Bank Bailout Fund ‘Arb’ Usage Soars (Again) Amid Money-Market Fund Outflows, Large RRP Drain

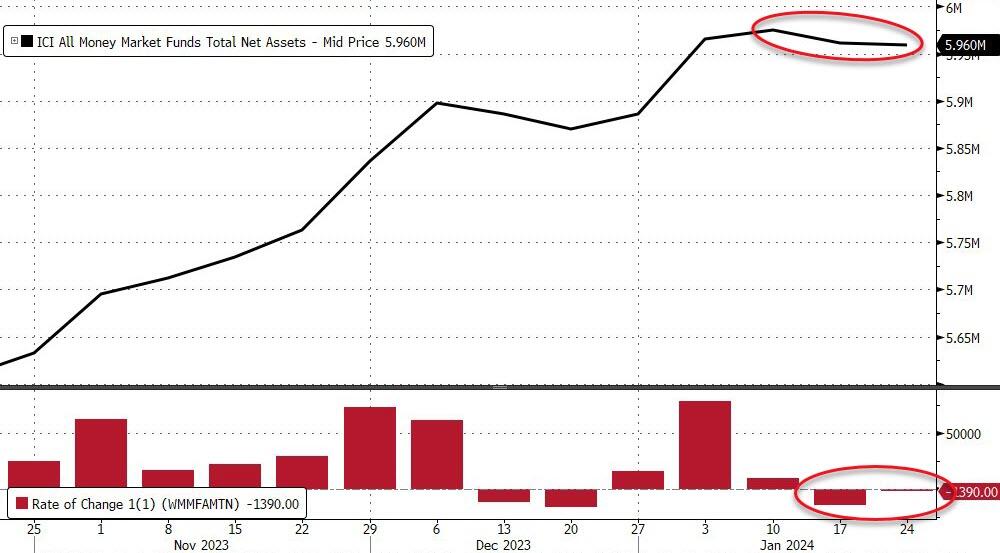

Money-market fund assets fell for a second week in a row, led by the departure of assets from institutional funds, as investors continued to reallocate portfolios in the new year.

Outflows were only a very modest $1.38BN last week, but still an outflow (on top of the prior week’s $14

{kind=link}

Source: Bloomberg

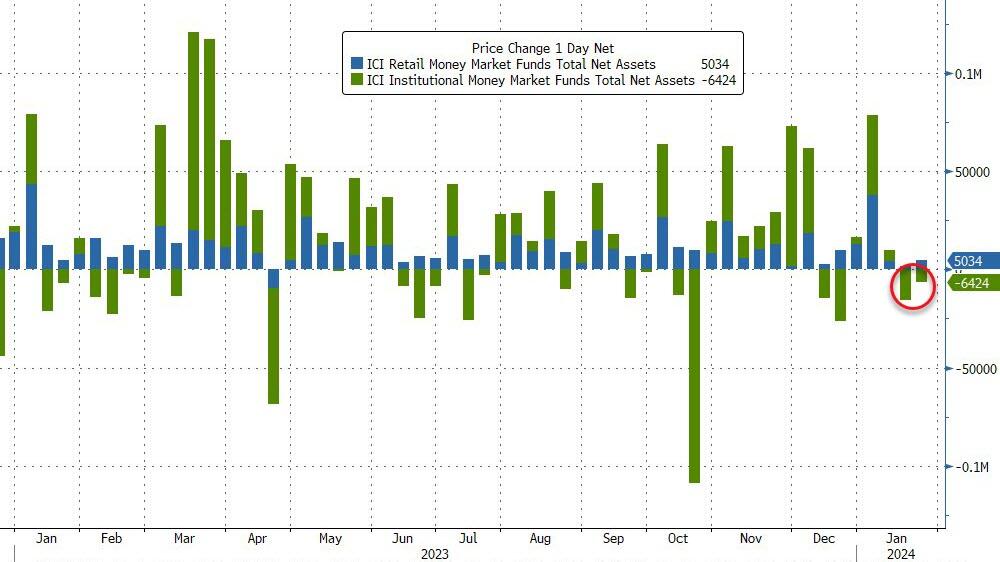

Retail funds continued to see inflows (again) of $5.0BN while institutional funds saw a $6.4BN outflow…

