ECB Preview: Rates On Hold, Guidance Intact, But Brace For Collapse In April Rate Cut Odds

The ECB policy announcement is due this morning at 13:15GMT/08:15EST, and Lagarde’s press conference starts half an hour later, from 13:45GMT/08:45EST. Consensus and market pricing look for no changes to the ECB’s three key rates, while focus will be on the extent of pushback on current market pricing

Below is a more detailed preview of what to expect courtesy of Newsquawk

OVERVIEW:Expectations are for the ECB to stand pat on all three of its key rates. In terms of recent economic developments, headline EZ HICP rose to 2.9% in December (vs. prev. 2.4%) amid unfavourable energy base effects from Germany. Note, the uptick is set to be a temporary one and therefore the disinflationary process is still judged to remain in place. On the growth front, the prelim. Q4 EZ release is not due until 30th January. The EZ-wide composite PMI for January printed at 47.9 vs. Exp. 48.0 (prev. 47.6). Despite the slowing trend for inflation and subdued growth, January is seen as too soon for the ECB to commence its rate cutting cycle with policymakers attempting to dampen market expectations for an aggressive path of reductions. On which, President Lagarde has noted that too optimistic markets do not help the ECB in its inflation fight. Adding that, it is likely that the ECB will cut rates by the summer. Looking beyond the current meeting, the recent dovish repricing has seen markets assign a circa 76% chance of a cut in April with a total of 130bps of cuts seen by year-end vs. circa 160bps in the aftermath of the ECB’s December meeting.

PRIOR MEETING:As expected, the ECB opted to stand pat on rates for a second consecutive meeting with the main policy adjustment coming via the balance sheet. The Governing Council decided that reinvestments under PEPP will run at current levels during H1 (vs. previous guidance of “at least until the end of 2024), after which, it intends to reduce the PEPP portfolio by EUR 7.5bln per month on average. Elsewhere, the statement omitted the prior judgement that “inflation is still expected to stay too high for too long”. The accompanying macro projections saw 2023 inflation downgraded to 5.4% from 5.6%, 2024 cut to 2.7% from 3.2% and 2025 held at 1.9%. Note, the forecasts drew criticism in some quarters given the November 23rd cut-off date, which has prompted suggestions that the 2024 core inflation projection of 2.7% is too high given recent economic developments. On the growth front, 2023 and 2024 projections were cut with GDP this year seen at just 0.8% with the 2025 forecast held steady at 1.5%. At the follow-up press conference, when questioned on the Bank’s plans for rate cuts in 2024, Lagarde stated that the Governing Council did not discuss rate cuts at the meeting with policy set for a “plateau of hold”. Lagarde also noted that the Bank will need to see more evidence on wage growth given that current data shows that wages are “not declining”. When questioned on the balance sheet, the President noted that there were differing views on PEPP whereby some governors wanted different tapering, earlier or later.

RECENT ECONOMIC DEVELOPMENTS:In terms of recent economic developments, headline EZ HICP rose to 2.9% in December (vs. prev. 2.4%) amid unfavourable energy base effects from Germany. Note, the uptick is set to be a temporary one and therefore the disinflationary process is still judged to remain in place. Core inflation has continued to decline with December showing a downtick for the super-core metric to 3.4% from 3.6%. The ECB’s Consumer Inflation Expectations survey for November saw the 12-month print fall to 3.2% from 4.0% and the 3-year decline to 2.2% from 2.5%. In terms of market gauges, the 5y5y inflation forward has held steady around 2.25%. On the growth front, the prelim. Q4 EZ release is not due until 30th January. However, the FY 2023 GDP release from Germany noted a prelim 0.3% Q/Q contraction for the Eurozone’s largest economy. The EZ-wide composite PMI for January printed at 47.9 vs. Exp. 48.0 (prev. 47.6); services 48.4 vs. Exp. 49.0 (prev. 48.8), manufacturing 46.6 vs. Exp. 44.8 (prev. 44.4). Elsewhere, industrial production in the Eurozone shrank 0.3% on a M/M basis and 6.8% Y/Y. In the labour market, the EZ-wide unemployment rate sits at the historical low of 6.4%.

RECENT COMMUNICATIONS:President Lagarde has noted that too optimistic markets do not help the ECB in its inflation fight. Adding that, it is likely that the ECB will cut rates by the summer. Elsewhere, Chief Economist Lane has suggested the ECB will have key data by June to decide on rates and that changing rates too fast can be harmful. The influential Schnabel of Germany, observed that financial conditions have loosened more than projected. At the most hawkish end of the spectrum, Austria’s Holzmann has stated that markets should not count on rate cuts at all in 2024, adding that some early wage data point to quite high increases. These comments were followed up by an interjection from France’s Villeroy that most of the monetary transmission is more or less over, adding that the next move should be a cut in rates this year. Elsewhere, Latvia’s Simkus is of the view that the probability of a rate cut is to rise markedly after April, in any case, the first cut is likely with a “high probability” before the summer break. On the Red Sea disruptions, Cyprus’ Herodotou noted that geopolitical conflicts and possible supply chain disruption from the Red Sea makes rate cut discussion premature.

