Intel Tumbles After Guidance Misses Expectations Despite Strong Q4 Earnings

After several years of constant earnings disappointment culminating with the catastrophic earnings release for Q4 2022, which was clearly meant to be the company’s kitchen sink, it was only a matter before the company released results that would impress a market that had largely given up hope in the OG chipmaker (at least until it was trounced by Nvidia). This indeed happened both in Q2and Q3, which in turn sparked a powerful rally in the stock which had almost doubled in the past year amid hopes that Intel’s disappointing days were behind it.

Alas it was not meant to last, and moments ago the world’s largest market of computer processors (if certainly not by market cap) regressed to its old ways, reporting earnings which beat expectations yet guiding well below street estimates, which in turn has hammered the stock after hours as much as 10%.

Here is what the company reported for Q4:

EPS $0.63, beatingest. of $0.45

Revenue $15.41 billion, beatingest. $15.17 billion, and $300MM above the company’s October guidance

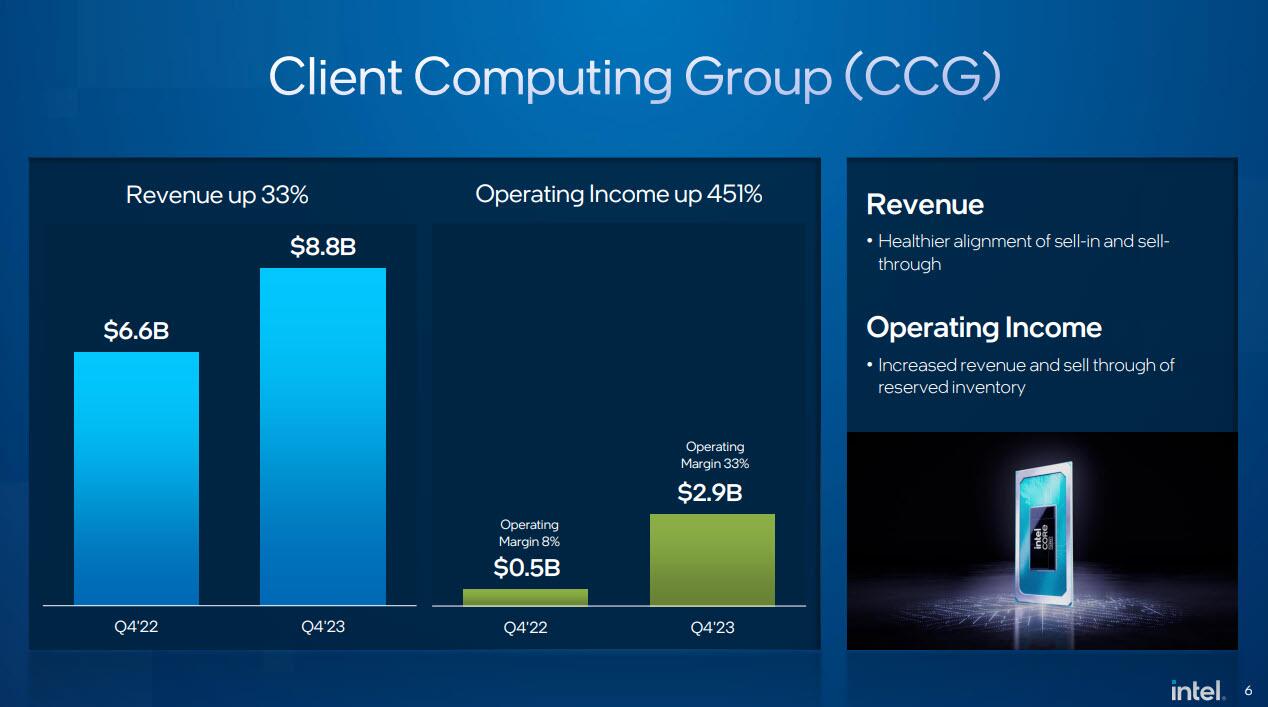

Client Computing revenue $8.84 billion, beatingest. $8.42 billion

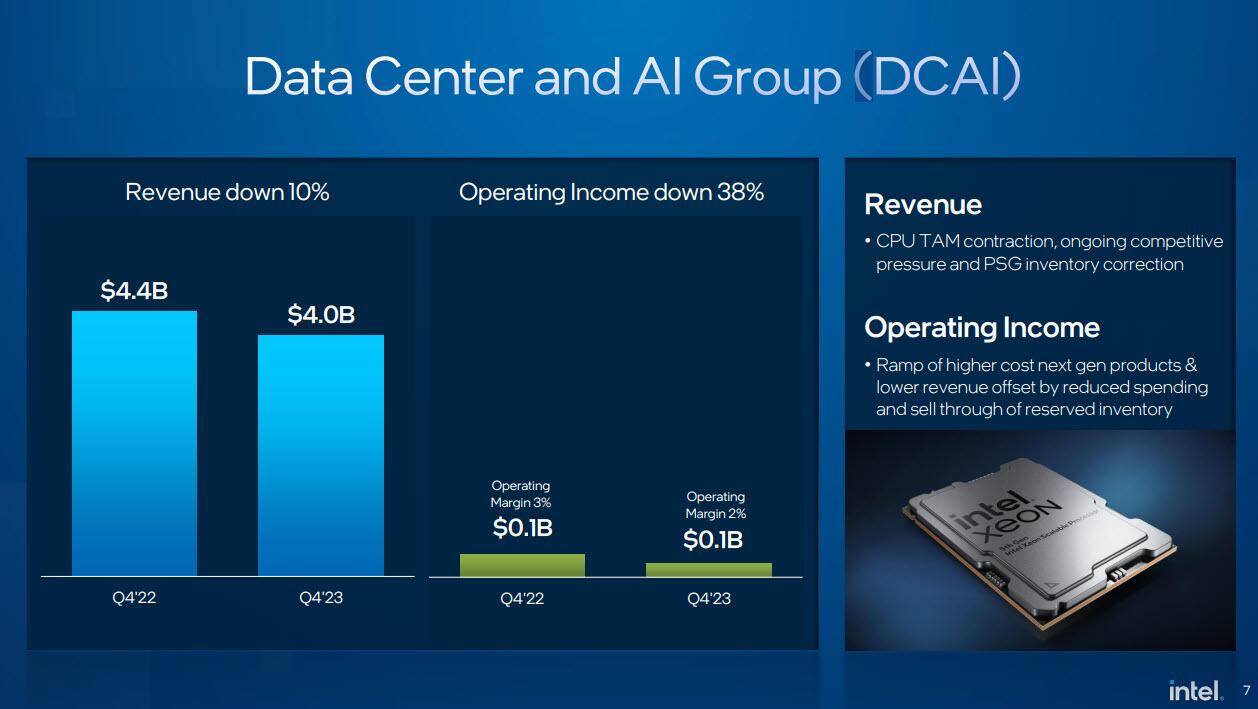

Datacenter & AI revenue $4.0 billion, missingest. $4.08 billion

Network & Edge revenue $1.47 billion, missingest. $1.55 billion

Mobileye revenue $637 million, beatingest. $627.2 million

Intel Foundry Services revenue $291 million, missingest. $342.5 million

Adjusted operating income $2.58 billion, beating est.$2.1 billion

Adjusted operating margin 16.7%, beatingestimates of 13.9%

Adjusted gross margin 48.8%, also beatingestimates of 46.5%

R&D expenses $3.99 billion, beatingthe est of $3.9 billion

Despite the (mostly) across the board beat, Intel still remains far from its heyday when it generated quarterly sales of more than $20 billion as recently as 2021.

{kind=link}

Client computing, Intel’s PC chip business, generated $8.8 billion in revenue last quarter. That compares with an estimate of $8.4 billion.

{kind=link}

Data-center sales were $4 billion, below the average projection of $4.08 billion.

{kind=link}

The company’s factory network, once the envy of the chip business, is crucial to whether Intel can regain its dominance. CEO Pat Gelsinger has promised that he will have the best production in the industry again by 2025 — and will even open those facilities up for rivals to use on a contract basis. In the meantime, the costly push to catch up with industry leader Taiwan Semi is weighing on profit.

