0.6% 0.6521 to erase week-to-date losses. Leveraged buying kicked in as rate differentials to US yields were seen contracting post the decision, traders said. “What worries me most, is that we don’t manage to bring inflation back down to target without collateral damage, more damage in the labor market that we’d like,” RBA Governor Michele Bullock said at a press conference following the decision.

In rates, the treasuries curve edged steeper with yields narrowly mixed and front-end outperforming slightly on the day. US yields richer by 1bp-2bp across front-end of the curve with long-end yields slightly cheaper on the day, steepening 2s10s, 5s30s spreads by 1bp-2bp vs Monday’s close; the 10-year yield is higher by 2bps at 4.1675%in a narrow daily range after climbing 28bp over past two sessions, outperforms bunds and gilts in the sector by 2.5bp and 1bp. Gilts underpinned in London session following strong demand for UK green bonds. Treasury auctions resume at 1pm with $54b 3-year note sale, followed by $42b 10-year and $25b 30-year new issues Wednesday and Thursday. WI 3-year yield at ~4.228% is around 12bp cheaper than January’s stop-out, which stopped through by 1.1bps. US session features several Fed speakers and start of Treasury auction cycle with 3-year note sale.

Oil prices are close to flat, with WTI trading near $72.80. Spot gold is also little moved on the day at around $2,024.

Bitcoin holds above the USD 43k mark, and Ethereum (+2.2%) continues to outperform, taking the coin above USD 2.3k.

Looking to the day ahead now, the US econ calendar is empty while data releases in Europe include German factory orders and Euro Area retail sales for December, the German and UK construction PMIs for January, and the ECB’s Consumer Expectations Survey for December. Otherwise, central bank speakers include the Fed’s Mester, Kashkari and Collins. And today’s earnings releases include Ford.

Market Snapshot

S&P 500 futures little changed at 4,966.25

STOXX Europe 600 up 0.2% to 484.75

German 10Y yield little changed at 2.32%

Euro little changed at $1.0744

MXAP up 0.7% to 166.94

MXAPJ up 1.3% to 511.39

Nikkei down 0.5% to 36,160.66

Topix down 0.7% to 2,539.25

Hang Seng Index up 4.0% to 16,136.87

Shanghai Composite up 3.2% to 2,789.49

Sensex up 0.6% to 72,177.50

Australia S&P/ASX 200 down 0.6% to 7,581.58

Kospi down 0.6% to 2,576.20

Brent Futures down 0.3% to $77.79/bbl

Gold spot down 0.0% to $2,024.56

US Dollar Index little changed at 104.41

Top Overnight News

European stocks rose, bolstered by strong results from BP Plc, while global bond markets steadied after the biggest two-day selloff in months.

Australia’s central bank kept interest rates unchanged and signaled further tightening remains possible, joining global peers in pushing back against expectations for near-term easing and sending the currency and bond yields higher.

Anticipation is mounting for more forceful Chinese government efforts to end the nation’s stock rout, with regulators planning to brief President Xi Jinping on the market as soon as Tuesday.

Reliable sources of liquidity are at the top of traders’ minds as they brace for another year of turbulence, according to a JPMorgan Chase & Co. electronic trading survey.

A more detailed look at global markets courtesy of Newsuqawk

APAC stocks were somewhat mixed as Chinese market stabilisation efforts offset the early headwinds from Wall Street where yields climbed to YTD highs after hot ISM Services data and recent hawkish Fed rhetoric.ASX 200 declined with weakness in tech and real estate amid rising yields, while attention was also on the RBA which maintained its rates as expected and reiterated its hawkish rhetoric. Nikkei 225 was subdued after disappointing household spending and soft wage data but with the downside cushioned amid a slew of earnings releases. Hang Seng and Shanghai Comp outperformed with sentiment boosted by China’s latest market stabilisation efforts including reports China’s sovereign fund will further increase ETF holdings, while the CSRC also encouraged listed firms to buy back more shares to inject more capital into the A-share market.

Top Asian News

China’s securities regulator said it encourages listed firms to buy back more shares to inject more capital into the A-share market and make every effort to maintain stable market operations, while it will guide institutional investors to increase stock investment. Furthermore, it was later reported that Chinese President Xi is set to discuss China’s stock market with regulators.