{kind=link}

Source: Bloomberg

In a breakdown for the week to Jan. 24, government funds – which invest primarily in securities like Treasury bills, repurchase agreements and agency debt – saw assets fall to $4.857 trillion, a $5.03 billion decline.

Prime funds, which tend to invest in higher-risk assets such as commercial paper, meanwhile, saw assets rise to $986.38 billion, an $8.10 billion increase.

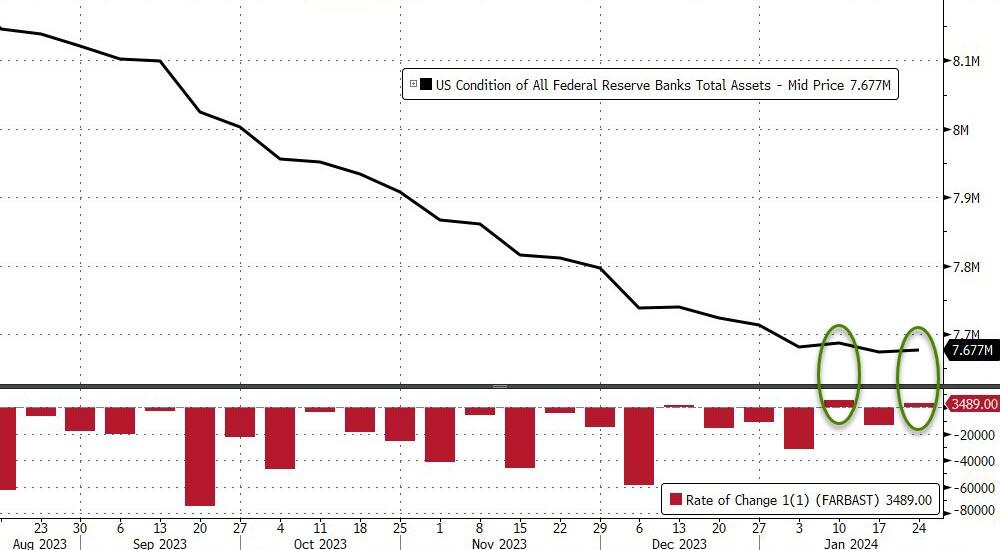

For the second week in the last three, The Fed’s balance sheet expanded last week (+$3.5BN)…

{kind=link}

Source: Bloomberg

Bank reserves at The Fed declined last week but that didn’t stop stocks from reaching new cycle highs in market cap…

