Bonds & Black Gold Bid, Big-Tech Skids As ‘No Landing’ Narrative Gores Goldilocks

StrongGDP growth (but cool inflation), strongnew home sales (but cool home prices), stronglabor market data (jobless claim rose but remain near multi-decade lows) all set the tone for the day as traders ignored weakNational Activity data from The Chicago Fed, weakmanufacturing data from The Kansas City Fed, and weak headline durable goods orders.

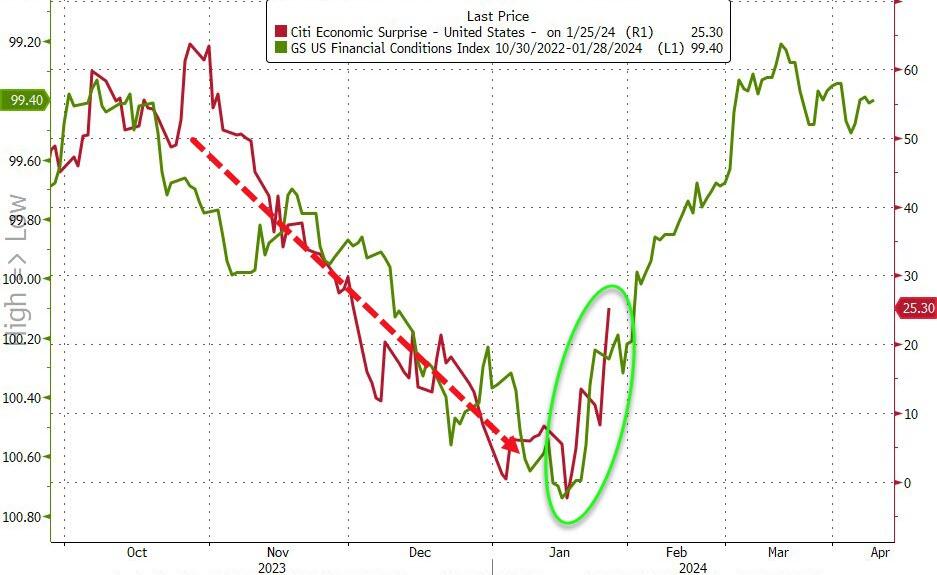

But, the macro surprise index is accelerating right when it is expected to as the lagged impact of the massive easing of financial conditions floods into the economy…

{kind=link}

Source: Bloomberg

Additionally, a massive $81BN of liquidity was pulled out of The Fed’s Reverse Repo facility today (after the surge in bill issuance), making a total of $460BN withdrawn from the facility in January so far– on track for by far the biggest monthly decline ever.

{kind=link}

Source: Bloomberg

Interestingly, amid all that, STIRs shifted dovishly – with the odds of a March cut rising modestly and the size of 2024 cuts rising (perhaps ahead of tomorrow’s pivotal Core PCE print)…

{kind=link}

Source: Bloomberg

Treasuries were bid across the entire curve with the short-end outperforming on the day (3Y -7bps, 30Y -3bps), leaving just the long-end still higher in yield on the week…

{kind=link}

Source: Bloomberg

The yield curve bull-steepened today, with 2s30s jumping to +7bps – its ‘steepest/uninverted’ since July 2022…

{kind=link}

Source: Bloomberg

Nasdaq lagged on the day – thanks in large part to TSLA – as Small Caps outperformed. Everything closed green (even Nasdaq)… with a late-day meltup ahead of Core PCE…

{kind=link}

This is the 5th record daily close in a row for the S&P 500

TSLA’s tumbled over 12% for its worst day since 2020 to its lowest since May 2023…

{kind=link}

TSLA weighed down The Magnificent 7 today, erasing most of yesterday’s meetings…

{kind=link}

Vol is extremely low ahead of tomorrow’s Core PCE print (and next week’s NFP), but the term structure does recognize it…

{kind=link}

Source: Bloomberg

The dollar rallied during the US session, recovering from overnight selling pressure…

