US PMIs Unexpectedly Soar In January Amid Manufacturing ‘Renaissance’, But…

It’s PMI day!!

Australia PMI improved on the back of expansion in manufacturing;

Japan Composite PMI improved into expansion overnight;

India soared with both services and manufacturing surging;

Europe disappointed with Germany and France weaker;

UK improved again;

US PMIs spiked with major jump in manufacturing (BUT…)

* * *

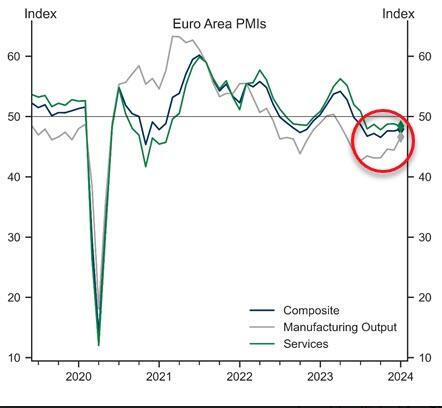

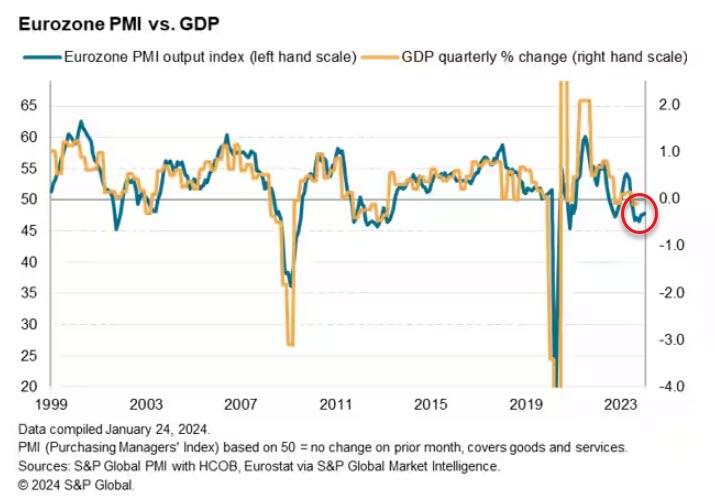

The Euro area composite flash PMI increased by 0.3pt to 47.9, in line with our expectations but below consensus.

{kind=link}

The improvement in the composite index was led by the manufacturing sector, where the manufacturing output index grew (by 2.2pt) to 46.6, partially offset by a deterioration in services activity, where the index fell (by 0.4pt) to 48.4.

Not a good sign for EU GDP…

{kind=link}

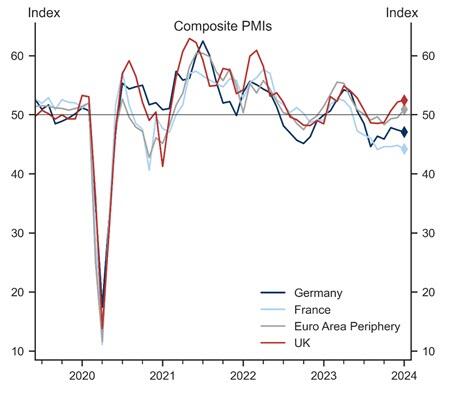

The national breakdown revealed weakness in the monetary union’s two largest economies (while the periphery improved, back into expansion).

France: The French composite flash PMI decreased by 0.6pt to 44.2 in January, below consensus. The decline was driven by both sectors, though skewed towards the services sector, where the index fell (by 0.6pt) to 45.0.

Germany: The German composite flash PMI decreased by 0.3pt to 47.1 in January, below consensus. The deceleration was driven by the services sector, where the index fell (by 1.6pt) to 47.6, partly offset by a significant improvement in manufacturing output, which grew (by 2.3pt) to 46.0.

Periphery: The periphery composite PMI increased by 1.4pt and entered expansionary territory at 50.9, driven by the manufacturing sector, where the manufacturing output index recorded a significant improvement (of 2.8pt) to 49.0.

The UK composite flash PMI improved again, by 0.3pt, to 52.5, slightly above expectations, on the back of a continued improvement in services activity, with the services index printing at 53.8 (up by 0.4pt), partially offset by a deceleration in the manufacturing sector, where the output index fell further (by 0.5pt) to 44.9.

{kind=link}

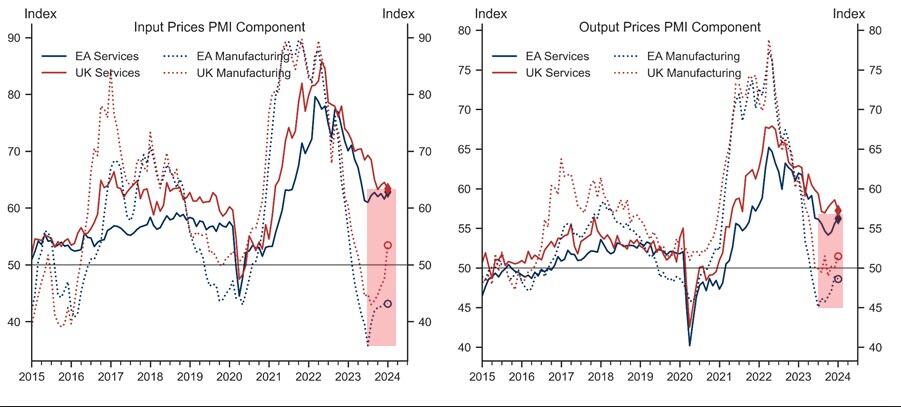

There is a problem though, as the Red Sea disruptions seem to be feeding through to the lengthening in delivery times and input cost inflation in the Euro area, but more so in the UK, and weigh on overall sentiment, as some survey respondents mention concerns over “global geopolitical risks”.