{kind=link}

Source: Bloomberg

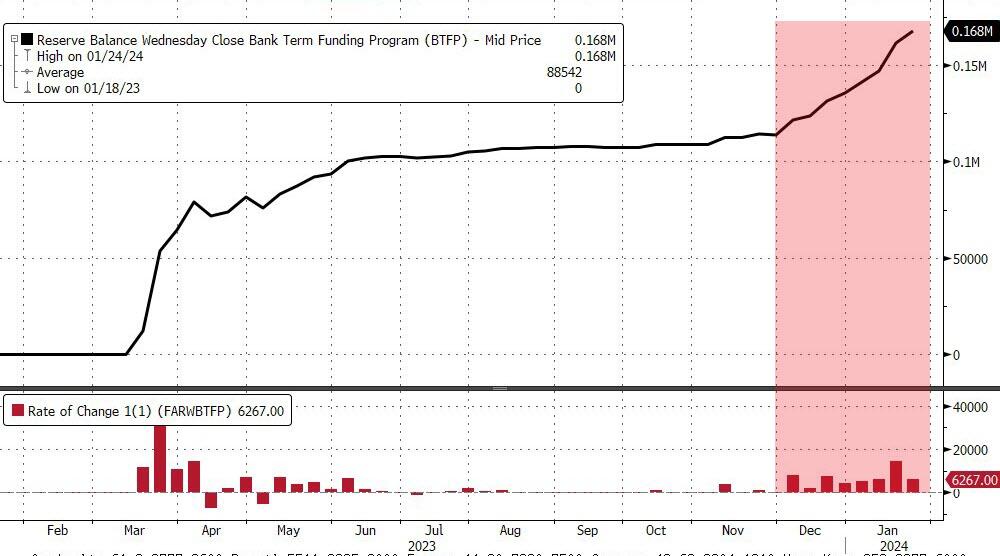

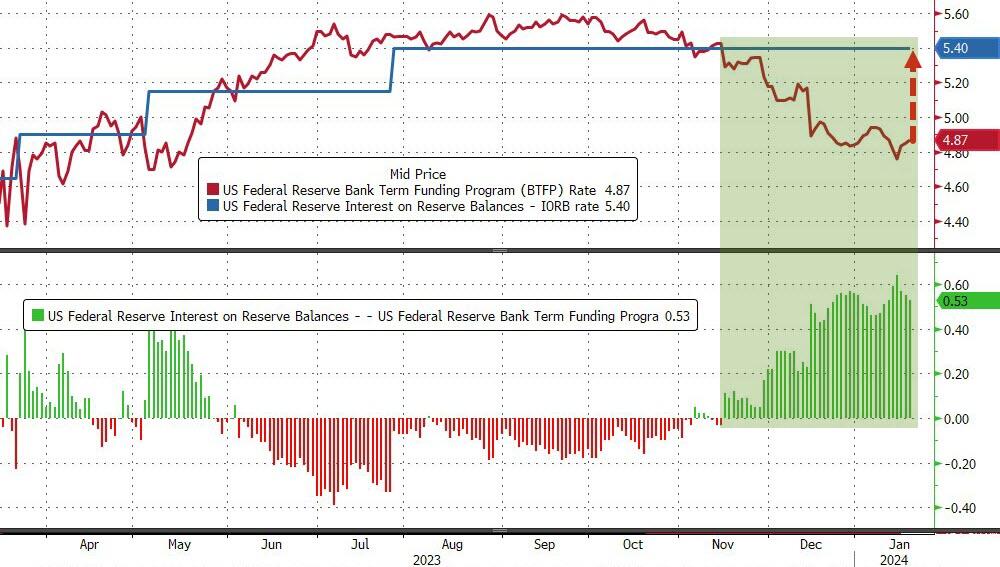

Usage of The Fed’s Bank bailout facility increased by another $6.3BN last week, that makes over $54BN since the BTFP Arb started in early December.

{kind=link}

But that is it for the ‘arb’ flows – from here, any increase in usage is pure banking system stress.

But, as we noted last night, with just two months until the March threat looming, the Fed has changed the terms on the BTFP to kill the free-money arb.

“…the interest rate applicable to new BTFP loans has been adjusted such that the rate on new loans extended from now through program expiration will be no lower than the interest rate on reserve balances in effect on the day the loan is made.

This rate adjustment ensures that the BTFP continues to support the goals of the program in the current interest rate environment. This change is effective immediately. All other terms of the program are unchanged.”

{kind=link}

Additionally, The Fed made clear that the entire BTFP program is being scrapped on March 11, just as we said it will be as one of our preconditions for a very exciting March:

March will be lit:

1. Reverse repo ends

2. BTFP expires

3. Fed cuts (allegedly)

4. QT ends (allegedly)

— zerohedge (@zerohedge) January 8, 2024

This is what the Fed said: “The Federal Reserve Board on Wednesday announced that the Bank Term Funding Program (BTFP) will cease making new loans as scheduled on March 11. The program will continue to make loans until that time and is available as an additional source of liquidity for eligible institutions.”