Chinese sovereign wealth fund CIC’s unit Central Huijin said it fully recognises A-shares’ allocation value and increased ETF holdings recently, while it will continue to increase holding size, according to Bloomberg.

US President Biden’s administration sent five senior Treasury officials to Beijing this week for economic talks including on subsidies and China’s “non-market” policies that are ending excess industrial capacity, according to a Treasury official cited by Reuters.

RBA kept rates unchanged at 4.35%, as expected, while it reiterated that the board remains resolute in its determination to return inflation to the target and that a further increase in interest rates cannot be ruled out. RBA also repeated that returning inflation to the target within a reasonable timeframe remains the board’s highest priority and although it noted that inflation continued to ease in the December quarter, it added that inflation remains high at 4.1%. Furthermore, it stated the Board needs to be confident that inflation is moving sustainably towards the target range and said that inflation is still weighing on people’s real incomes and household consumption growth is weak, as is dwelling investment. RBA’s quarterly Statement on Monetary Policy lowered the forecasts for inflation and GDP, while it noted that risks to the outlook are balanced and stated the level of demand is still above the economy’s capacity to supply, creating price pressures.

RBA Governor Bullock said at the press conference that the situation is more back to normal than during the pandemic and that everyone is focused on inflation, while she added there is still more work to do and still a little way to go to get inflation down. Furthermore, she stated that risk remains that inflation expectations drift further and they are not ruling anything in or out on policy, while they need to be convinced on inflation before thinking of cutting rates.

BoJ is on track for a policy shift by April, via Reuters citing sources; assisted by wage outlook. Piece adds that the BoJ is laying the groundwork to end NIRP by April and overhaul other policy framework areas, but likely to go slow on subsequent action

European bourses are mixed, having initially traded entirely in the green taking impetus from positive Chinese trade overnight; the FTSE 100 outperforms post-BP (+5.9%) earnings.European sectors are mixed; Energy is the clear outperformer propped up by strength in Energy after BP’s strong results. To the downside, Utilities is hampered by a broker downgrade at RWE (-1.1%) and UBS (-2.9%) numbers are weighing on Financials. US equity futures (ES -0.1%, NQ +0.2%, RTY -0.4%) are mixed with outperformance in the NQ lifted by improved sentiment within the Tech sector and as NVDA (+1.4%) looks to breach the USD 700/shr level for the first time.

Top European News

Barclays noted that UK January consumer spending rose 3.1% Y/Y with more consumers shopping online due to cold weather, while consumer confidence about personal finances was at the highest since November 2021.

ECB’s de Cos says is confident that inflation is returning to the 2% target

ECB Consumer Inflation Expectations survey (Dec) – 12-months ahead 3.2% (prev. 3.5%); 3-year ahead 2.5% (prev. 2.4%). Economic growth expectations for the next 12 months remained unchanged at -1.3%

FX

Dollar remains at elevated levels after a combination of NFP, hawkish Fed speak and strong ISM sent the DXY to a YTD peak at 104.60 yesterday. DXY remains above its 100DMA at 104.21, though not much in the way of upside until 105.

EUR still in a downtrend since late-Dec; currently remains in place after the pair took out its 100DMA to the downside yesterday at 1.0783 and printed a YTD trough at 1.0723.

The JPY is relatively steady vs. the USD after advancing to a fresh YTD peak yesterday at 148.89. Fate of the pair will ultimately depend on the relative Fed vs. BoJ policy path.

AUD is the G10 outperformer following the “hawkish hold” from the RBA and strong Chinese equity performance overnight. That being said, it was unable to maintain 0.65+ status with yesterday’s YTD trough of 0.6486 in close proximity.

PBoC set USD/CNY mid-point at 7.1082 vs exp. 7.2057 (prev. 7.1070).

Fixed Income

USTs are a touch firmer, though has been edging off best levels throughout the European morning. Yields are lower across the curve with modest bull-flattening; the docket for today includes supply (3yr) and Fed speak from Mester, Collins, Harker & Kashkari, trough for today at 110-26.

Bunds are a touch firmer as the complex generally rebounds from the post-NFP/Powell/corporate-supply induced pressure of Monday’s session. Thus far, broader macro drivers are relatively limited with the complex unreactive to German Industrial data and an ECB survey.

Gilts is the modest outperformer, though this follows recent underperformance as BoE expectations have been subject to a more hawkish re-pricing.

