The Intrinsic Value Of Bitcoin And Gold

By Dhaval Joshi of BCA Research

The Intrinsic Value Of Bitcoin And Gold, Finally Explained

{kind=link}

The US Securities and Exchange Commission approval last week for bitcoin spot ETFs marked an important milestone for the cryptocurrency asset-class. Albeit, after bitcoin’s spectacular recent rally, the widely-anticipated ‘news’ was the trigger for some healthy profit-taking, which could run further. Even so, bitcoin is up by 160 percent since the start of last year, unwinding most of the losses through 2022, and making cryptocurrencies by far the best performing asset-class of 2023.

Yet for anybody who is considering buying bitcoin or a bitcoin ETF, an over-arching worry lingers. Does bitcoin have intrinsic value? Many senior economists, politicians, and investors have answered with an emphatic ‘no’. Bank of England governor Andrew Bailey has warned:

“If you want to buy bitcoin, fine, but understand it has no intrinsic value. It may have extrinsic value, but there is no intrinsic value.”

Donald Trump has said:

“I am not a fan of bitcoin and other cryptocurrencies, which are not money, and whose value is highly volatile and based on thin air.”

The unlikely paring of Andrew Bailey and Donald Trump are warning that if bitcoin has no intrinsic value, then it is really nothing more than an elaborate Ponzi scheme. Its value relies entirely on finding somebody else to sell to at a higher price. Or, as the late Charlie Munger put it:

“Bitcoin reminds me of Oscar Wilde’s definition of fox hunting: ‘The pursuit of the uneatable by the unspeakable.’”

The Intrinsic Value Of Bitcoin Is That It Cannot Be Confiscated

Andrew Bailey, Donald Trump and Charlie Munger are wrong. Bitcoin does have intrinsic value. The important insight is that something’s intrinsic value comes not only from what you can do with it, but also from what you cannot do with it.

What you cannot do with bitcoin is confiscate it.

This is significant because throughout history, the state and institutions have confiscated our wealth. They have done so in three ways:

Through monetary inflation, which confiscates the real value of our wealth by stealth.

Through the failure of banks and other financial institutions that have custody of our wealth.

Through the outright expropriation of our wealth as, for example, was suffered by European Jews in the 1930s.

Crucially, bitcoin cannot be confiscated in any of these ways.

{kind=link}

This is not to say that bitcoin cannot be stolen. If someone forces you, at gunpoint, to give them the keychain to your bitcoin wallet, they can steal your bitcoin. But it would be almost impossible for the state or institutions to confiscate everyone’s bitcoin in this way.

The state could ban bitcoin, but this would not be confiscation. So long as there remained a critical mass of bitcoin users globally, your wealth would remain yours.

And of course, like any asset, bitcoin can be subject to fraud. If you pay someone to buy bitcoin on your behalf and they pocket the cash, then this is just old-fashioned fraud. Which is what the FTX scandal was.

But once you have a bitcoin in your own digital wallet, it is almost impossible for the state to confiscate it either through inflation, or through bank failure, or through outright expropriation. This is what gives bitcoin its intrinsic value: its ‘non-confiscatability’.

Most Of Gold’s Value Also Comes From Its ‘Non-Confiscatability’

Gold is also non-confiscatable in two out of the three ways. Gold cannot be confiscated by inflation, given its controlled supply. And gold cannot be confiscated by bank failure.

This leads to a second insight. All of gold’s value is ‘intrinsic’ with one part coming from its chemical and physical properties – its inertness that makes it suitable for jewellery which stays eternally beautiful, plus its high electrical and thermal conductivity. And the other part coming from its non-confiscatability.

