FOMC Preview: No More Tightening Bias

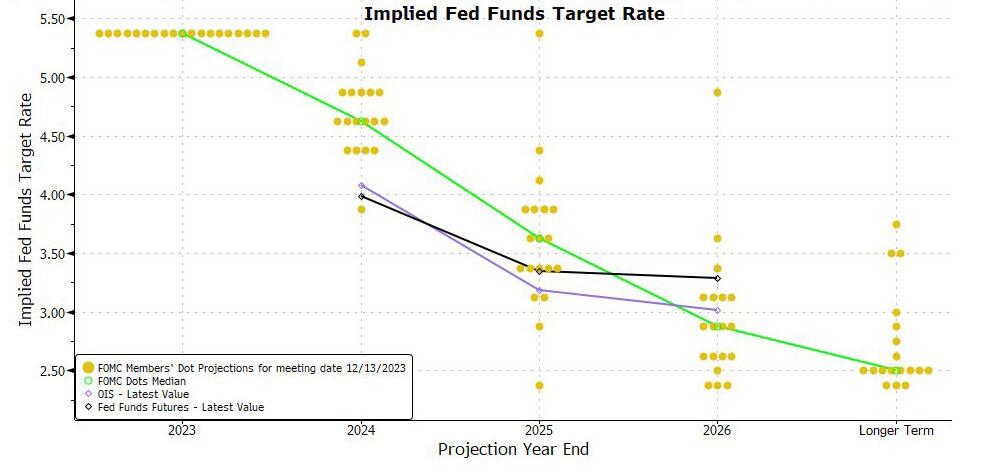

While the market is split about the March – and subsequent – Fed meetings, tomoorrow’s FOMC decision is clear: the Fed will keep rates unchanged at 5.25-5.50% while tweaking the statement further to signal the end of the tightening bias and tipping the balance towards futures rate cuts.And since there are no new Economic Projections (i.e., “Dot Plot”) at this meeting after the December release saw three rate cuts pencilled in for 2024, markets will focus on the statement and Powell’s messaging for clues on the path ahead.

{kind=link}

Here, as Newsquawk notes, theMarch meeting is likely to remain an open question after Powell concludes this week, given the Fed is walking the tightrope of a faster-than-expected fall in inflation against the resilient economic backdrop, causing debate amongst policymakers on how fast to move ahead with rate cuts despite the level of real monetary restrictiveness continuing to drift higher amid concerns the growth strength could keep inflation buoyed moving forward. The market is pricing in just under half a rate cut for the March FOMC, a steep from from December when in the aftermath of the Fed’s dovish pivot, it was briefly expecting 1 full rate cut.

{kind=link}

On the balance sheet, no decision is expected to be made on the pace of the runoff at the January meeting, although it is expected to be an active discussion.

RATE EXPECTATIONS: All 123 economists surveyed by Reuters expect the Fed to keep rates unchanged on Wednesday,with money markets also priced for no change. The central bank is expected to begin cutting rates in Q2, according to 86 of 123 surveyed (55 thought June was more likely, while 31 see a reduction in May) – money markets are pricing a 43% chance of a first cut in March with more than one 25bp cut priced for May.

{kind=link}

Additionally, the Reuters poll shows that most economists (72 of the 123) believe the Fed will cut rates by 100bps or fewer this year– that compares to money market pricing, which currently sees five 25bps rate cuts fully priced, with a good chance of a sixth.

