China Stocks Hit Rock Bottom: After $6.3 Trillion Market Loss, Brokers Suspend Short-Selling

Amid ‘snowball derivative liquidations‘, China’s stock market is falling faster than its population.

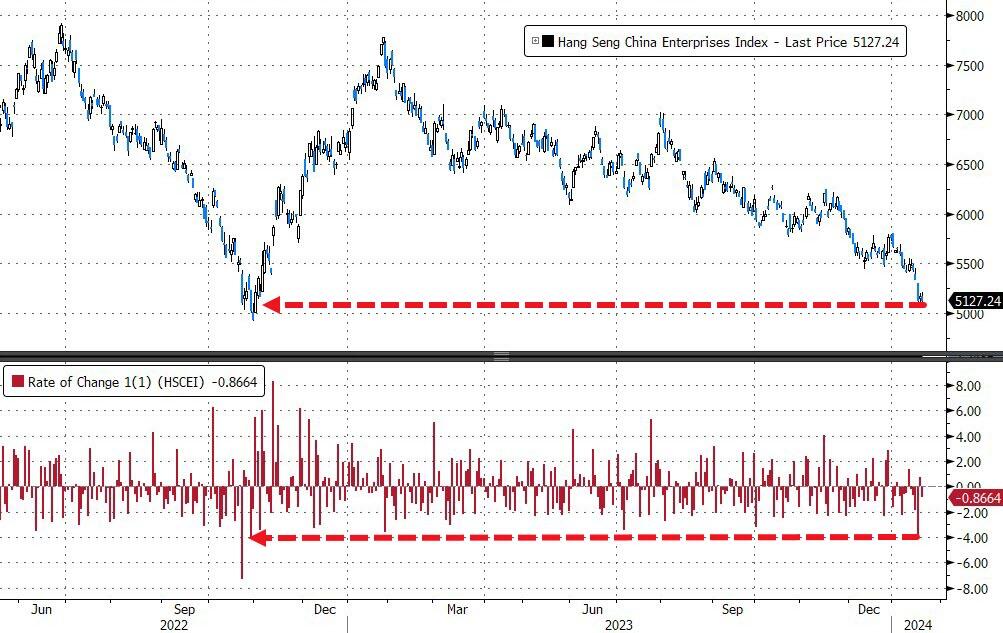

The Hang Seng China Enterprises Index crashed 6.5% this week – its worst weekly loss since March 2023 with Wednesday seeing the biggest daily loss since Oct 2022 as the index plummeted to key support levels around the Oct 2022 lows…

{kind=link}

Source: Bloomberg

For context, Chinese and Hong Kong stocks have seen some $6.3 trillion of market value wiped out since a peak reached in 2021…

{kind=link}

Source: Bloomberg

But, as we detailed earlier in the week, authorities have ruled out the use of massive stimulus to revive the flagging economy, leaving traders wondering when things will improve.

“What we are seeing this year so far really is a continuation of what we saw last year,” John Lin, AllianceBernstein’s chief investment officer of China equities, said in an Jan. 17 interview on Bloomberg TV.

“These squeezing-the-toothpaste type of stimulus policies so far haven’t been able to turn around the underlying bottom-up fundamentals of areas like the property sector.”

It gets worse as China is setting grimmer and grimmer milestones by the day:

Tokyo has overtaken Shanghai as Asia’s biggest equity market…

{kind=link}

India’s valuation premium over China has hit a record.

{kind=link}

Locally, a meltdown in Chinese shares is wreaking havoc on the nation’s asset management industry, pushing mutual fund closures to a five-year high.