Spain has started the 30yr syndicated bond sales with EUR 50bln in initial demand, according to the lead manager.

Commodities

Crude is modestly firmer, having initially started the session on a softer footing, with overall specifics light for the complex; currently, Brent holds just above USD 78/bbl.

Spot gold is around flat and unable to benefit from the modest pullback in the Dollar and lower yield environment; resides just under the 21-DMA at USD 2029/oz, 50-DMA above at USD 2034/oz.

Base metals are bid, deriving support from the firmer APAC handover given the strength seen in China from support measures into the Lunar New Year celebration period.

Citi: TTF prices could average USD 8.5/MMBTU in Q1 (circa. EUR 27/MWh), but then surpass USD 10/MMBTU during Q2.

Petrobras CEO said the Co. will expand refining capacity by 25% in four years, according to Reuters.

Earnings

NXP Semiconductors NV (NXPI) – Q4 2023 (USD): Adj. EPS 3.71 (exp. 3.65), Revenue 3.42bln (exp. 3.39bln). Co. said it is navigating a soft landing by managing what is in its control, especially limiting over shipment of products to customers. Sees Q1 Adj. EPS USD 2.97-3.38 (exp. 3.17). Sees Q1 revenue USD 3.03bln-3.23bln (exp. 3.17bln). (Newswires) Shares +2.8% pre-market

Palantir (PLTR) – Q4 23 (USD): Adj. EPS 0.08 (exp. 0.08), revenue 608mln (exp. 602mln). Q124 revenue view 612-616mln (exp. 617mln). FY revenue view 2.652-2.668bln (exp. 2.66bln). Said demand for large language models from commercial institutions in the US continued to be “unrelenting,” and it is focussed on the rollout of its AI; adds momentum with AI product is now significantly contributing to new revenue and new customers. Sees Q1 revenue between USD 612-616mln (exp. 617mln), Q1 operating income seen at USD 198mln (exp. 171mln); for the FY, revenue seen between USD 2.652-2.668bln (exp. 2.66bln), and operating income seen between USD 834-850mln (exp. 760mln). (Newswires) Shares +18.4% pre-market

Semiconductors – US Commerce Secretary Raimondo said the US will announce several more semiconductor chips funding announcements over the next six to eight weeks, adding that there was no artificial timeline, adding that the US will award funds as quick as possible.

BP (BP/ LN) – Q4 (USD): EPS 0.18 (exp. 0.15), adj. EBITDA 10.56bln (exp. 9.2bln), Profit 0.4bln (prev. 4.9bln), adj. for inventory holding losses of 1.2bln and adverse 1.5bln impact. USD 1.75bln buyback & dividend of USD 0.07270/shr, +10% Q/Q for Q1. USD 3.5bln buyback in H1 2024, plans buybacks of at least USD 14bln through 2025. Q1 Guidance: Upstream production higher vs Q4. Customer business: expects seasonally lower volumes across most businesses and the absence of one-off positive effects from Q4. Expects fuels margins to remain sensitive to movements in cost of supply. Products: expects a significantly lower level of refinery turnaround activity vs Q4. “expects lower industry refining margins, with a larger reduction in realized margins due to narrower North American heavy crude oil differentials.” 2024 Guidance: Reported and underlying upstream production to be slightly higher vs 2023. Customers: expects continued growth from convenience. Products: lower level of industry refining margins, with realized margins impacted by narrower North American heavy crude oil differentials and for “refinery turnaround activity to have a similar impact on both throughput and financial performance compared to 2023, with phasing of activity in 2024 heavily weighted towards the second half.” Gulf of Mexico oil spill payments to be around 1.2bln pre-tax, incl. 1.1bln to be paid in Q2. In other news, Whiting, Indiana refinery (435k BPD) is continuing assessment following a power outage, according to Reuters. (Reuters/Newswires) Shares +5.4% in European trade

Infineon (IFX GY) – Q1 (EUR): EPS 0.44 (exp. 0.46), Revenue 3.7bln (exp. 3.83bln). Cuts outlook citing market environment outside automotive remains weak and does not expect noticeable recovery in demand until H2’24. Guides Q2 Revenue approx. 3.6bln (exp. 4.1bln). Segment result margin approx. 18%. Provides FY24 Guidance: Cuts FY24 Revenue 15.5-16.5bln (exp. 18.2bln, prev. guidance 16.5-17.5bln), adj. gross margin “low to mid 40s %” (prev. guidance 45%), adj. FCF 1.8bln (prev. guidance 2.2bln). (Newswires) Shares -3.0% in European trade

Geopolitics

US Central Command said its forces conducted a strike in self-defence against two Houthi explosive uncrewed surface vehicles, according to Reuters.