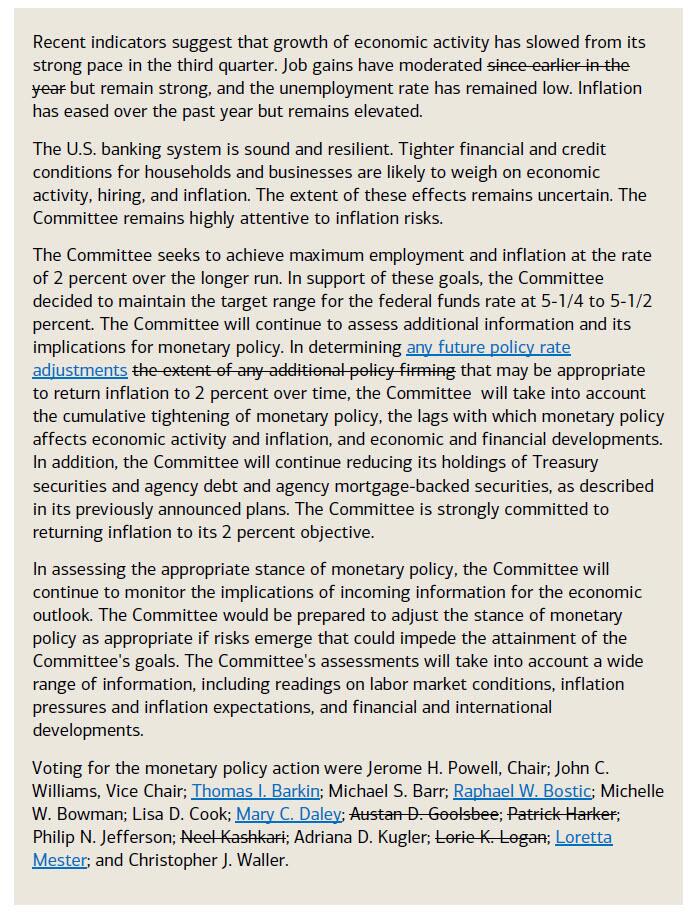

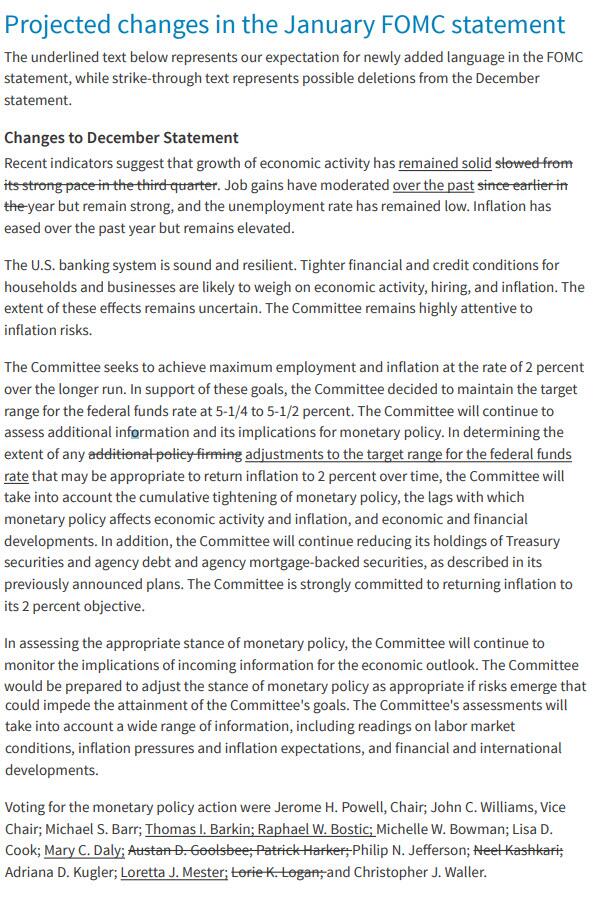

STATEMENT:There are expectations for another dovish tweak to the statement guidance after the December statement’s adjustment: “In determining the extent of ANY [new word] additional policy firming that may be appropriate…”. WSJ’s Timiraos writes, “Fed officials are likely to take a symbolically important step this week by no longer signalling in their policy statement that rates are more likely to rise than fall.”That is a view held by many analysts too. Using the 2006-07 guidance history as a benchmark, BofA suggests the following, “in determining any future policy rate adjustments that may be appropriate…”.There is BofA’s proposed statement redline…

{kind=link}

… and here is Barclays:

