US Leading Indicators Slump Continues – Longest Losing Streak Since ‘Lehman’

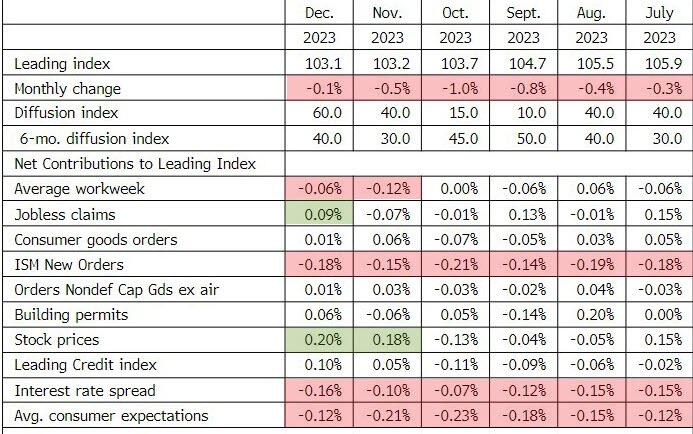

The Conference Board’s Leading Economic Indicators (LEI) continued its decline in December, dropping 0.1% MoM (slightly better than the -0.3% MoM expectations). That is the smallest MoM decline since March 2022.

The biggest positive contributor to the leading index was stock prices (again)at +0.20

The biggest negative contributor was ISM New Ordersat -0.18

This is the 21st straight MoM decline in the LEI (and 22st month of 24) – just barely shorter than the longest streak of declines since ‘Lehman’ (22 straight months of declines from June 2007 to April 2008)

{kind=link}

“The US LEI fell slightly in December, continuing to signal underlying weakness in the US economy,” said Justyna Zabinska-La Monica, Senior Manager, Business Cycle Indicators, at The Conference Board.

“Despite the overall decline, six out of ten leading indicators made positive contributions to the LEI in December.

Nonetheless, these improvements were more than offset by weak conditions in manufacturing, the high interest-rate environment, and low consumer confidence.

As the magnitude of monthly declines has lessened, the LEI’s six-month and twelve-month growth rates have turned upward but remain negative, continuing to signal the risk of recession ahead.

Overall, we expect GDP growth to turn negative in Q2 and Q3 of 2024 but begin to recover late in the year.”

Despite ‘soft landing’ hype, the LEI is showing no signs at all of ‘recovering’, tumbling back below the peak in March 2006…

{kind=link}

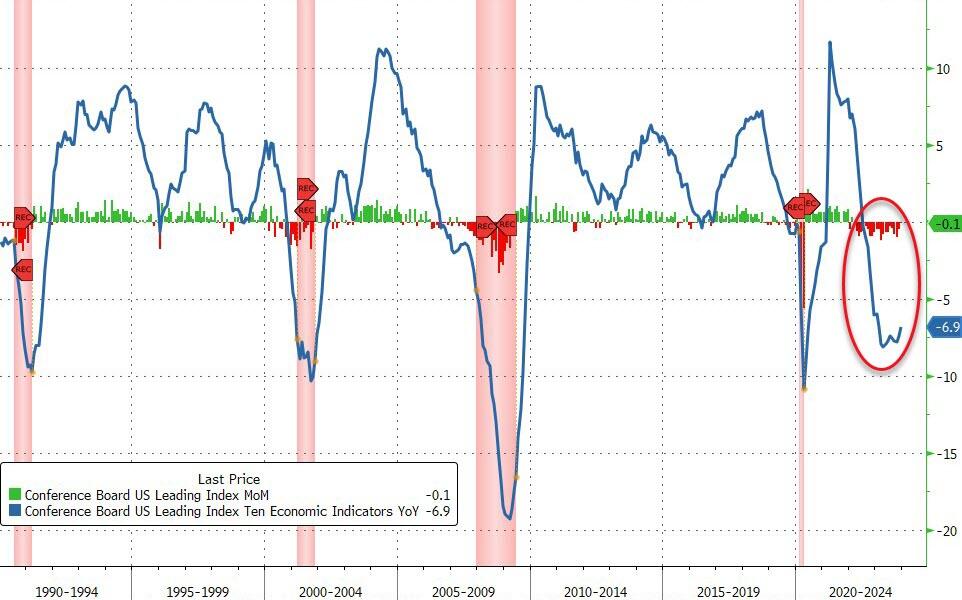

And on a year-over-year basis, the LEI is down 6.9% (down YoY for 18 straight months) – still close to its biggest YoY drop since 2008 (Lehman) outside of the COVID lockdown-enforced collapse (but starting to inflect)…