And just as we predicted a few days ago when reporting on the Fed’s sudden infatuation with the discount window…

*US PLANS TO PUSH MORE BANKS TO USE THE FED’S DISCOUNT WINDOW

translation: many more banks will HAVE to use the discount window… right after the BTFP expires

— zerohedge (@zerohedge) January 18, 2024

… the Fed is now saying that all liquidity needs going forward will be met by the discount window (the same one that precipitated the global financial crisis back in 2008).

During a period of stress last spring, the Bank Term Funding Program helped assure the stability of the banking system and provide support for the economy. After March 11, banks and other depository institutions will continue to have ready access to the discount window to meet liquidity needs.

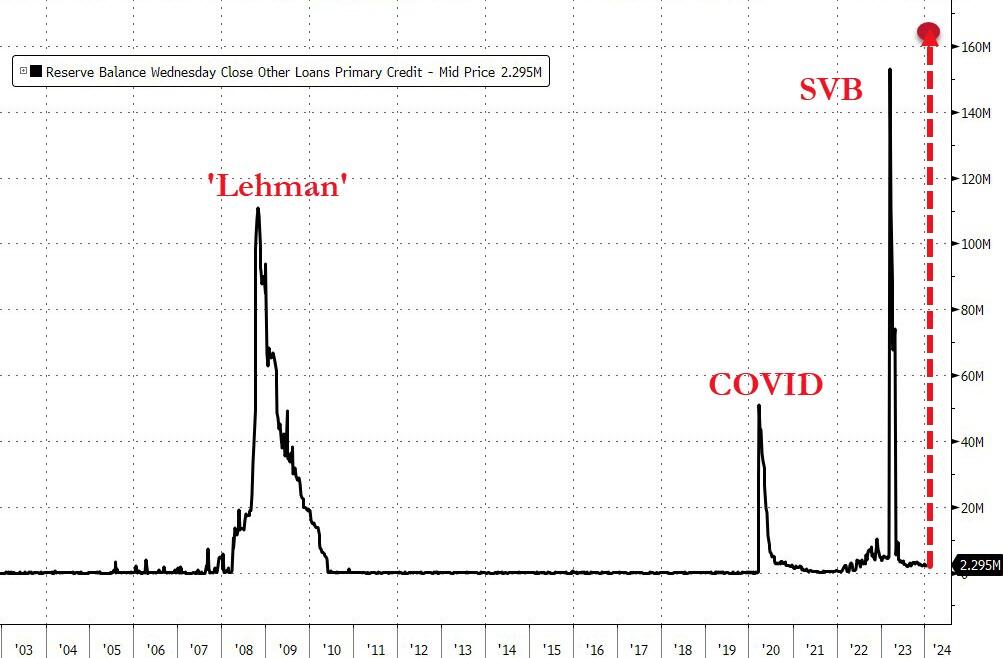

Can the discount window cope with the sudden need for over $147 Billion?

Last week saw usage of the discount window rise $189 Million to $2.295 Billion…

What do you think?

