Figuring It All Out

Submitted by QTR’s Fringe Finance

For two years, the question has been the same: when is something going to give, and when are we going to see some real volatility in some market — anymarket — thanks to 5% interest rates?

The answer, it turns out, may be simpler than I thought.

I gave up a long time ago trying to figure out whether the market is going to flash crash or melt up as a result of aggressive further easing. If I had to handicap the situation today, I’d predict both are going to happen: we will see a sharp decline in the market, as a result of either a black swan event, disappearing liquidity, an unexpected blowoff valve (more on this in a bit) or all of the above, which would trigger margin calls and a deleveraging. Then, from there, I would predict an unprecedented response from the Fed, who would flood the system with money and easing in a way that was larger by any factor than how they have done it in the past.

Whatever outcome occurs should be irrelevant thanks to the way that I positioned myself heading into the year. I’m hedged and short the indexes and a couple of specific names that I believe would plunge in the event of a market pullback. At the same time, I will be ready to use any profit from a sharp downturn to purchase sound money assets – namely, gold and silver, miners, first and foremost, and maybe some real estate and bitcoin – should they also wind up selling off in any type of panic that encompasses all assets.

{kind=link}

But for me the bizarre thing is how long it has taken for either of these situations to take place. For all intents and purposes, the market has been in a very relaxed, slow and steady melt-up over the last two years despite interest rates being hiked at a record pace, record levels of outstanding debt, and mounting geopolitical instability.

I was starting to feel like it was officially time to don my tinfoil hat and ask questions about whether or not the markets are being held up unnaturally by the plunge protection team. Well, to be honest, I alwaysthink they are, but I mean, asking questions about whether or not it’s happening more now than ever.

But then I came across a couple of interesting facts that made me once again believe that my thesis could be correct, but my timing could just be wrong. On this blog, I often reference a sign in my local Korean deli above the sandwich counter that says:

“You never need patience more than when you are about to lose it.”

The sign makes the point that when you feel like despair is setting in, you may be the closest you’ve ever been to what you’ve been waiting for.

So here are two new pieces of data to chew on that I found this weekend.

First is data that came out of the San Francisco Fed back in November indicating that household savings left over from the pandemic were actually running a bit higher than people had expected.

Those that read me regularly know my belief that diminishing personal savings and rising credit card debt will eventually lead to increased delinquencies and then economic and stock market volatility. It’s possible that the system was simply bombarded with so much excess cash as a result of COVID that it hasn’t run out yet. Here’s the San Francisco Fed:

Figure 1 incorporates the recent data revisions to show how our updated estimate of cumulative excess savings in the aggregate economy changed following the BEA’s update. Figure 1 also incorporates the subsequent BEA data release for September 2023. Accumulated excess savings, estimated in nominal terms, totaled more than $2.1 trillion by August 2021 when it peaked. This is largely unchanged from the total pre-revision value.

Since then, the drawdown on household savings—that is, when aggregate personal savings dip below the pre-pandemic trend—has been slower than previously believed. The new estimates average about $75 billion per month, compared with $100 billion per month before the data revisions.

Figure 2 compares the latest post-revision measures of actual personal savings and the pre-pandemic savings trend. The red area shows our updated estimate for cumulative drawdowns. As of September 2023, this reached about $1.7 trillion of the $2.1 trillion in total accumulated excess savings (green area). This latest update implies that around $430 billion of excess savings remains in the aggregate economy.

They predict that excess savings will last until “sometime” in the first half of 2024:

If the recent pace of drawdowns persists—for example, at average rates from the past 3, 6, or 12 months—aggregate excess savings are likely to remain available in the overall economy until sometime in the first half of 2024.

And interestingly enough, this is similar to the thesis that Larry Lepard put forth on my podcast over the weekend.

Talking about why the market hasn’t crashed yet, Larry said: “I have a theory and I could be wrong, but it’s stunning to me. You know what’s happened to me, it’s been the most frustrating piece of the last year or two. I mean, I was, you know, if you’d asked me at the beginning of this year, ‘Will the stock market go back and revisit its old or exceed its old high?’ I’d have said there’s just no way. And of course, I was dead wrong.”

50% OFF ALL SUBSCRIPTIONS: Subscribe and get 50% off and no price hikes for as long as you wish to be a subscriber.

He added: “But I found a chart, it’s going to be in my most recent quarterly, which will be out in a few days, and it’s a very interesting chart. It talks about federal government spending and what it shows is that we were kind of ticking along in the $4 trillion range, then COVID came along and just blew things out. You know, we went to six, seven trillion in one year. And what’s amazing to me is COVID’s gone now, right, and yet the spending is still at that level. Chris, I mean, we’re at 6.1 [trillion] last year, and so, you know, it’s really kind of this Inflation Reduction Act, of course, which is just a sick joke, and the fact that the debt ceiling won’t be revisited until January of 2025, has just, you know, they’re spending like drunken sailors.”

“And this is further evidenced, if you look at the December number that just came out from the CBO, the Congressional Budget Office,” Larry said.

“I mean, the year-on-year deficit in December was up 20%. And so for the first quarter, the deficit was 500 plus [billion] dollars, and usually, the first quarter is one of the better quarters, implying that next year will be over $2 trillion. Last year we were at one. So, you know, I think what’s going on is just all this free money, and I shouldn’t say free money, all this aggressive spending by the federal government.”

You can listen to Larry’s full interview here:

Finally, everybody should watch Luke Gromen’s analysis of the situation from Palisades Gold Radio out just hours ago.

