Why The Market Is Gunning For An Early Fed Rate-Cut

Authored by Simon White, Bloomberg macro strategist,

The high degree of certainty the Federal Reserve will deliver an early rate cut – which is a fait accompli historically when pricing is as skewed as it is today – is a sign the market perceives financial-instability risks are rising, and that a near-term reduction in rates is required to help prevent liquidity and funding issues from developing.

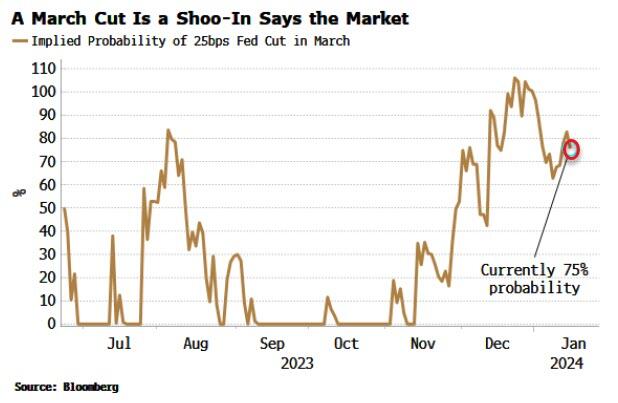

The curious case of the March rate-cut rumbles on. Several theories have been put forward for why the market is ascribing such a high probability to it, such as more dovish economic data, or large yield-curve steepening positions skewing front-end rate pricing.

None really pass muster when you look more closely at them.

But under the lens of reserves and financial-stability risks, things start to make more sense.

{kind=link}

This is controversial.

A shibboleth of central banking is the “separation principle,” the idea that monetary policy is distinct from financial stability. As Cameron Crise noted last week, in a response to my view that Fed balance-sheet dynamics are playing a much bigger part in the market’s rate outlook, Jerome Powell himself has recently invoked the principle, noting the two are on “independent tracks.”

But the separation principle was always questionable, something the Bank for International Settlements has long argued might be correct in theory, but is wrong in practice. Funding costs, leverage incentives and risk-taking – all influenced by the size and composition of the Fed’s balance sheet – affect credit growth and asset prices.

That’s even more the case when the government is running a large fiscal deficit as it is today. Interest payments are poised to become an ever-greater drain on reserves and reserve velocity, intensifying the risks from the Fed’s ongoing quantitative tightening program.

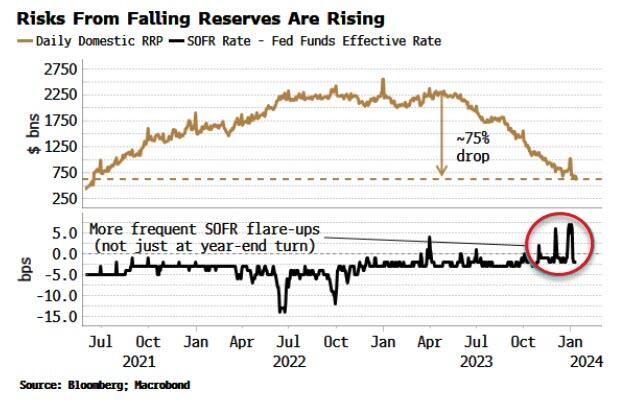

The savior of market liquidity in the face of vast government supply has been the Treasury’s decision to issue mainly bills, allowing the liquidity parked at the Fed’s reverse repo facility (RRP) to harmlessly absorb much of this supply.

But now the RRP is dropping rapidly, and continues to fall as money market funds’ assets keep rising and bill yields remain attractive.

But the closer the RRP gets to zero, the nearer we are to the point where reserves are approaching their so-called lowest comfortable level, and funding problems could ignite as they did in September 2019.

In a sign risks are already rising, SOFR has jumped higher on more frequent occasions in recent months.

{kind=link}

As a result, several banks have brought forward when they believe the Fed will begin to taper and then end QT.

JP Morgan, Bank of America and Barclays believe the process will start as early as April, and end as soon as mid-summer.

This highlights that financial-instability risks are possibly much closer than is commonly thought.

Why?

In practice the Fed does not want to run reserves down to their lowest comfortable level.

Powell has talked about ending QT when reserves are still abundant, but with an added buffer.

Banks will also want to keep a buffer in their reserves so they don’t run into funding issues.

But if perceived risks are rising – which we know is the case as end-of-QT forecasts are brought forward – the incentive is to increase the buffer.

If everyone does this – and everyone knows everyone else is doing it – then it’s prudent to raise your buffer a little more: if you’re going to panic, it’s best to panic first. Reserves could go from superabundant to scarce very rapidly.

