China “Unexpectedly” Cuts Required Reserve Ratio In Desperate Bid To Contain Market Collapse

In a move many said was very long overdue, this morning China which has paradoxically waited too long until deflation reigns across the country, said it will cut the required reserve ratio (RRR) by 50bps within two weeks and hinted at more support measures to come, which while coming largely in time with the easing ahead of the lunar new year was an unusually early disclosure that shows mounting urgency across President Xi Jinping’s government to shore up the economy and halt a $6 trillion stock-market rout. The cut was announced unexpectedly by People’s Bank of China Governor Pan Gongsheng during a press conference on Wednesdayin Beijing and sends a new signal that officials are eager to curb the stock-market selloff, while also stepping up support for the broader economy.

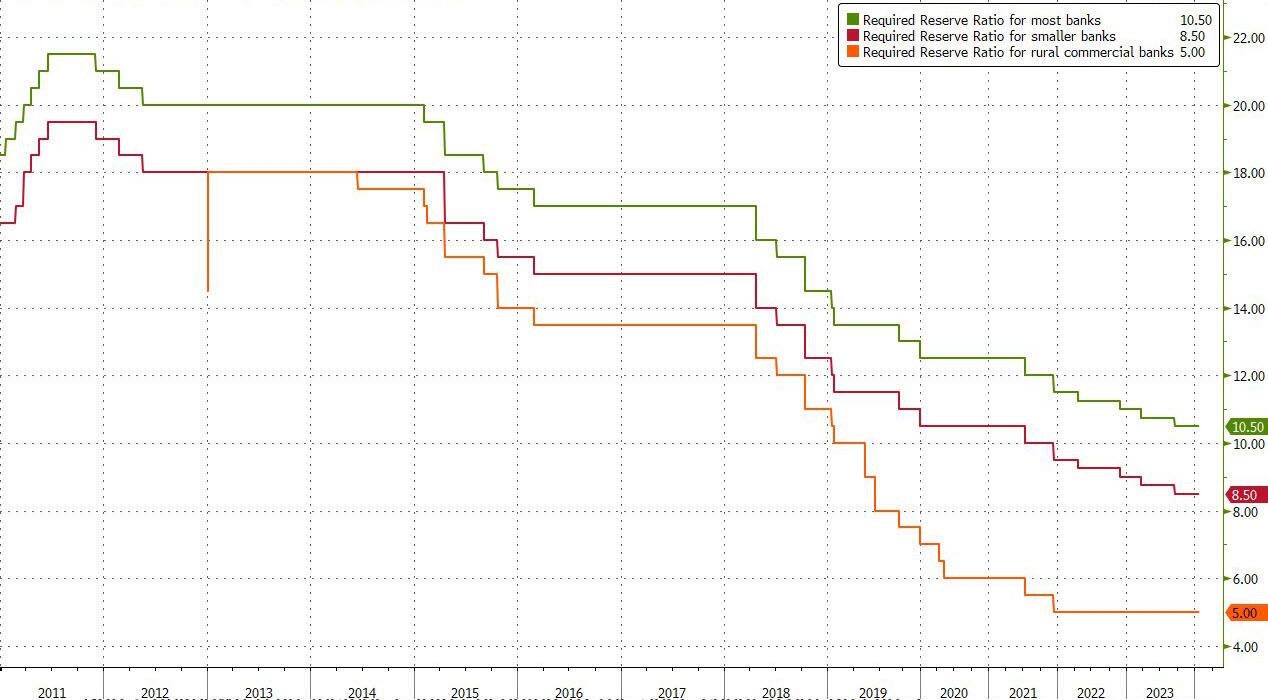

The RRR, which determines the amount of cash banks have to keep in reserve, will be lowered by 0.5% on Feb. 5 to provide 1 trillion yuan ($139 billion) in long-term liquidity to the market, the People’s Bank of China’s Governor Pan Gongsheng told reporters at a briefing.