{kind=link}

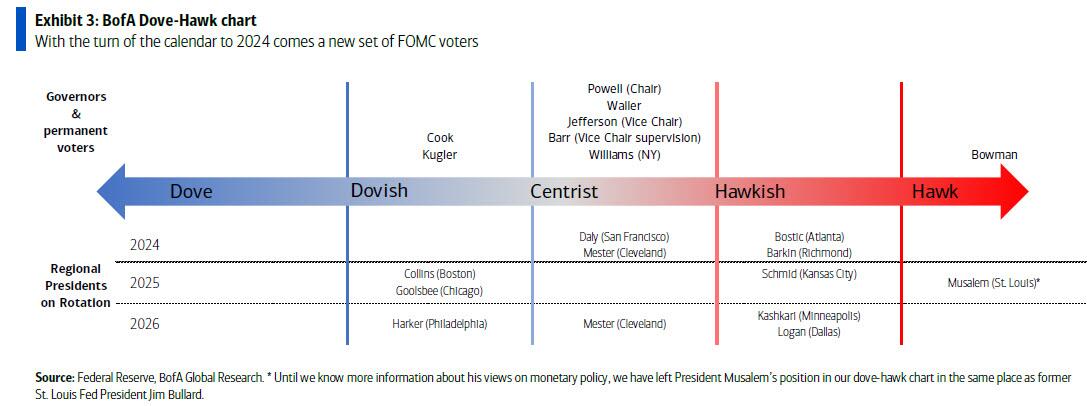

VOTER ROTATION: A more hawkish bent…With the January meeting comes a new rotation of voters on the committee. Rotating onto voting status are Cleveland Fed President Mester, Richmond Fed President Barkin, Atlanta Fed President Bostic, and San Francisco Fed President Daley. Rotating off voting status are Chicago Fed President Goolsbee, Philadelphia Fed President Harker, Minneapolis Fed President Kashkari, and Dallas Fed President Logan. This rotation results in a slightly more hawkish group of FOMC voters given recent communication (see recent comments from Bostic, Mester and Daly). That said, BofA doesn’t put too much emphasis on the views of voters versus non-voters given the trend toward fewer dissents and preference for unanimous decisions. Hence, while the mix of FOMC voters may skew more hawkish in 2023 versus 2024, all voices on the committee matter and can influence the policy decision at any given meeting.

{kind=link}

POWELL:Fed Chair Powell, in his Presser/Q&A, is unlikely to go into specifics on rate cuts beyond acknowledging that they are on the horizon, likely retaining the optionality for a March cut via “data dependence”.Powell may also temper aggressive expectations around policy easing by framing any future rate cuts as “gradual” or “methodical”/”technical”.Powell is also likely to give a nod to discussions over tapering the Fed’s balance sheet runoff.

INFLATION:Core inflation, as measured by the Fed’s preferred index (PCE), rose at 2.9% Y/Y in December, the lowest since early 2021 and beneath the Fed’s December SEP forecast of 3.2%. There is even more focus on the three-month and six-month annualized figures, which have fallen beneath the Fed’s 2% target; the three-month annualized rate now at 1.5% and the six-month annualized rate is now at 1.9%.The large inflation decline through year-end has seen the level of real restrictiveness (Fed policy rate minus inflation) drift higher, with the Fed Funds Rate having been on hold at 5.25-5.50% since August, causing some policymakers to bring forward their discussion and calls for rate cuts as they look to avoid excessive tightening. The pushback against this view is that the disinflation has been heavily led by the decline in goods inflation, whilst services inflation has been much more sticky, which could leave the headline inflation readings above target if the goods disinflation fades.

GROWTH:A major conundrum of rushing into rate cuts is that GDP and the consumer have remained resilient,while there have been little signs of a material breakdown in the labour market despite its gradual rebalancing, leaving inflation at risk of reacceleration, or at least suppressing the chances of returning to 2%.The flash Q4 real GDP reading printed at 3.3%, well above the analyst forecast for 2.0%, which would see 2023 GDP at 2.5%, which is actually a tenth less than the Fed’s SEP forecast of 2.6% but likely far above what is required for the aggressive rate cut cycle priced by markets.

BALANCE SHEET:No decision is expected to be made on the pace of the runoff at the January meeting, although it is likely to be an active discussion, as the December meeting minutes and recent Fed Speak have indicated. That was also suggested by WSJ’s Timiraos, “Fed officials are to start deliberations on slowing, though not ending, [QT] as soon as their policy meeting this month”.The WSJ summarised the rationale in three points:

The current USD 60bln/month pace is twice as fast as its prior QT period, raising the risk that reserves drain too quickly vs the money market’s ability to redistribute reserves,so a cut could allow the Fed to continue the runoff for longer;

The RRP, a proxy for cash surplus, is falling faster than expected, and once that is completely drained, forecasting demand for reserves becomes uncertain;

Officials have expressed a preference for retaining more reserves than the prior QT period.

Analysts have been pencilling in forecasts for a QT taper to begin between March and June.

{kind=link}

Much more in the full FOMC preview folderavailable to pro subs in the usual place.

Tyler Durden

Tue, 01/30/2024 – 23:05