Regulator Readies For End Of Fed Bank Bailout Fund As ‘Arb’ Volumes Explode Higher

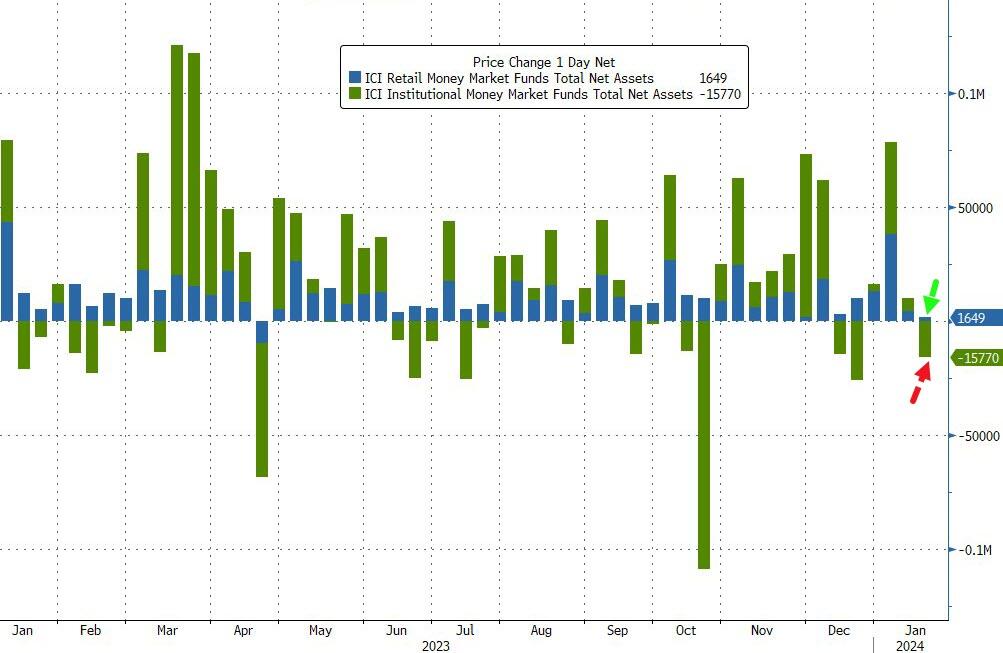

Money-market fund assets notched their first net weekly outflows in a month, led by declines in government funds as investors reallocated portfolios in the early days of the new year. Total assets dropped $14.1BN to $5.961TN from $5.975TN the week prior, which was a record high…

{kind=link}

Source: Bloomberg

Retail funds saw yet another inflow (of $1.6BN) while Institutional funds saw $15.8BN outflows…

{kind=link}

Source: Bloomberg

In a breakdown for the week to Jan. 17, government funds – which invest primarily in securities like Treasury bills, repurchase agreements and agency debt – saw assets fall to $4.862 trillion, a $15.7 billion decrease.

Prime funds, which tend to invest in higher-risk assets such as commercial paper, meanwhile, saw assets rise to $978.3 billion, a $5.2 billion increase.

