Stocks’ Perpetual Motion Machine Can’t Run Forever

Authored by Simon White, Bloomberg macro strategist,

Perpetual motion machines shouldn’t exist. Yet the stock market seems to have found one.After initially striking turbulence when the Federal Reserve began hiking rates in 2022, equities have stabilized and are in a seemingly unshakable uptrend. Credit, volatility, option speculation and well-behaved inflation expectations are in a virtuous circle, keeping the market grinding higher.

Stocks are navigating the thin aperture of the Panama Canal.

Either a return to a low-and-stable inflation regime, or a re-acceleration in price growth — which unanchors inflation expectations and decimates the real value of stocks — would leave them in a precarious spot.

Their gains are thus built on a bed of sand, and are highly sensitive to any change in the inflation outlook.

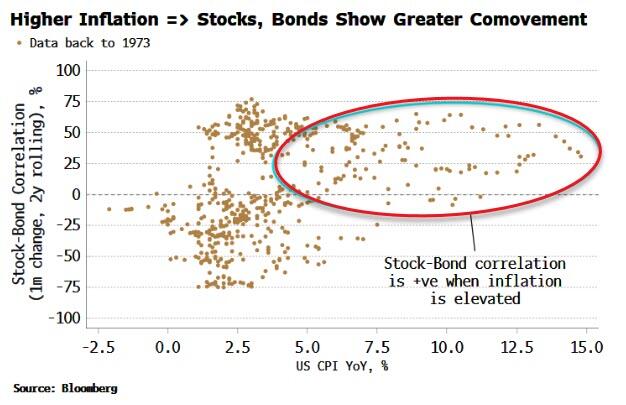

The stock-market’s perpetual motion machine has two engines, the first of which is the positive stock-bond correlation. Equities started moving in concert again after spending most of the last two decades moving oppositely to one another. Rising inflation is the main reason, with both assets moving increasingly together as CPI rises.

{kind=link}

Elevated price pressures mean shocks in growth and inflation are more likely to occur at the same time, i.e. stocks and bonds could fall together.

Not great if you own bonds as a hedge for your equity portfolio. But a positive stock-bond correlation, when neither growth nor inflation is in a bad way as with today, has the fortunate side-effect (if you are a long-only investor heedless of the underlying risks) of lower volatility leading to a cheaper cost of credit.

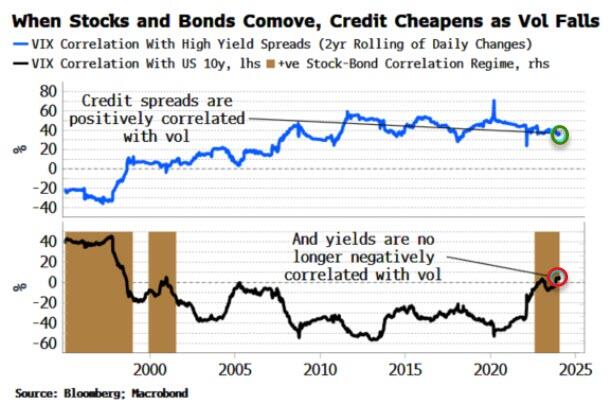

Why? The total cost of credit is made up of the credit spread and the yield on government bonds.Typically, as can be seen in the top panel of the chart below, credit spreads and the VIX are positively correlated, i.e. a lower VIX means cheaper credit.

But that effect is dulled when the stock-bond correlation is negative.

As the bottom panel in the chart shows, the VIX tends to be negatively correlated with 10-year yields when stocks and bonds move inversely. So even though credit spreads fall as the VIX falls, yields rise, meaning the total cost of credit may not drop by much, if at all.

{kind=link}

On the other hand, when the stock-bond correlation is positive, as today, the VIX becomes uncorrelated or positively correlated with the 10-year yield. A lower VIX therefore tends to have a bigger impact on reducing the cost of credit, which in turn makes the equities of companies in the aggregate more attractive. This ties with what we actually observe, with credit spreads and stock prices exhibiting a strong negative correlation.

In fact, the VIX is a direct input to credit-pricing models via the Merton distance-to-default model.

It might be an elegant solution to divining how likely firms are to default, but its inventor probably didn’t reckon with the speculative behavior seen today in stocks, repressing both implied and realized volatility and thus artificially making companies look less likely to go bankrupt.