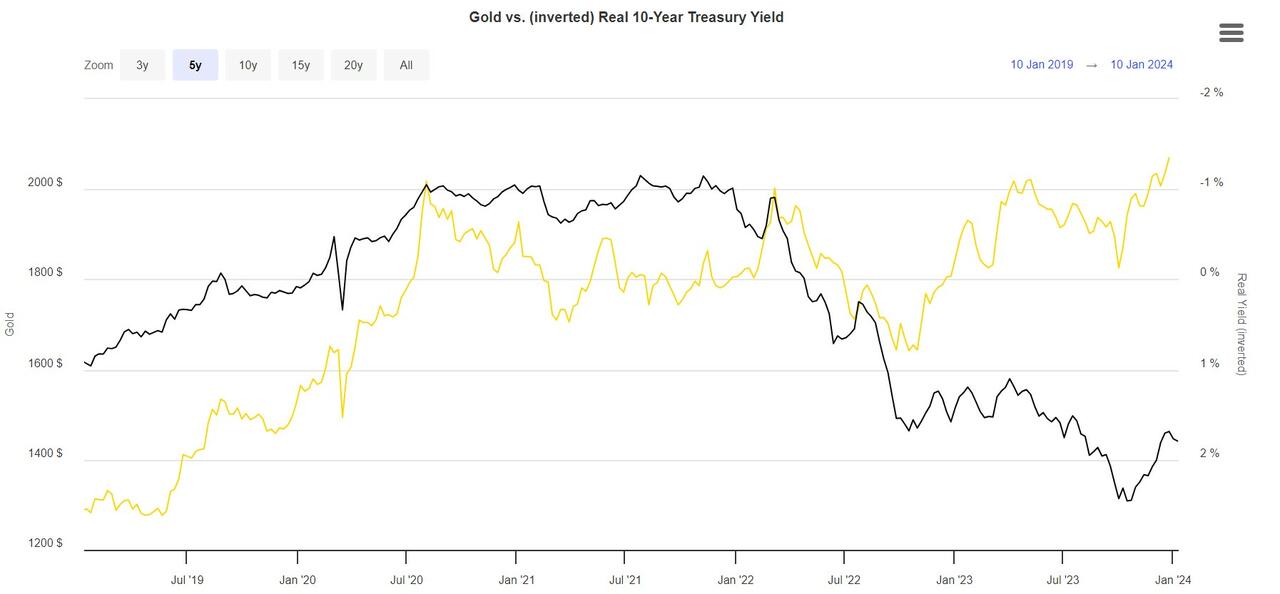

In it, he postulates that the treasury market is calling all of the shots and that the Fed will almost certainly devalue the dollar and sacrifice long-term debt in favor of keeping the system from crumbling. This would support a scenario where gold and other sound money assets moon and, importantly, Luke points out that this is why the price of gold may have separated from real rates for the first time in his career (i.e. money is starting to move out of the $150 trillion long term debt market as people figure this out, and is starting to trickle into sound money assets).

{kind=link}

In the above chart, look at how the relationship between real 10Y rates and gold changed from Fall 2023 until now. Luke explains what the widening delta means and lays out in great detail how the treasury market is driving the bus here:

All of the above scenarios — even if we get a sharp downturn at some point — wind up with the dollar losing significantly more purchasing power heading forward. Almost every reasonable potential outcome fiscally and monetarily will eventually benefit sound money assets, in my opinion, making it easy to relax with gold miners my best idea for the new year.

And look, I don’t necessarily feel rushed for my thesis to play out, as long as it does play out over time. If we go the hyperinflation route without having a crash, I expect assets like gold to skyrocket in tandem. If we get the economic collapse, I expect to cash in on my hedges and put cash to work at points of peak panic, perhaps before the Fed steps in, or maybe even at the early stages of rate cuts. Either way, I would describe my strategy as being volatility-based, and not so much reliant on what direction the market goes. I’ve already written about dozens of different stock ideas that I find intriguing for the forthcoming year and I’ve got my shopping list ready if the market tanks.

But for those who know me, I still think miners are the absolute best bet to hedge against all different types of risk heading into this year.

And so this weekend I reminded myself that if Larry Lepard and the San Francisco Fed (and Luke Gromen) are right, and we are literally holding onto the last thread of personal savings before liquidity completely dries up, it could be sooner than we think before the only outcome I believe to be a mathematical certainty – volatility – takes hold.

Certainly, you can call me a cynic, but I feel like the louder the financial media celebrates a soft landing, the more likely we are, the closer we are to the edge of the volatility cliff. Either way, these perspectives make up important context as we make our way into the new year and I’d encourage you to listen to the above interviews and carefully continue to watch personal savings data.

Now read:

More Ideas For 2024: Harris Kupperman’s Position Review

Modern Monetary University Plagiarism Theory

7 More Stocks To Watch In 2024

24 Stocks I’m Watching For 2024

QTR’s Disclaimer: I am an idiot and often get things wrong and lose money. I may own or transact in any names mentioned in this piece at any time without warning. Contributor posts and aggregated posts have not been fact checked and are the opinions of their authors. They are either submitted to QTR, reprinted under a Creative Commons license or with the permission of the author. This is not a recommendation to buy or sell any stocks or securities, just my opinions. I often lose money on positions I trade/invest in. I may add any name mentioned in this article and sell any name mentioned in this piece at any time, without further warning. None of this is a solicitation to buy or sell securities. These positions can change immediately as soon as I publish this, with or without notice. You are on your own. Do not make decisions based on my blog. I exist on the fringe. The publisher does not guarantee the accuracy or completeness of the information provided in this page. These are not the opinions of any of my employers, partners, or associates. I did my best to be honest about my disclosures but can’t guarantee I am right; I write these posts after a couple beers sometimes. Also, I just straight up get shit wrong a lot. I mention it twice because it’s that important.

Tyler Durden

Thu, 01/18/2024 – 15:40