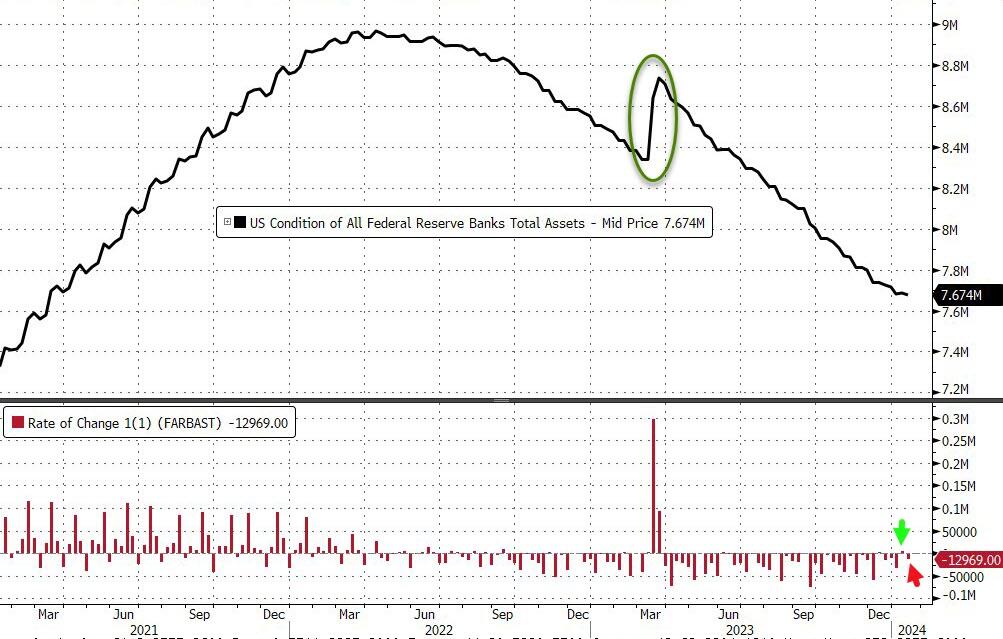

After its biggest increase (+$5.7BN) since the SVB crisis last week, The Fed’s balance sheet shrank by $13BN last week to a new cycle low of $7.674TN (the lowest since March 2021)…

{kind=link}

Source: Bloomberg

The Fed’s reverse repo facility continues to see drawdowns, pointing to the source of liquidity zero-ing out by March as we have warned about.

Bank reserves at The Fed continue to rebound strongly(helped by the drawdowns from RRP to their highest since April 2022), catching up to equity market cap’s recent gains…

{kind=link}

Source: Bloomberg

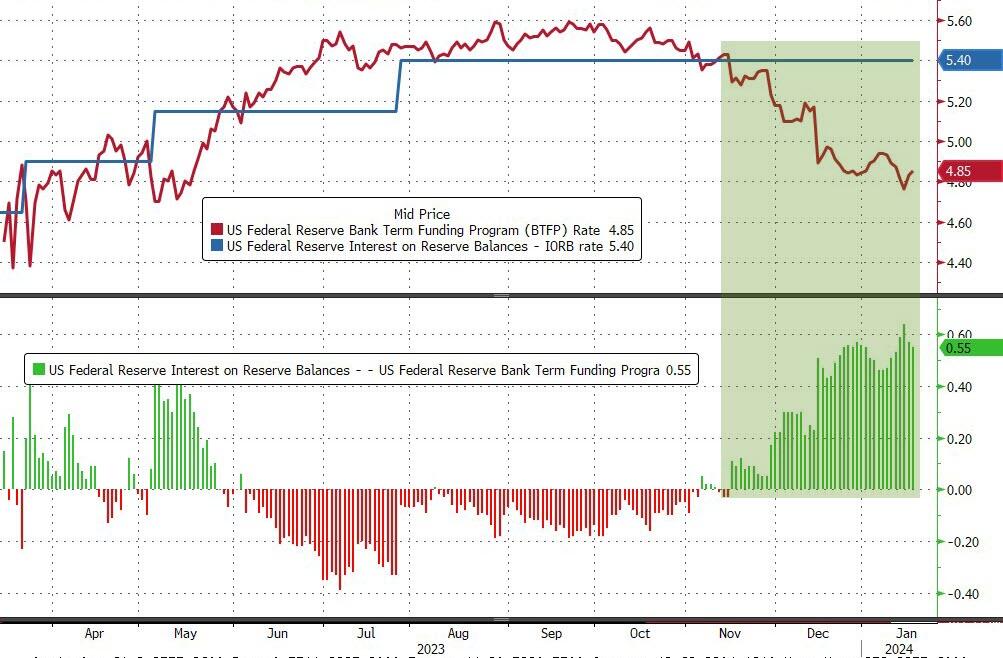

Additionally, usage of The Fed’s bank bailout facility (BTFP) exploded higher by $14.3BN last week (presumably as everyone piled into the arb) to a new record high of $162BN…

That is the biggest weekly jump since the SVB crisis…

{kind=link}

Source: Bloomberg

The Fed has totally lost control of its BTFP facility as it has risen by over $47BN since the arb existed.