Yemen’s Houthis says they targets one US and one British ship with naval missiles, via group’s spokesperson

US Event Calendar

Nothing major scheduled

Central bank speakers

12:00: Fed’s Mester Speaks on Economic Outlook

13:00: Fed’s Kashkari Participates in Moderated Discussion

14:00: Fed’s Collins Delivers Opening Remarks at Labor Market Confere

19:00: Fed’s Harker Speaks on Fed’s Role in Economy

DB’s Jim Reid concludes the overnight wrap

Morning from breakfast now at Heathrow, lunch in Brussels and dinner in Paris. As I type from a very windy airport (always nice as you’re boarding a plane) the bond market sell-off is easing a bit in Asia but it’s generally been a tough 48 hours for rates. That continued yesterday as a bunch of hawkish headlines meant investors priced out the probabilities of rate cuts this year. I n part, that was because markets were catching up to Fed Chair Powell’s ’60 Minutes’ interview over the weekend that we discussed yesterday, which didn’t signal much hurry to cut rates. But on top of that, we got some hawkish comments from Minneapolis Fed President Kashkari, whilst the ISM services index also surprised on the upside, with a significant jump in the prices paid component. So there was plenty of fresh momentum behind the selloff. Indeed, since the jobs report on Friday, the 10yr Treasury yield has risen by +27.8bps, which is the biggest 2-day jump since June 2022, back when the Fed suddenly geared up to hike by 75bps for the first time since the 1990s. So we shouldn’t underestimate the moves or the volatility.

In terms of those drivers, the first (to briefly echo comments from yesterday) was the ‘60 Minutes’ interview, where Powell said that the “danger of moving too soon is that the job’s not quite done”. Moreover, the interview was recorded before the jobs report came out, so it’s reasonable to assume that things may have got a bit more hawkish since. That meant Treasuries had already got the day off to a rocky start, but that was then cemented by a blog post from Minneapolis Fed President Kashkari. He said that “ It is possible, at least during the post-pandemic recovery period, that the policy stance that represents neutral has increased.” And in turn, he wrote that “gives the FOMC time to assess upcoming economic data before starting to lower the federal funds rate”. So that echoes remarks from other officials, which suggests they’re not in a rush to start rate cuts.

Aside from the hawkish remarks, the latest round of data gave the selloff a further push, as the ISM services index surprised on the upside at 53.4 (vs. 52.0 expected). And significantly, the prices paid subcomponent surged to an 11-month high of 64.0 (vs. 56.7 expected), which added a warning that inflationary pressures are still around. So that will be concerning to the Fed, particularly since Powell commented that inflation was still yet to hit their target on a 12-month basis.

Later in the day we also got some more positive data from the Fed Senior Loan Officer’s survey (SLOOS). This showed the recent sharp tightening of credit conditions moderating in Q4, with credit standards for commercial & industrial loans tightening at their slowest pace in seven quarters. Credit conditions remain tight but the downside risks for activity suggested by the SLOOS are easing.

On the topic of greater US economic optimism, our US economists released an updated outlook overnight. The key change is that they no longer expect a mild recession to emerge during H1-24 and now foresee 2024 real GDP growth at a solid 1.9% (Q4/Q4). They continue to anticipate that the first rate cut will come in June but that the Fed will only cut rates by 100bps this year. See their full report here.

With the upbeat macro backdrop in mind, investors dialled back their expectations for rate cuts this year, adding to the moves after the jobs report on Friday. For instance by the close, futures were pricing in just a 17% chance of a March cut, the lowest in over two months. And looking at the year as a whole, only 113bps of cuts were priced in by the December meeting, which is the lowest so far in 2024, and a reduction of -11.6bps relative to Friday and down from 168bps at the peak on January 12. So it’s clear that markets are now anticipating a significantly more hawkish profile over the months ahead, with roughly 4-5 cuts priced in for 2024, down from 6-7 just over three weeks ago.