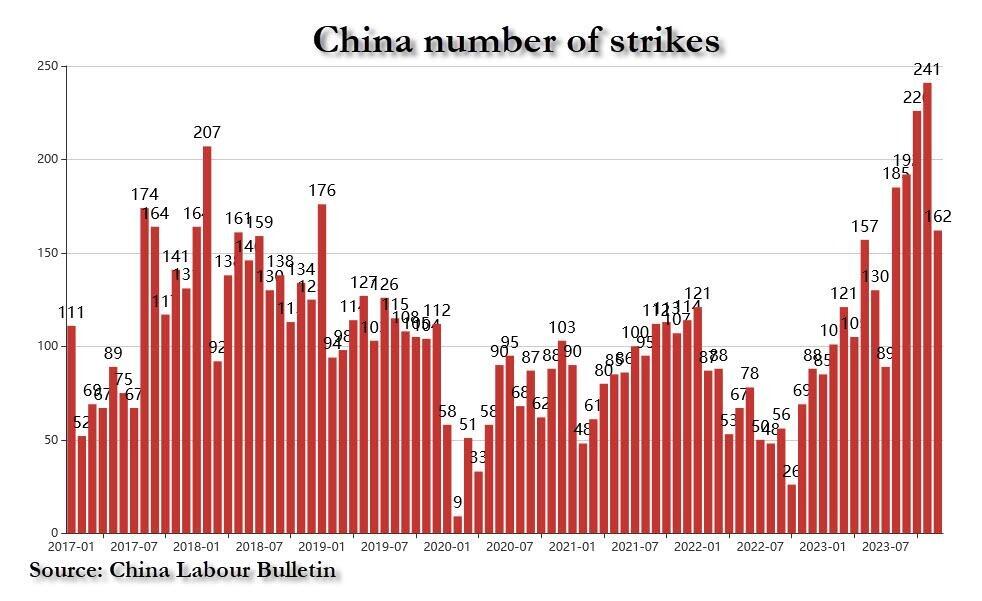

Most importantly, as we noted previously, the lack of stimulus (amid China’s real estate sector crisis and escalating tensions with Washington on trade) has had a very adverse impact on both economic and market sentiment at a time when China’s middle class is growing increasingly restless and pitchforky, resulting in a surge in labor strikes and (mostly peaceful) protests.

{kind=link}

And while a quiet, painless sovereign suicide may be an option for Japan – with its demographic disaster and rapidly aging population where more adult than baby diapers have been sold for years; for China – which still has a young, vibrant and increasingly angry population – this is not an option as the coming tidal wave of unrest could easily result in the one thing the Chinese Communist Party dreads the most, a revolution.

For now, Beijing refuses to unleash a monetary bazooka – amid its longest period of deflation since 1998 – but that doesn’t mean it won’t step in to try and arrest the collapse of the stock market (which along with real estate) is a considerable source of ‘wealth’ for the Chinese.

“The government seems very sanguine about the economy,”said Xin-Yao Ng, an investment director for Asian equities at abrdn.

“The market might not even trust the 5% growth figure, it certainly has a much more negative view on the economy and definitely believes Beijing needs a big fiscal response.”

{kind=link}

With that in mind, just a day after unleashing The National Team (China’s Plunge Protection Team), Bloomberg reports that China’s largest brokerage has suspended short selling for some clients in mainland markets, according to people familiar with the matter.

State-owned Citic Securities Co. has stopped lending stocks to individual investors and raised the requirements for institutional clients this week after so-called window guidance from regulators, said the people, asking not be identified discussing a private matter.

Of course, as we have pointed out numerous times (most recently here for example), researchhas consistently shown that banning short selling during stretches of particularly volatile equity market activity intensifies the volatility.

Such prohibitions impede investors from determining accurate prices of assets and reduce market liquidity.

Moreover, short-selling bans in one market can increase volatility in other marketsas some investors try to circumvent the ban.

But since when has historical evidence of the failure of policies ever stopped any politician from ‘doing something’ or blaming someone.

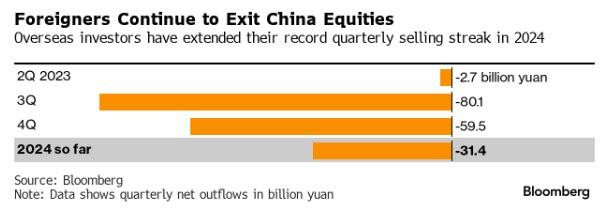

Everything that Chinese authorities have tried has failed to convince money managers that the worst is behind us. As Bloomberg reports, Asian funds have cut their allocation to China by 12 percentage points to a net 20% underweight, the lowest in more than a year, according to the latest Bank of America survey.

Managers of benchmark-tracking funds have sold a net $300 million of shares traded in mainland China and Hong Kong this month, according to a Morgan Stanley analysis.

That’s a reversal from the last half of 2023, when they bought $700 million on a net basis even as stock indexes declined.

{kind=link}

“China is a waiting game and we continue to be waiting,”said Mark Matthews, head of Asia research at Bank Julius Baer & Co., which is mostly avoiding Chinese equities.

How much longer can Beijing wait?

Tyler Durden

Fri, 01/19/2024 – 12:25