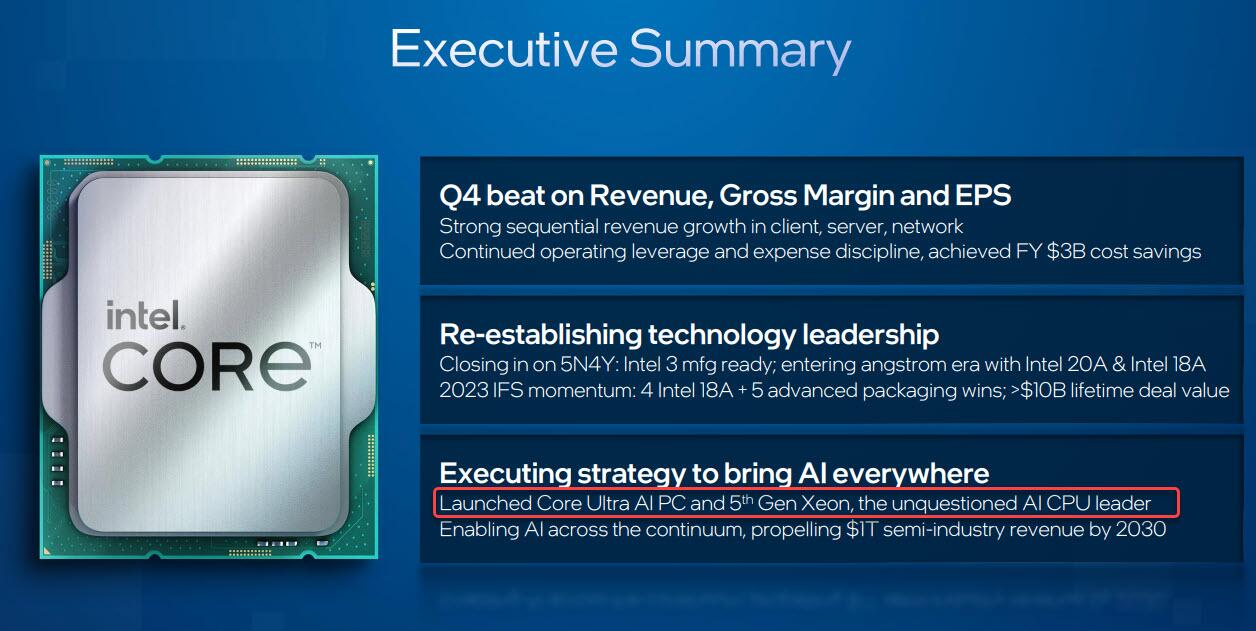

Commenting on the quarter, Intel said that it

Generated strong sequential revenue growth in client, server, network

Continued operating leverage and expense discipline, achieved FY $3B cost saving

Re-establishing technology leadership:

IS closing in on 5N4Y: Intel 3 mfg ready; entering angstrom era with Intel 20A & Intel 18A

2023 IFS momentum: 4 Intel 18A + 5 advanced packaging wins; >$10B lifetime deal value

And keeping up with peers, the company has realized that it hasto mention AI at every possible opportunity. And sure, enough, looking at the exec sum we didn’t have to scroll to low to find it:

{kind=link}

But the most notable part of the Q4 earnings report was the company’s outlook, where Intel now sees revenue between $12.2 and $13.2BN, badly missing consensus estimates of $14.25BN; it also expects gross margin of 44.5%, missing estimates of 45.5% and down from the current quarter’s 48%, and resulting in EPS of $0.12, also well below the consensus est. of $0.34, as the company once again slides into projection shambles, something the market hates.

The outlook suggests CEO Pat Gelsinger still has a long way to go in restoring Intel’s former prowess. Though the PC business is recovering, it continues to lose ground in the lucrative market for data center chips (where it is pushing ahead with a Xeon AI offering). The company also is contending with weaker demand at units that make programmable chips and components for self-driving vehicles, as well as a fledgling outsourced production effort.

In servers, where Intel once had a market share of more than 99%, the company is facing more competition and a shift in spending patterns. Longtime rival AMD has fielded increasingly powerful chips that are winning over customers. In another troubling sign for Intel, some of the world’s biggest spenders on the technology – including Amazon’s AWS and Microsoft – are designing their own processors.