“Average prices charged for goods and services also rose at the steepest rate since last May. Having fallen to a 32-month low last October, the rate of selling price inflation has now ticked higher for three successive months to therefore remain elevated by the historical standards of the survey,” according to the press release published by S&P Global.

{kind=link}

So to summarize the state of play in Europe – the EU data is screaming stagflation as economic growth continues to weaken and prices resurge (while UK is seeing growth accelerate along with prices).

The US flash PMI data soaredwith manufacturing back above 50 (50.3 – the highest in 15 months) and Services rising to 52.9 (7-month highs), tracking higher with stronger ‘hard’ data in January…

US Manufacturing was expected to decline from 47.9 to 47.6 but instead it ripped up to 50.3

US Services was expected to be basiclaly flat at 50.9 but instead it jumped to 52.3.

{kind=link}

“An encouraging start to the year is indicated for the US economy by the flash PMI data, with companies reporting a marked acceleration of growth alongside a sharp cooling of inflation pressures.

“Output measured across both goods and services rose in January at the fastest rate since last June, growth momentum having stepped up a gear on the back of improved demand conditions. New orders inflows have now picked up for three months, buoyed in particular by improving sales to domestic customers, helping lift business confidence about the year ahead to the most optimistic since May 2022.

“Confidence has also been buoyed by hopes of lower inflation in 2024, easing the cost of living squeeze and facilitating the path to lower interest rates. With prices rising in January at the slowest rate since the initial pandemic lockdowns of early 2020,companies report that selling price inflation is now below the pre-pandemic average and consistent with consumer price inflation dropping below the Fed’s 2% target.

“With the survey indicating that supply delays have intensified while labor markets remain tight, cost pressures will need to be monitored closely in the coming months, but for now the survey send a clear and welcome message of resilient economic growth and sharply waning inflation.”

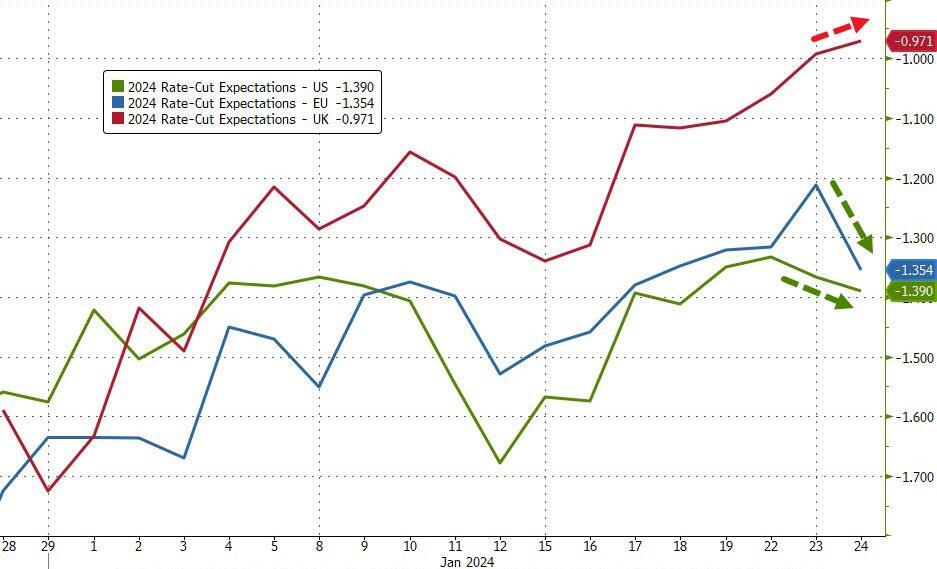

The result of all that is UK rate-cut expectations for 2024 has declined (hawkishly) to less than 100bps while US and EU rate-cut expectations are drifting higher (dovishly) with The ECB converging with The Fed.

{kind=link}

But… and it’s a big but…

Don’t get too excited about the super-hot US PMIs.

They did it again – Lead times lengthened for the first time in over a year and to the greatest extent since October 2022.

S&P Global interprets that a positive in their model – longer lead times must mean demand overwhelming supply, hence ‘good’ news.

{kind=link}

But in this case – just as we saw during the COVID lockdowns – the longer lead times are supply-chain bottleneck issues (Red Sea and US storms)– and not at all a positive.

“…firms noted broadly sufficient availability of materials at suppliers, challenging trucking conditions due to storms and transportation delays reportedly weighed on vendor performance

Purchasing activity at manufacturers continued to contract, with firms also depleting pre-production inventories further, but both rates of decline eased on the month.

Stocks of finished goods saw a renewed expansion, indicating the fastest rise in post-production inventories since November 2022.“

Does that sound like the message of an “expanding” manufacturing sector?

Tyler Durden

Wed, 01/24/2024 – 10:00