Thus a linear correlation between reserves and financial conditions is not the appropriate way to judge whether the relationship is spurious or not, as Cameron argues it may well be.

In non-linear relationships it’s not about what happens through all time, but at turning points.

With reserves, there is likely to be a regime shift when they go below a certain level, where suddenly they do have a strong causal correlation with financial conditions.

That’s why QT’s end could happen rapidly once any taper starts. Cameron disagrees, giving the analogy of running while juggling tennis balls, with the juggling representing banks trading reserves with one another, and the speed of the running the pace of QT. More juggling is needed the more that reserves fall, thus it’s prudent to run slower.

In the analogy, however, there is no penalty for dropping one of the balls. If this cost is perceived to be rising, and yet you’re still being forced to run at a certain pace, i.e. QT is ongoing, then you might decide to stop juggling altogether! In other words, the funding markets would seize up, with negative repercussions for asset prices.

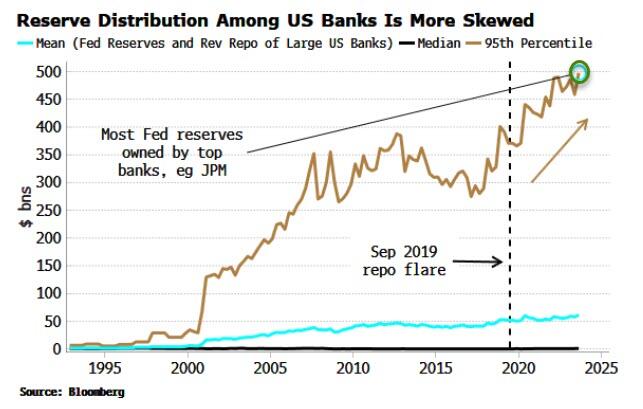

Banks with plenty of reserves will be OK, but it is the unevenness in how they are distributed that is the problem.

5% of the largest US banks own 40% of reserves, and the problem has become even more acute since the repo flare-up in 2019.

Pricing is set at the margin, and smaller banks without reserves will push up the cost of funding – a major risk to financial stability if it happens in an uncontrolled fashion.

{kind=link}

The sooner rates are cut, the sooner pressure is taken off reserves from government interest payments, which are set to balloon to as high as an astronomical $1.5 trillion this year.

A simple regression shows that that the drop in yields since November as more rate cuts were priced in could already have taken $250 billion off the government’s interest-rate bill. That eases pressure on the government to tax and borrow more, which is ultimately a boon for reserves and their velocity.

Rate cuts should also bolster banks’ balance sheets as duration positions become less underwater – reducing the risk that banks stop dealing with one another in funding markets.

The Fed may purport to believe in the separation principle, but its unexpected pivot in December without obvious economic justification hints it may not. Either way, neither does the market, hardwired to seek what works in practice, not in theory. If perceived risks are rising, then pushing for an early rate cut makes sense (especially as there is no direct way to express a view on when QT ends).

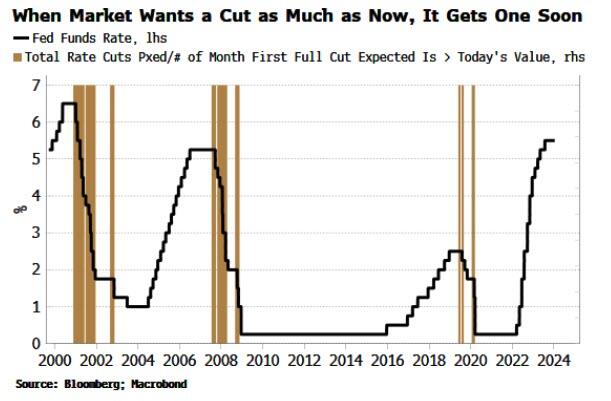

And we are now at the stage where the market has always got its way.

The chart below shows a market-based Fed easing trigger.

{kind=link}

The brown bars are the times when at least the same amount of rate cuts have been priced as there is today, and as imminently. On every occasion the Fed was already cutting rates or very close to doing so.

The Fed could, of course, decide to push back more forcefully on early rate-cut expectations (and the risk-reward for trading a March cut in any event is very poor; an April vs May Fed Funds flattener may be a better option). But the fact so much got priced so quickly when not justified by Fed-speak or the data indicates the market is perhaps conditioning on other factors. Financial stability risks from the Fed’s balance sheet and the heightened impact of Treasury funding decisions fit that bill.

The lesson of the curious case of the March cut is that anticipating the short-term interest outlook in this cycle requires acknowledging we may be in a new paradigm, where unemployment and inflation are only part of the picture.

Tyler Durden

Tue, 01/16/2024 – 14:20