And the Fed-BTFP Arb remains alive and well and offering 55bps of free money to every bank that qualifies…

{kind=link}

Source: Bloomberg

And it appears our warnings that is becoming more likely that The Fed will be able to keep the bank bailout (BTFP) plan alive after its planned obsolescence in March have been proven right.

“In justifying the generous terms of the original program, the Fed cited the ‘unusual and exigent’ market conditions facing the banking industry following last spring’s deposit runs,” Wrightson ICAP economist Lou Crandall wrote in a note to clients.

“It would be difficult to defend a renewal in today’s more normal environment.”

Expanding on earlier plans that we detailed here to reduce banks’ ability to use FHLB as an implicit funding tool, Bloomberg reports today that US regulators are preparing to introduce a plan to require that banks tap the Federal Reserve’s discount window at least once a year to reduce the stigma and ensure lenders are ready for troubled times.

In an interview, Michael Hsu, the acting comptroller of the currency, said the changes regulators will propose aim to ensure banks are more prepared to respond to sudden flights of deposits.

“We want to make sure that banks have enough resources to meet any kind of outflows within five days—especially those related to uninsured deposits,” Hsu said.

He added that the plan will also seek to remove any stigma associated with borrowing from the Fed’s discount window.

Hsu is the latest top US regulator to flag the need for banks to be more comfortable using the discount window.

“Banks need to be ready and willing to use the discount window in good times and bad,”Michael Barr, the Fed’s vice chair for supervision, said in December.

Maybe banks are starting to realize this won’t be painless…

{kind=link}

To make the discount window more attractive, the government is considering ways to make it cheaper for borrowers, according to a person familiar with the rule-writing effort.

The proposal could also affect how assets such as high-quality bonds and mutual funds, which are frequently held as collateral to gain discount-window access, can be counted on a bank’s balance sheet, said the person, who asked not to be identified as the plans haven’t been released.

Translation: all the “pay me at par” rules of the BTFP will now be applied to the discount window… but maybe not the arbitrage.

Well, now we know where the regional banks will be going for funding…

*US PLANS TO PUSH MORE BANKS TO USE THE FED’S DISCOUNT WINDOW

translation: many more banks will HAVE to use the discount window… right after the BTFP expires