{kind=link}

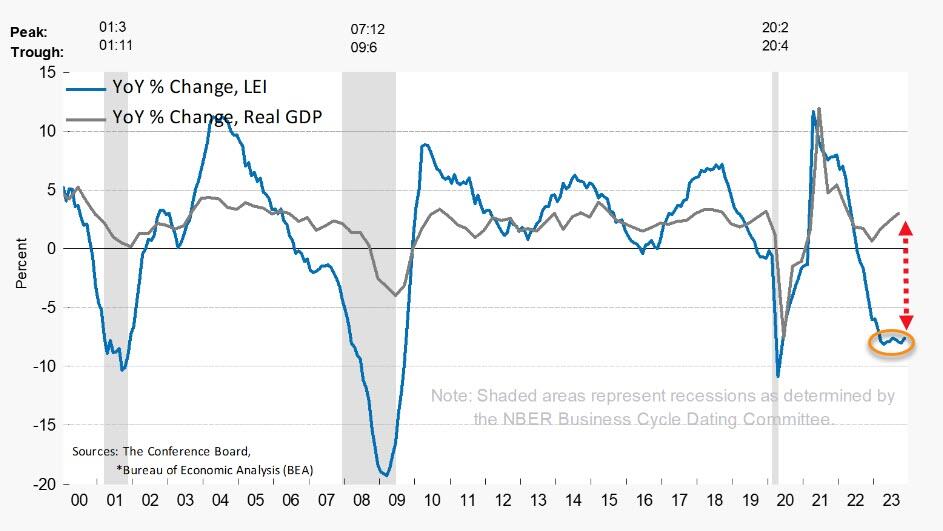

The annual growth rate of the LEI remains deeply negative and decoupled from Real GDP…..

{kind=link}

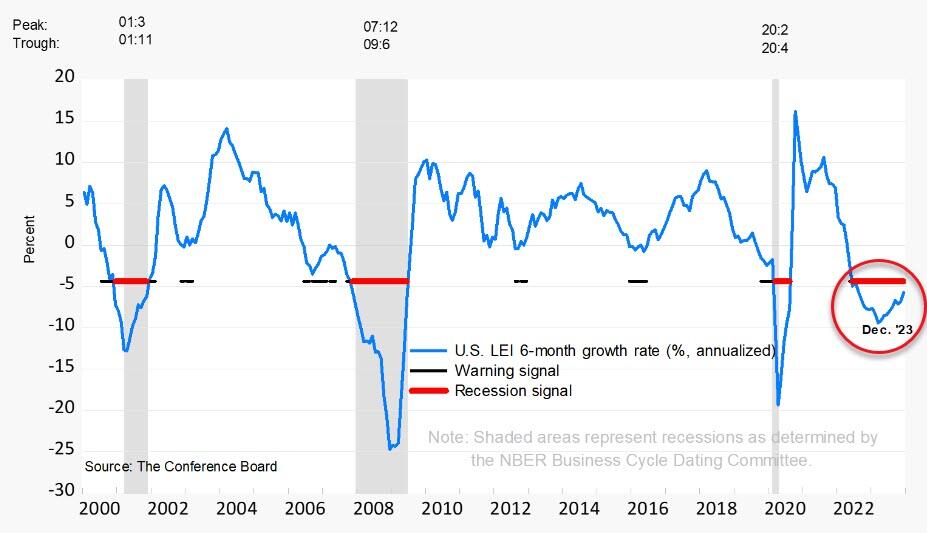

Despite a recent upswing in its 6-month growth rate, the US LEI continues to signal recession…

{kind=link}

Finally, the massive easing of financial conditions in the last few months suggests a turn in LEI is imminent…

{kind=link}

And hence the ‘soft landing’ mission is accomplished… so no need for rate-cuts? (Except for the banking crisis that looms in March).

Tyler Durden

Mon, 01/22/2024 – 10:14