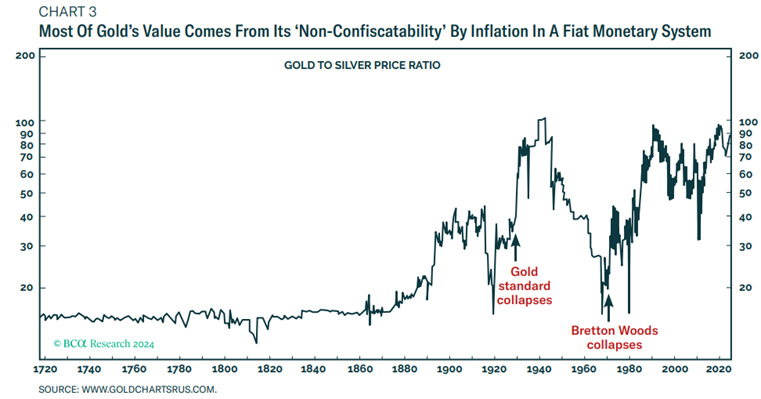

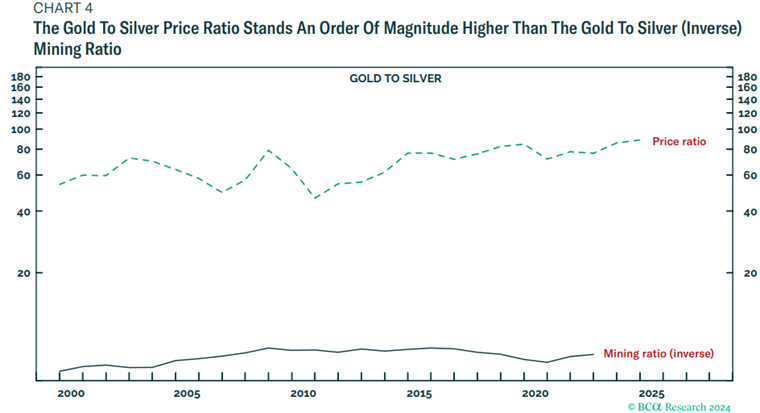

To quantify these two parts, note that other precious metals – silver, platinum, and palladium – can substitute for the chemical and physical properties of gold. So, if all of gold’s value came from its chemical and physical properties, then the gold to (say) the silver price ratio would just track the relative scarcity of gold to silver, as captured by the so-called ‘mining ratio’.

Indeed, for centuries, the gold to silver price ratio did just track its mining ratio. But when the world moved to a fiat monetary system – after the collapse of the gold standard in 1931 and then again after the collapse of the Bretton Woods ‘pseudo gold standard’ in 1971 – the gold to silver price ratio surged to well above its mining ratio. This is because in a fiat monetary system, the dominant part of gold’s value became its non-confiscatability through monetary inflation.

Today, gold is eight times as scarce as silver based on its mining ratio, but the gold to silver price ratio stands an order of magnitude higher, at 88 times.

{kind=link}

Hence, the gold price of $2050/oz comprises around $190/oz of intrinsic value for its chemical and physical properties (around 10 percent), and around $1860/oz of intrinsic value for its non-confiscatability (around 90 percent).

Given that the above ground value of gold stands at $15 trillion, the 90 percent share that represents its non-confiscatability equals $13.6 trillion. Meanwhile, the market value of cryptocurrencies equals $1.7 trillion. Meaning that the total market value for non-confiscatability is $15.3 trillion, of which gold comprises 89 percent and cryptocurrencies just 11 percent.

Bitcoin Will Displace Gold In The $15 Trillion Non-Confiscatability Market

The structural bull case for bitcoin is simple. First, that the $15.3 trillion market for non-confiscatability will grow in line with the growth in global wealth. And second, that bitcoin will displace gold to take an increasing share of this market.

After all, bitcoin is superior to gold in its non-confiscatability. While neither bitcoin nor gold can be confiscated through inflation or bank failure, gold can be confiscated by outright expropriation as happened to European Jews during the 1930s. Yet it is almost impossible to confiscate bitcoin in this way.

Assuming that in the next few years, the non-confiscatability market grows to around $20 trillion and that cryptocurrencies increase their share of this market to around 20 percent, this would imply that bitcoin’s market value could more than double. As the supply of bitcoins is now reaching its upper limit, it would equate to the bitcoin price rising to well north of $100,000.

Turning to gold, with cryptocurrencies gradually displacing it in the non-confiscatability market, the major source of gold demand is petering out. As such, the real price of gold is likely to stay in the sideways range that it has been in for the past ten years.

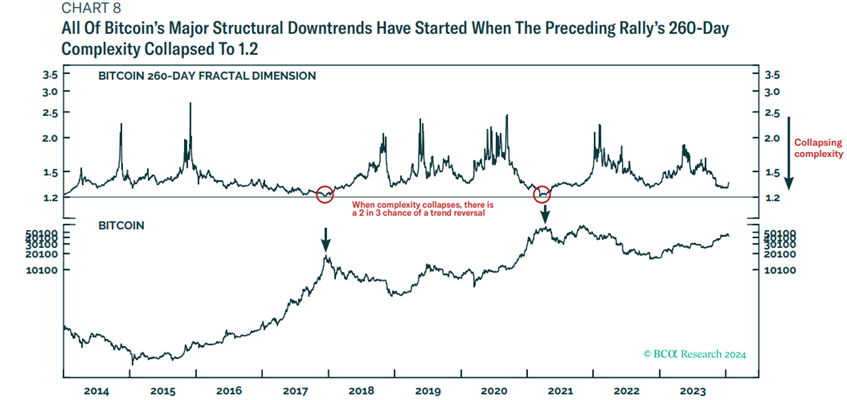

Finally, bitcoin and gold are highly susceptible to trending. Such trends, and specifically their vulnerability to reversal, are best analyzed by the breakdown in their complexity. In the case of gold, its recent rally has reached the collapsed 65-day complexity that has reliably marked previous short-term turning points.

As such, a tactical recommendation is to short gold, setting a profit target and symmetrical stop-loss at 5 percent.

This brings us to our third and final insight. All of bitcoin’s major structural uptrends have started when the preceding sell-off’s 260-day complexity collapsed to 1.3. Whereas all of bitcoin’s major structural downtrends – so-called ‘crypto winters’ – have started when the preceding rally’s 260-day complexity collapsed to an even lower level of 1.2.

{kind=link}

Despite bitcoin’s strong recent rally, its 260-day complexity is not yet close to the 1.2 level that would signal the start of another crypto winter. Hence, while we should expect a near-term countertrend move, the structural uptrend that started in November 2022 is still intact.

Tyler Durden

Fri, 01/19/2024 – 11:25