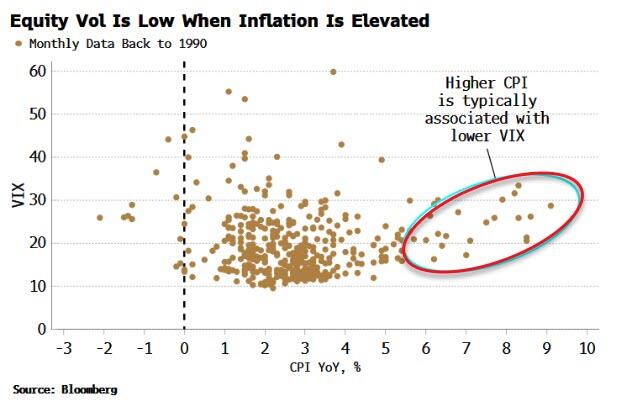

And this neatly brings us on to the second engine of the perpetual motion machine: a lower VIX.

That low volatility tends to accompany elevated inflation may seem paradoxical, but that is the case historically.

{kind=link}

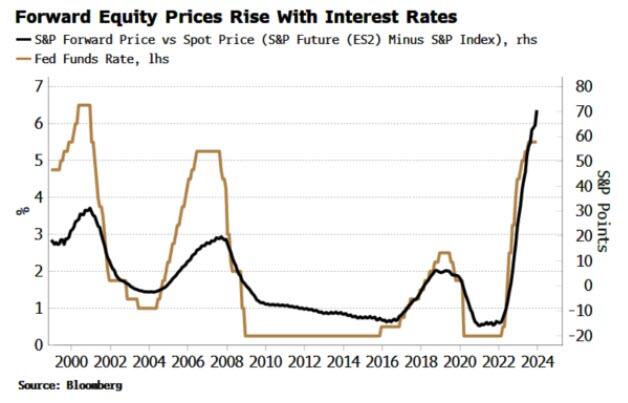

The explanation comes from forward prices (as we have touched upon in this column previously). Higher inflation elicits higher interest rates, which in turn causes the forward price of equity indexes to rise. (The cost of financing a forward rises when rates rise, and this is reflected in a higher forward price.)

{kind=link}

Equity options, including those that make up the VIX, are priced not off the spot price of the S&P but its forward price. This has the effect of increasing the price of call options and decreasing the price of puts.

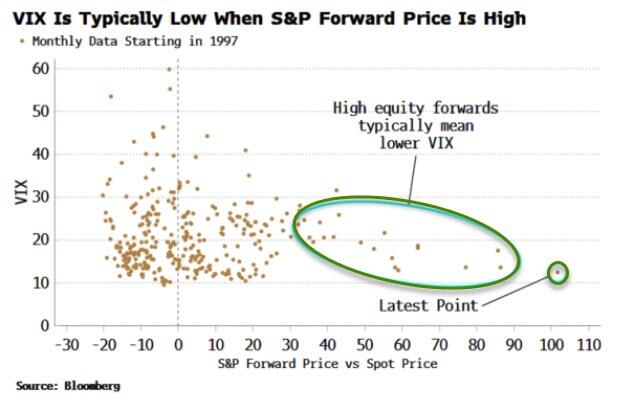

Put options typically cost more than calls (as downside insurance is more expensive), and they tend to be more out-of-the-money. Given the VIX is a weighted average of all puts and calls (with about 1-month expiry), higher forward rates are thus associated with a lower VIX. This is borne out by what we actually observe. As the chart below shows, we are now at the most extreme high forward price/low VIX in over 25 years.

{kind=link}

Falling implied volatility makes selling volatility more attractive — strategies like selling calls against long positions are very popular. But this has the effect of lowering realized volatility through the hedging behavior of the dealers who are long the call options (the dealers are long gamma).

This increasingly frenetic speculative behavior, charged by the explosion in 0DTE options, has the net impact of increasing the S&P’s risk-adjusted return, bolstering its attractiveness as an investment, and thus fueling its grind to yet higher levels.

In fact, high Sharpe ratios should be a warning, not an inducement, as repressed volatility has a tendency to explode higher, taking prices much lower with it, and decimating the risk-adjusted return.

Nevertheless, for now the game is in play.

And as we have seen it is one plank of a symbiotic relationship between inflation, credit and volatility driving the stock market higher in a seemingly never ending positive feedback loop.

But perpetual motion machines don’t exist, as they contravene the Second Law of Thermodynamics.

There are no equivalent iron-clad universal laws for stocks, and if something seems too good to be true, it generally isn’t.

Punters and investors alike should therefore continue to monitor inflation closely, because stocks won’t be able to thread the needle between the Great Moderation and the Great Inflation indefinitely.

Tyler Durden

Thu, 01/25/2024 – 09:10