{kind=link}

Source: Bloomberg

Bitcoin went sideways again today hovering around $40,000…

{kind=link}

Source: Bloomberg

…as GBTC outflows shrank again…

{kind=link}

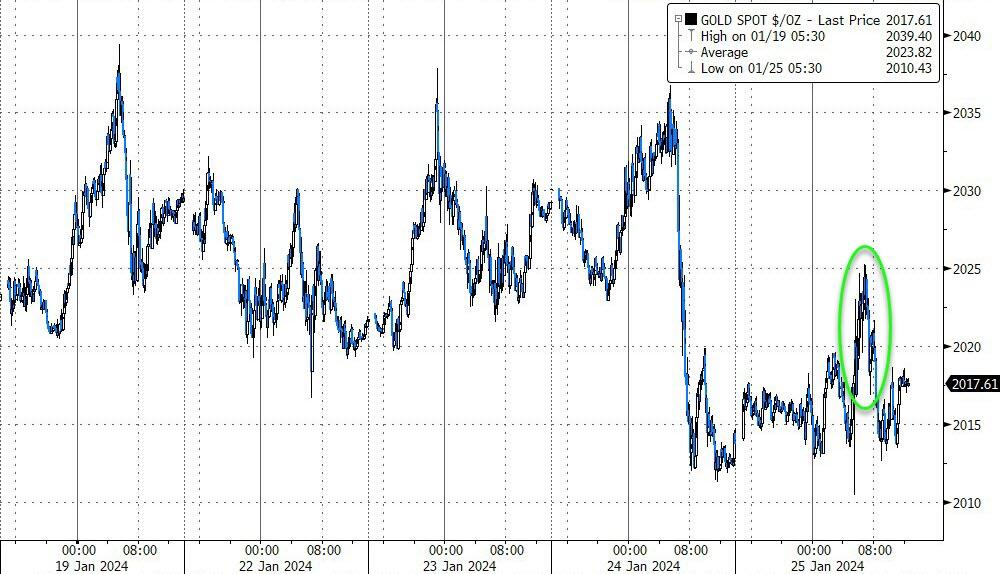

Gold went sideways today, testing up to $2025 intraday before fading back…

{kind=link}

Source: Bloomberg

Oil prices well and truly broke out of their recent rangebound trading bracket with WTI ripping up to almost $78 – its highest since 11/30 (when OPEC+ failed to impress with its announcement of additional – voluntary – production cuts…

{kind=link}

Source: Bloomberg

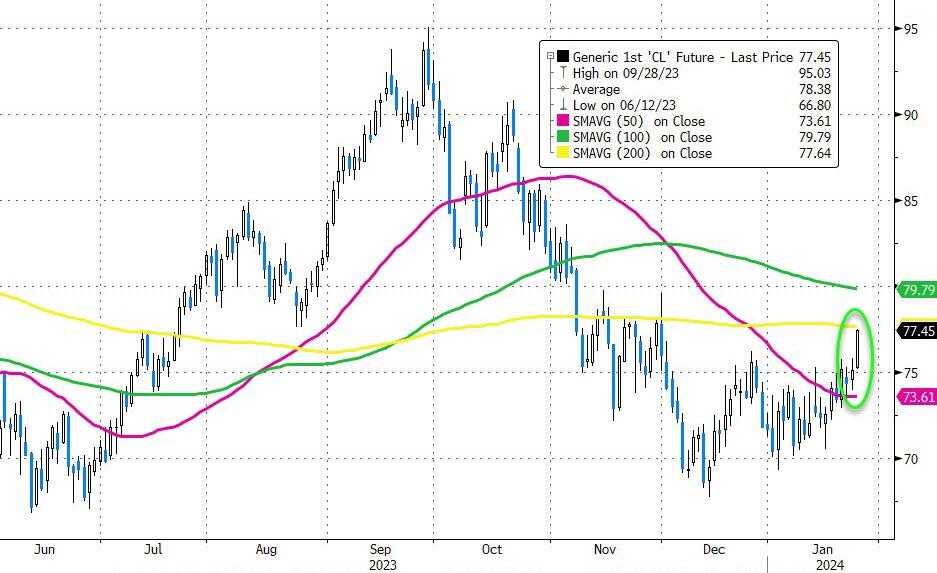

WTI tested all the way up to its 200DMA today…

{kind=link}

Source: Bloomberg

Finally, as Goldman’s Lee Coppersmith noted today, the dichotomy between the first half of February and the second half from a seasonal perspective is dramatic to say the least…

{kind=link}

For those worried about any froth in the US markets, the last two weeks in February are historically the worst 2 weeks of the year.

Given how well markets followed the historical analog last year, it’s something to have on the radar.

Tyler Durden

Thu, 01/25/2024 – 16:00