{kind=link}

The cut comes on the heels of signs of gathering government support for China’s swooning stock market, with investors detecting a rash of share buying by pension funds, insurers and other state-linked firms, and follows a Bloomberg report that Beijing is also “mulling” a 2 trillion market rescue package.

As Bloomberg notes, it was a “rare and transparent reveal of a policy change by the head of the PBOC.” Typically the central bank announces it on its website first, with the State Council — China’s cabinet — sometimes hinting at one beforehand. But troubling economic data and the massive rout in stocks have prompted authorities to step up rhetoric this week. Pan’s remarks add to a flurry of promises from other agencies following a call by Premier Li Qiang to stabilize the market.

“Announcing an RRR cut in advance suggests there’s no other effective tools available to stem the market rout,” said Shen Meng, managing director at Beijing-based Chanson & Co.

While many economists had been expecting a RRR cut at some point this quarter, it’s not clear how much this will move the needle. Several analysts see the latest move as a way to smooth liquidity ahead of the Lunar New Year holiday next month, though any broader impact on the economy may be limited.

“An RRR cut helps sentiment in the sense that the action seems more decisive,” said Kevin Net, head of Asian equities at Tocqueville Finance SA. “But some investors may use this as an exit opportunity if there is such short-term market rebound — unless there are more policies to address structural issues, like those with the property market.”

Todd Schubert, senior fixed-income strategist at Bank of Singapore, echoed the sentiment, saying that the planned reduction in China’s reserve requirement ratio is a welcome step and investors are hopeful that it will be followed by further aggressive policy moves to bolster the economy. For bond investors, it is “not necessarily a game changer, and perhaps even a bit overdue but a welcome step in the right direction,” he said adding that “China has been suffering from a lack of demand stemming from diminished consumer confidence. The RRR cut should help improve domestic faith that the Chinese government is taking the necessary proactive steps to bolster the economy and stem recent market weakness and volatility.”

Others were even more pessimistic: Lin Jing Leong, a senior sovereign rate and currency strategist at Columbia Threadneedle Investments, said that the impact of China’s plan to cut the reserve requirement ratio on financial markets is negligible and investors shouldn’t get too excited.

“This is very much expected given it is primarily for liquidity injection for the Chinese New Year, which tends to see system liquidity tighten as large scale cash withdrawals are made.”

To be sure, the market’s kneejerk reaction was favorable and the Hang Seng China Enterprises Index extended gains following Pan’s remarks, capping its biggest two-day advance since November 2022. The yield on China’s 10-year government bonds slipped slightly before rebounding to 2.51%. The offshore yuan erased earlier losses amid state-bank sales of the US dollar.

Most of the other announcements this week have been fairly vague. The state-owned enterprise watchdog vowed to improve the quality of listed SOEs, while the securities regulator said it would “make every effort” to maintain the stable operation of capital markets and to calm investor nerves. Bloomberg News reported that authorities are mulling a $278 billion rescue package using offshore money as part of a stabilization fund. The plan hasn’t been finalized.

Along with the reserve ratio, Pan also said the central bank would from Thursday lower interest rates on relending funds provided to banks that incentivize loans to the agricultural sector and small firms. He added that the PBOC will unveil an adjustment to borrowing policies related to commercial property — a move that will expand the amount of funds available to property developers and improve their liquidity conditions.

The central bank later followed up on the pending cut, along with reductions in some relending rates, in a statement.

Still, the move is unlikely to cheer economists who say that what the world’s second-largest economy needs isn’t cheaper or more abundant loans but rather a pickup in government spending, as well as more forceful efforts to bring a drawn-out real-estate crunch to a close and boost consumer confidence.

“It’s another step in the right direction, but monetary policy by itself is not enough to boost economic momentum,” said Zhang Zhiwei, chief economist at Pinpoint Asset Management.

Tyler Durden

Wed, 01/24/2024 – 07:46