“Stagflation, Border Failure, & Regulatory Dysfunction” – Texas Manufacturing Collapsed In January

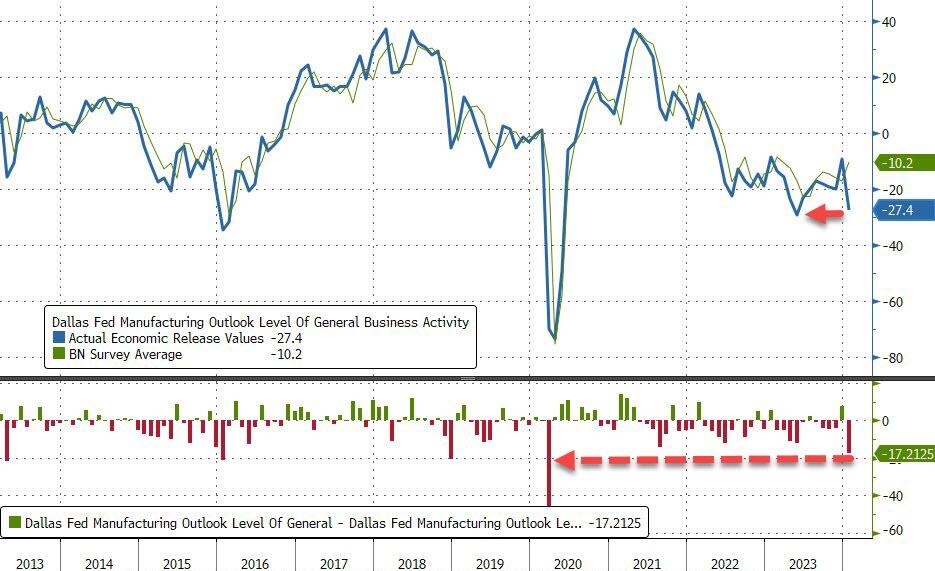

The ‘soft’ data slaughterfest continues with a huge miss for The Dallas Fed’s Manufacturing Outlook survey, plunging from -9.3 to -27.4 (dramatically worse than the -11 expected).

This is the biggest miss since the COVID lockdowns and back to post-COVID lows…

{kind=link}

Source: Bloomberg

And it gets worse…

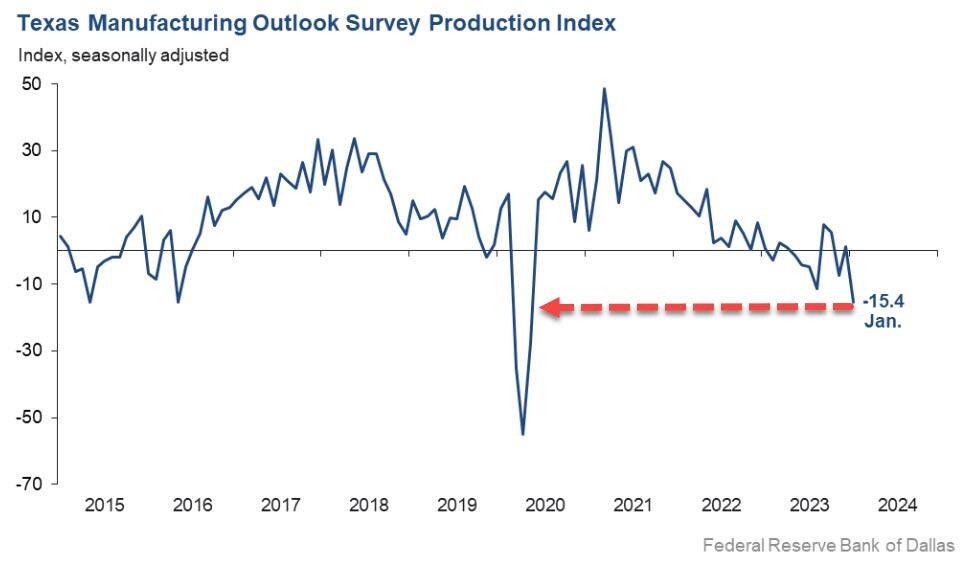

The production index, a key measure of state manufacturing conditions, dropped 17 points to -15.4 – its lowest reading since mid-2020.

{kind=link}

Other measures of manufacturing activity also indicated contraction this month.

The new orders index ticked down from -10.1 to -12.5 in January, while the growth rate of orders index remained negative but pushed up eight points to -14.4.

The capacity utilization index dropped to a multiyear lowof -14.9, and the shipments index slipped 11 points to -16.6.

Perceptions of broader business conditions continued to worsen in January.

Additionally, wage and input costs continued to increase this month.

{kind=link}

Smells like stagflation, which is how some respondents saw it too…

Stagflation, increased commodity costs, labor costs and benefits to retain talented staff, political upheaval, border failure and dysfunction at the regulatory level [are issues affecting our business].

Current macroeconomic conditions are not encouraging. After a busy fourth quarter, the start of 2024 has been slower than planned. My view of 2024 has changed. I had thought 2024 would be a good year, but I see signs of trouble ahead, which will be disruptive.

Demand feels weak right now.

January has been a slower month for sales relative to December (to be expected) and year over year (which was not expected). We are also seeing increasing lead times for inventory and delays at the ports, which we’ve not seen or experienced in several months. Overall, uncertainty is high, and I’m feeling less optimistic than I did last quarter.

The unnecessary, ill-advised postal rate increase conflicts with the already-weakened demand and has undermined any recovery of that type of marketing. Combined with the continued inflationon our raw materials of paper, ink and replacement parts for our machinery, nothing is helping our future.

The current state of the oil market is slowing.This is resulting in a noticeable reduction in new orders. The first and second quarters of the year will be challenging. Things may pick up near the end of the third quarter, best-case scenario. Worst-case scenario, fourth quarter or early 2025.

In order to improve our business outlook, we are adding product offerings through capital expenditures. Legacy business is declining due to competition outside of the U.S.

Our segment of the manufacturing industry is under attack with unfair trade practices. We were successful around 10 years ago in slowing down China from dumping extrusions. A coalition of companies within our industry filed unfair trade charges last year against 15 countries. Initial rulings by the International Commerce Commission last year indicate our industry has been severely damaged, which means our trade case is moving to the next step, and anti-dumping and countervailing duties more than likely are forthcoming.

Lots of bad vibes out there.But orders are not down as much as I would have expected.

We expect softening of demand in the first half of 2024, with partial recovery forecasted for the second half.

Federal Reserve rate-hike levels have all but stopped demand. There is no way to forecast six months forward.

We are very concernedabout our credit line renewal in February, the loan amount being decreased and rate costs increasing.

It has been a slow start to the year as we thought business would pick up after the holidays, however, it has not. Based on current business activity, this may be a rough year.

We are investing short term in new manufacturing equipment because our competitors are now asking us to manufacture their equipment. This is increasing our sales and production of finished goods to the point that we are buying larger quantities of raw materials.

The election is the greatest influencer presently. Oil prices and Middle East “anxiety” have an adverse impact. Extreme cold after a seemingly inordinately hot summer have also added some incongruity to our production.

We have seen a decrease in quote opportunities, quote requests and sales orders. I am not sure the reason why.

[Our] heads [will be] in the sand for the next 18 months.

Which is all very odd because President Biden and Janet Yellen told us that everything is awesome and Bidenomics is doing what it’s supposed to do…?

Tyler Durden

Mon, 01/29/2024 – 10:45