Intel’s outlook also has been clouded by a division that it partially spun off. Earlier this month, Mobileye, a maker of autonomous driving technology, gave a full-year forecast that was well below analysts’ predictions. Intel is still the majority owner of the Israel company.

The company also said it was looking for ways to further tighten its belt. “We expect to unlock further efficiencies in 2024,” Chief Financial Officer David Zinsner said in the statement.

Furthermore, despite the stabilization in margins, they remain nowhere near the 60% level that it maintained for years, when it had dominant market share and productive factories. The company, one of the few in the industry that doesn’t outsource production, has been running its plants at less than full capacity. That’s helped reduce the amount of supply in a market where customers already have too much inventory.

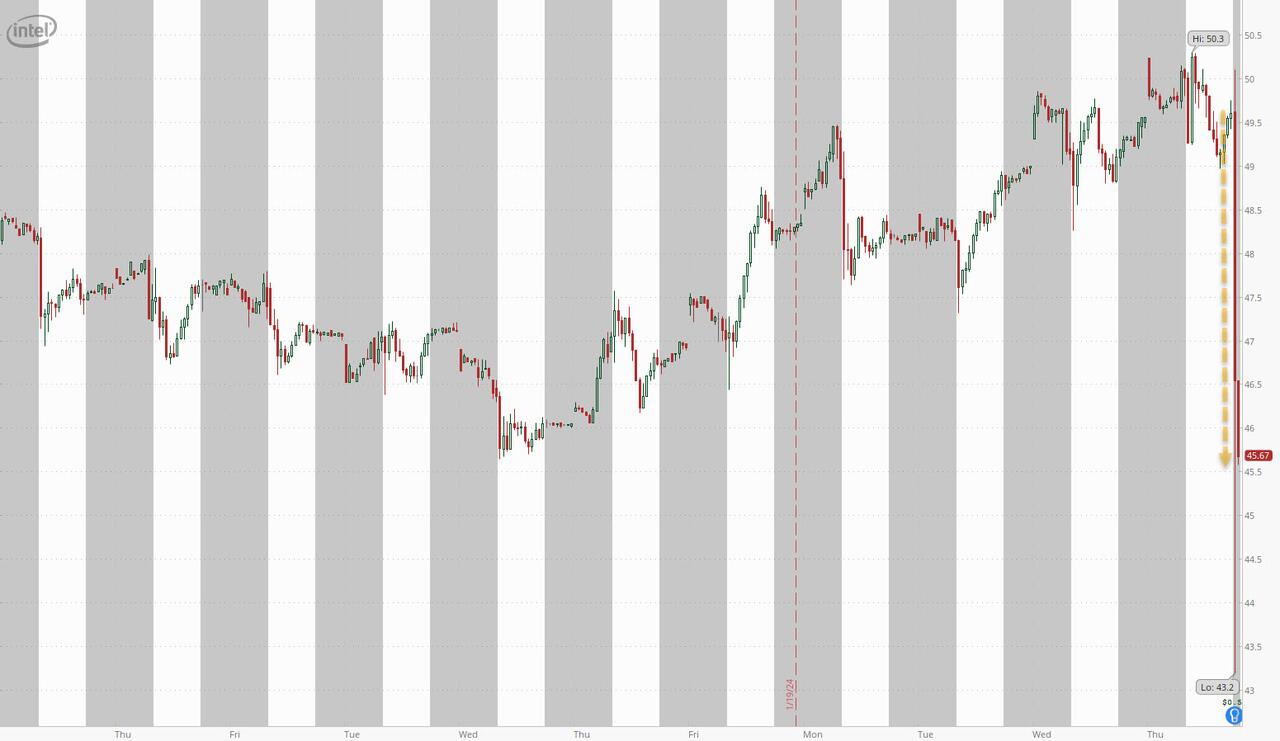

Q1 notwithstanding, the copmany remains in the early stages of a turnaround, which hinges on reestablishing Intel’s once-bulletproof lead in chip technology. And judging by the market reaction, after the furious recent rally pushed the stock as high as $50, doubt has once again started to creep in that INTC knows what it is doing as its stock tumbles over 8% after hours, which however is hardly catastrophic considering it traded there just one week ago.

{kind=link}

Tyler Durden

Thu, 01/25/2024 – 16:47