— zerohedge (@zerohedge) January 18, 2024

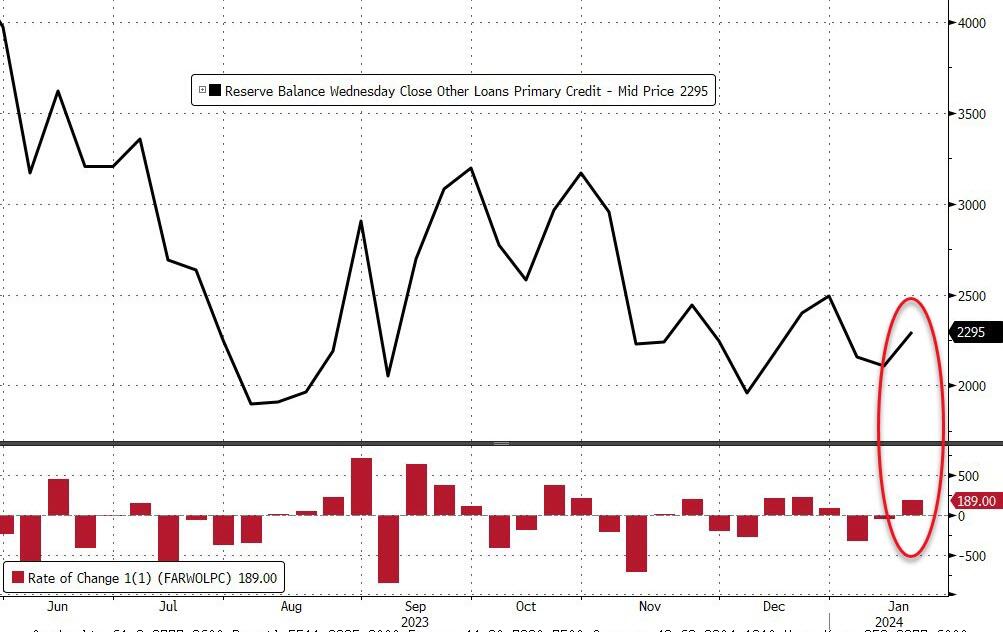

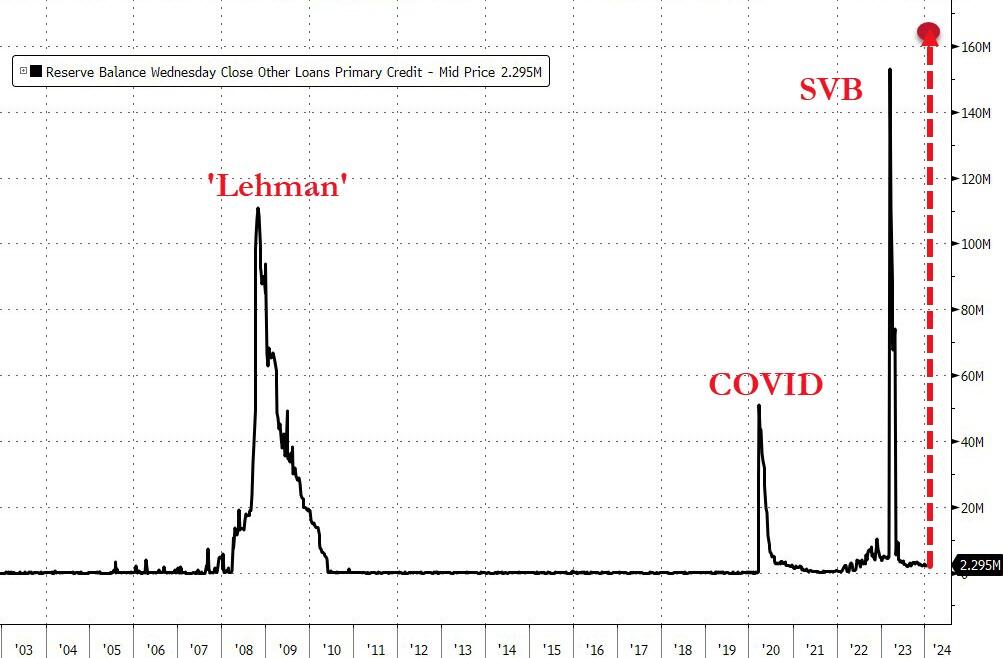

Can the discount window cope with the sudden need for over $147 Billion?

Last week saw usage of the discount window rise $189 Million to $2.295 Billion…

{kind=link}

What do you think?

{kind=link}

It is clear that The Fed is well aware of the problem it faces on March (or sooner). As we noted previously, the potential for this liquidity crisis created the possibility of a worrying chain reaction – from the Fed’s balance sheet, via the money market funds and the private repo market, through the basis trade and on to the demand for Treasuries, at a time when the US government is coming to market with massive amounts of issuance.

Instead of scarce bank reserves creating liquidity problems and forcing the Fed to stop QT, it may well be the exhaustion of the ON RRP and the upending of the hedge fund basis trade that causes problems in 2024. The worrying difference now is that there is no Fed backstop for hedge funds and the high degree of leverage used in the trade could lead to liquidity problems proliferating even more quickly through the financial system.

This may be too late to avert a severe bout of bond market volatility, though.

Either way, the Fed is on course to end QT and restart QE in the coming months, against a backdrop of loose fiscal policy and a still-resilient economy, opening the door to a reappearance of inflationary pressures that the Fed may have little appetite (or ability) to restrain.

And that’s why The Fed will cut rates no matter whether employment is at record highs or inflation is re-igniting.

Tyler Durden

Thu, 01/18/2024 – 16:45