There’s Not Much Upside To Chasing Bunds From Here

Authored by Ven Ram, Bloomberg cross-asset strategist,

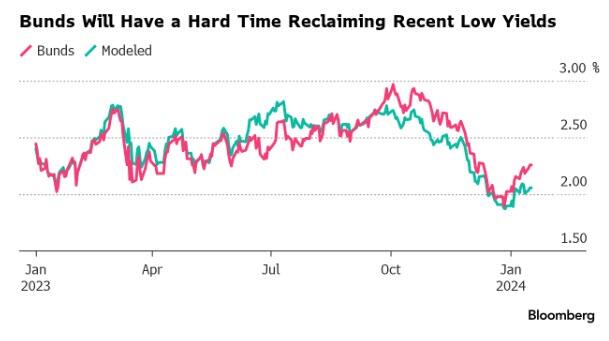

German’s long-dated bonds have rallied deep and hard since the start of the fourth quarter, leaving them with minuscule further upside in 2024.

The yield on the nation’s 10-year bonds slumped as much as 95 basis points to 1.89% at the end of December.

They have since corrected to around 2.25% on Tuesday.

A model of yields based on interest-rate swaps, the European Central Bank’s policy rates and front-end sovereign notes that can explain more than 98% of movements in Germany’s long-dated bonds shows that bund yields won’t be able to probe below 2% this year – unless the ECB were to cut interest rates deeper and more aggressively than what the markets are currently pricing.

{kind=link}

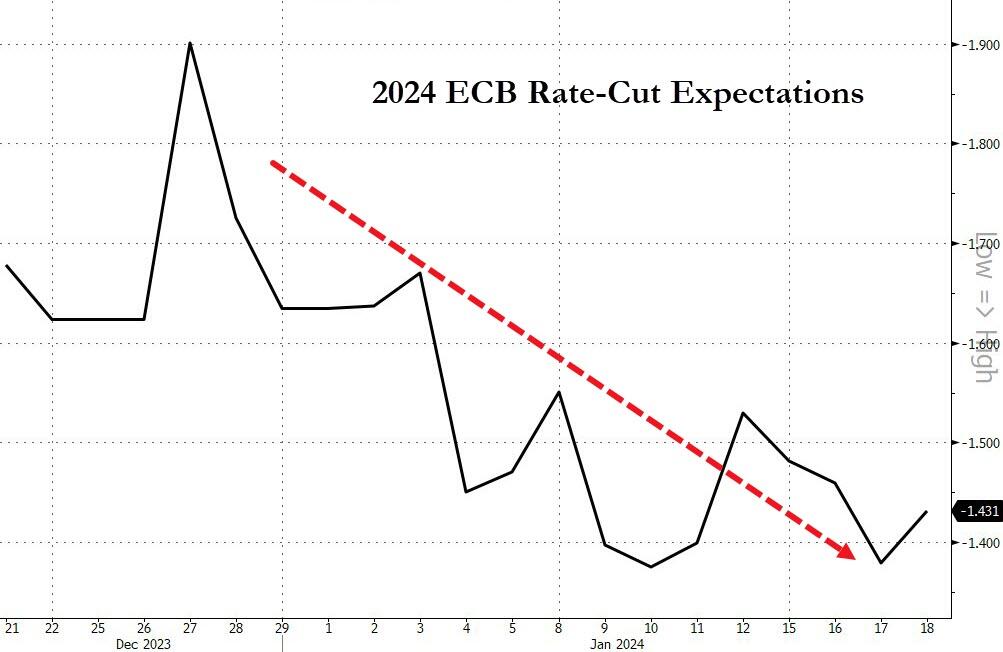

ECB officials have been pretty vocal in recent days, suggesting that the central bank may not cut rates as soon as March.

{kind=link}

Neither have they seemed willing to lower rates as many as six times this year, which interest-rate traders have been using as their ballpark.

{kind=link}

Governing Council member Joachim Nagel remarked that any reduction can wait for the summer break, a view that President Christine Lagarde subsequently endorsed, citing consensus among officials.

While one could dismiss Nagel’s stance as that of a arch-hawk, even the more dovish Philip Lane said that reductions that are too quick might stoke a new wave of inflation, putting policymakers in “a far worse scenario.”

Lane also commented that Eurostat national accounts data – which he highlighted as key to the ECB’s policy decision – would be available in time for the June rate review, pouring cold water on the possibility of rate cuts sooner.

His colleague Madis Muller remarked that the market’s pricing of some 150 basis points of reductions this year “is quite an aggressive expectation indeed,” given labor costs in the euro zone. The annual increase in regional wages is running above 5%, while the jobless rate is at the lowest it has ever been, which may yet keep inflation simmering.

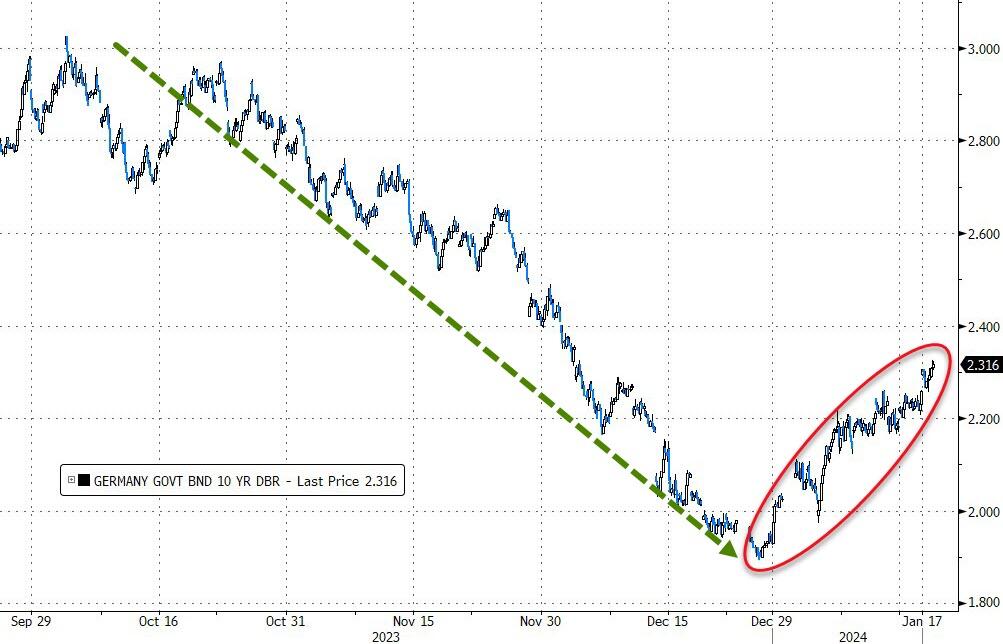

Germany’s 10-year bond yield slid precipitously from almost 3% at the start of October through the end of December.

While the start of the new year has seen a paring back of that exuberance, the correction may have further to run.

{kind=link}

That’s not to say that bund yields will climb a whole lot from here given that the ECB will still cut rates this year.

Rather, the point is that the deep rally of the past three or so months has fundamentally skewed the risk-reward equation on bunds for the remainder of 2024.

Positioning for a re-visit of the December lows seems premature.

Tyler Durden

Thu, 01/18/2024 – 05:00