RATES/BALANCE SHEET: Expectations are for the ECB to stand pat on all three of its key rates after having held the deposit rate at its current peak of 4% since October. Despite the slowing trend for inflation and subdued growth, January is seen as too soon for the ECB to commence its rate cutting cycle with policymakers attempting to dampen market expectations for an aggressive path of reductions. Looking beyond the current meeting, the recent dovish repricing has seen markets assign a circa 76% chance of a cut in April with a total of 130bps of cuts seen by year-end vs. circa 160bps in the aftermath of the ECB’s December meeting. Surveyed economists are slightly more hawkish-leaning with the median looking for a rate cut in June and a total of 100bps of cuts this year. No changes on the balance sheet are expected given the adjustment at the prior meeting which saw the bank decide that reinvestments under PEPP will run at current levels during H1 (vs. previous guidance of “at least until the end of 2024), after which, it intends to reduce the PEPP portfolio by EUR 7.5bln per month on average.

* * *

Finally, some observations from Bloomberg’s Ven Ram, who notes that since the start of the year, we have seen bets for a rate cut as early as March in the euro zone (and US) evaporate, and that after today’s European Central Bank policy review, the markets may similarly reduce the odds being priced for an April reduction.

Indeed, while interest-rate traders are pricing almost a 65% chance of a move in early spring, after the resilient PMI prints from the euro zone on Wednesday, the ECB has little incentive to bring forward its time line guidance.

Philip Lane, the ECB’s chief economist, said earlier this month the key Eurostat national accounts data for the first quarter that will guide the governing council, would be available only in time for the June review. President Christine Lagarde later commented that there would likely be majority support for a cut in the summer.

While the disinflationary momentum in the region has been remarkable over the past year, a record-low jobless rate has stoked wage inflation past 5%, the highest in recent memory — sparking concern over how sticky inflation will prove to be around current levels.

Of key interest will be what the ECB does with this part of the statement from December:

“Based on its current assessment, the Governing Council considers that the key ECB interest rates are at levels that, maintained for a sufficiently long duration, will make a substantial contribution to this goal. The Governing Council’s future decisions will ensure that its policy rates will be set at sufficiently restrictive levels for as long as necessary.”

Given President Lagarde’s recent comments, the ECB may prefer to leave that guidance unchanged for fear of confusing the markets. A change of language may come as late as the April meeting ahead of a possible cut in June.

We also get a policy review from Norway’s central bank today and it’s unlikely we will get a surprise hike given that inflation since the last meeting showed a moderation. Of keen interest to traders will be guidance on a possible rate cut, with Norges Bank indicating earlier that a reduction may come after the autumn.

* * *

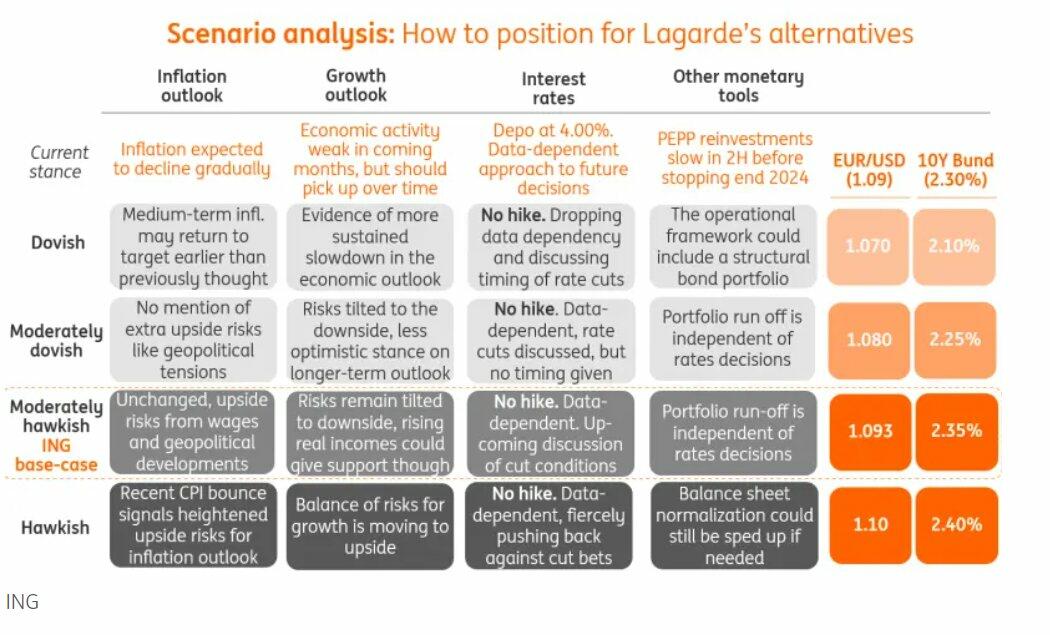

Finally, those looking for a market matrix, here is ING with its familiar ECB cheat sheet:

{kind=link}

Tyler Durden

Thu, 01/25/2024 – 07:41