Defying Inflation, Americans Have Kept Spending Money

U.S. retail sales grew more than expected in December, rounding off a surprisingly strong year in terms of consumer spending, as Americans continued to spend money in defiance of inflation and high interest rates. According to advance estimates from the U.S. Census Bureau, total retail and food services sales – including spending at stores, online and in restaurants – amounted to $709.9 billion in December, up 0.6 percent from the previous month and 6 percent compared to December 2022.

Considering that consumer prices grew by 3.4 percentin December, retail sales outpaced inflation last month, meaning that consumers actually spend more than 12 months earlier, even adjusted for inflation. When measured in constant 1982-1984 dollars, retail sales increased 2.2 percent year-over-year in December, marking the highest increase since February 2022.

As Statista’s Felix Richter shows in the following chart, most of the increase in retail sales over the past two years can be attributed to rising prices, as shoppers have spent more bucks for the same bang.

You will find more infographics at Statista

Between December 2021 and December 2023, monthly retail and food services sales (adjusted for seasonal variations, holiday and trading day differences) have increased by 12 percent.

Adjusted for CPI inflation, sales have almost flatlined over the past two years, increasing less than 2 percent over the 24-month period.

That in itself is remarkable, however, as it means that consumers have kept their buying behavior roughly the same despite surging prices.

However, in order to maintain that quality of life, Americans have decimated their savings, and taken on more and more debt…

{kind=link}

In fact the latest data from The Fed shows that consumer borrowing increased much faster than expected during the month of December…

US consumers did not rein in their spending this past holiday season, and now have near-record-breaking debt balances to show for it, according to new Federal Reserve data released Monday.

Consumer borrowing spiked by $23.75 billion in November, more than doubling economists’ expectations for a $9 billion increase and sending outstanding credit balances north of the $5 trillion mark for the first time on record, the Fed’s latest Consumer Credit report showed.

The monthly increase during the critical holiday shopping month was driven by higher rates of revolving credit (which includes mostly credit cards), which soared by nearly $19.5 billion — the third-highest monthly increase on records that go back to 1943.

For quite a while, U.S. consumers were able to handle rapidly rising debt levels, but now it appears that we are reaching a breaking point.

In fact, we are being told that “delinquencies are at their highest level since 2012”…

However, the sharp increase in credit balances is starting to be a cause for concern, Ted Rossman, Bankrate senior industry analyst, told CNN via email.

“Credit card usage and Buy Now, Pay Later usage seemingly surged during the holidays, on top of already hefty debt loads,”Rossman said.

Now, delinquencies are at their highest level since 2012.

In 2012, we were just coming out of the Great Recession.

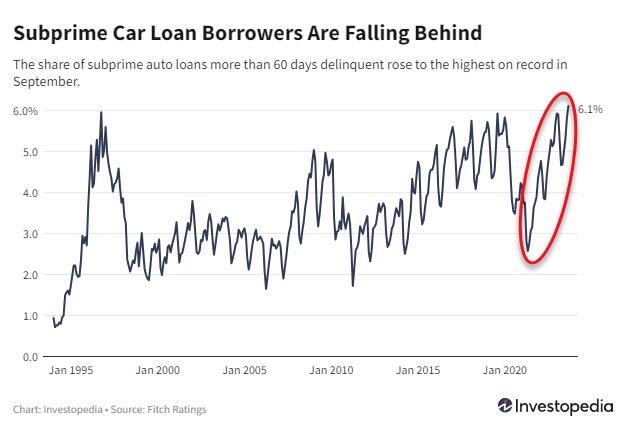

Creditnews has recently reported on a sharp rise in auto delinquencies, especially among subprime borrowers.

In September, the percentage of subprime borrowers who were at least 60 days behind on their car payments increased to 6.11% – the highest since at least 1994.

{kind=link}

Those were very painful days… but today we are being told by The White House that Bidenomics is awesome and we should all be more grateful and optimistic than the surveys suggest.

Presumably the ‘truth’ will be exposed in November.

Tyler Durden

Sat, 01/27/2024 – 11:05