Given the combination of hawkish comments, strong data, and fewer cuts being priced, it was a bleak day for sovereign bonds. US Treasuries were at the forefront of that, with the 10yr yield up +13.7bps to 4.16%. And it meant the 2-day increase now stands at +27.8bps, the largest since June 2022. Meanwhile at the front-end, the 2yr yield rose another +10.8bps to 4.47%, bringing the 2-day increase up to +26.9bps, which is the largest since last March shortly after the regional banking turmoil. Both 2 and 10yr yields are rallying back 3-4bps in Asia though. Before that overnight rally the US rates sell-off boosted the dollar, with the broad dollar index (+0.51% yesterday after +0.85% Friday) seeing its strongest 2-day rally since this time last year. It’s only off a tenth of a percent in Asia this morning.

Yesterday’s moves for US Treasuries were echoed in other markets, with yields on 10yr bunds (+7.5bps), OATs (+7.0bps) and BTPs (+6.9bps) seeing significant moves of their own. And similarly, investors grew more sceptical about the chance of ECB cuts happening soon, with the probability of a cut by the April meeting down to 68%, having been at 75% on Friday. So there’s a growing sense that the major central banks might wait until later in Q2, if not beyond, before they feel confident adjusting their policy rates.

The prospect of fewer rate cuts meant that equities struggled as well. The S&P 500 (-0.32%) came off its record high on Friday. While the S&P did partially recover after trading -0.8% down early in the session, the decline was broad with 83% of its constituents lower on the day. In keeping with a theme from this year, it was small-cap stocks that suffered in particular, with the Russell 2000 down -1.30%, whilst the equal-weighted S&P 500 (-0.86%) was back into negative territory for 2024 so far. There were continued losses for regional banks as well, with the KBW Regional Bank Index (-1.85%) seeing all 47 members lose ground. That included a further loss for New York Community Bancorp (-10.6%), which followed the news from Fitch Ratings after Friday’s close that they were downgrading NYCB to BBB- from BBB. Chipmakers were the notable outperformer, with the Philadelphia semiconductor index up +1.18%, led by a +4.77% gain for Nvidia. However, this did not translate into broader tech gains, with the Magnificent 7 down -0.24%. Over in Europe, the STOXX 600 (-0.05%) posted a marginal decline.

Chinese stocks have been rallying hard overnight, especially just before we go to print as measures continue to be rolled out to halt the recent slump. In addition it’s being reported that the Chinese securities regulator is preparing a report on the stock market for President Xi which perhaps helps explain the seriousness of the situation. In fast markets the Hang Seng (+3.3%), the CSI (+2.6%) and the Shanghai Composite (+2.3%) are all higher. Other Asian markets are a bit lower with the Nikkei (-0.32%), the KOSPI (-0.70%) and the ASX (-0.69%) down with Aussie markets reacting to the RBA leaving rates unchanged but with a comment that further hikes couldn’t be ruled out even if the tone is towards the next move being a cut.

The central bank in its statement highlighted that inflation remains too high despite it falling in recent months. It would still consider more rate increases if price pressures remained sticky. Following the decision, the Aussie rose +0.49%, to trade at 0.652 versus the dollar. Meanwhile, the RBA has slightly lowered its near-term inflation forecasts, expecting it to be within its 2% to 3% target band at 2.8% by the end of 2025, before achieving the midpoint of the band by around mid-2026.

In early morning data, household spending in Japan dipped more than expected in December, falling 2.5% y/y compared with the -2.1% estimate as against a -2.9% prior drop. Also, real wages fell for a 21st straight month though at a slower pace, declining -1.9% y/y in December (v/s -1.5% expected), compared to a revised decline of -2.5% in the previous month.

Looking at yesterday’s other data, we did get the final services and composite PMIs from around the world. In the Euro Area, the final January composite PMI was in line with the flash reading, at 47.9. But in the UK there was an upgrade to 52.9 (vs. flash 52.5), whilst in the US there was a downgrade to 52.0 (vs. flash 52.3). Separately, we also heard that Euro Area PPI was at -10.6% in December.

To the day ahead now, and data releases include German factory orders and Euro Area retail sales for December, the German and UK construction PMIs for January, and the ECB’s Consumer Expectations Survey for December. Otherwise, central bank speakers include the Fed’s Mester, Kashkari and Collins. And today’s earnings releases include Ford.

Tyler Durden

Tue, 02/06/2024 – 08:14