{kind=link}

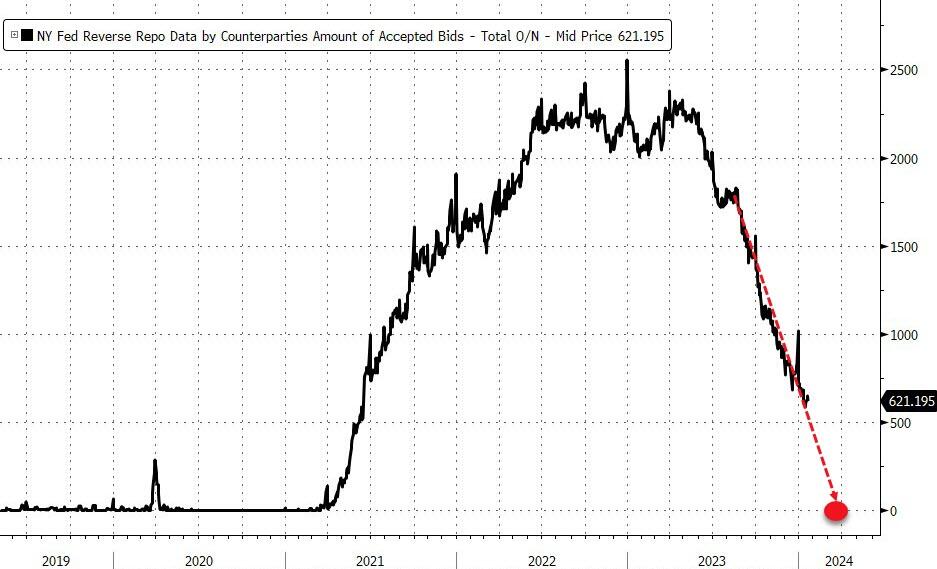

And that March expiration of the facility lines up with another potential crisis moment for the banking system – The Fed’s Reverse Repo facility being drawn down to zero (down a whopping $81BN today alone) – at which point reserves get yanked which means huge deposit flight, and a restart of the banking crisis, more liquidity injections, rate cuts, end of QT and so on.

{kind=link}

We leave with one question – who could have seen this coming?

1.❓

2.✅

3.❓

4.❓ https://t.co/4AlC0HRqSZ

— zerohedge (@zerohedge) January 25, 2024

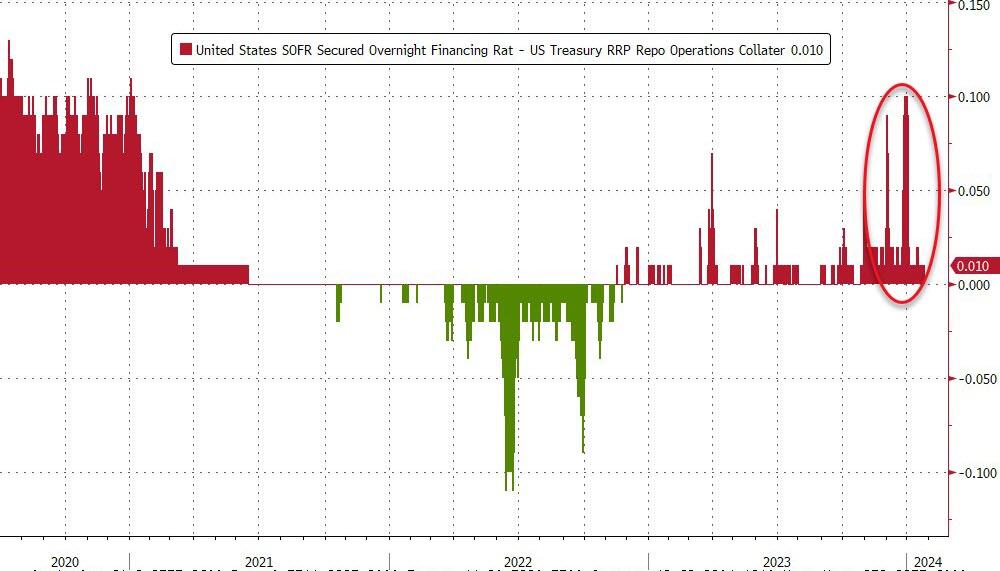

Watch the SOFR-O/N RRP Spread for signs of stress…

{kind=link}

Key things to keep an eye on are re-increases in the RRP, indicating extra reserves are being taken back out of the system, or a rising take-up in the Fed’s standing repo facility, which would point to potential funding problems. All said and done, don’t put your spanner away yet, knowing how to plumb remains an essential skill.

Tyler Durden

Thu, 01/25/2024 – 16:41