Goldman Was Dumping Billions In Stocks And Other Assets As It Told Clients To Buy

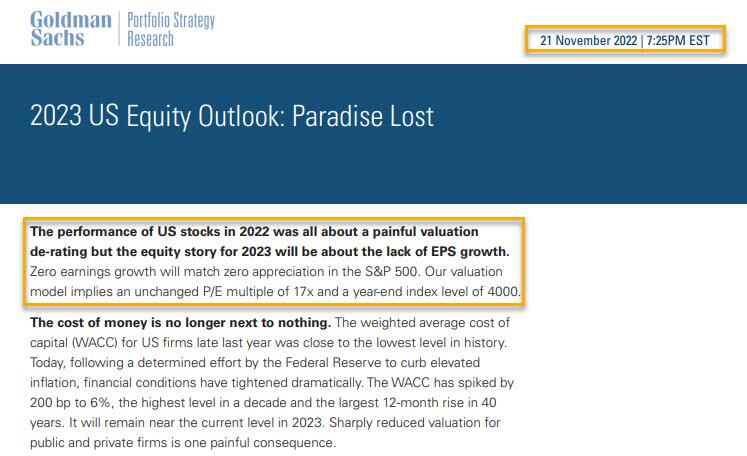

After getting his 2023 forecast catastrophically wrong in Nov 2022 when he predicted the S&P would close 2023 at only 4,000, or effectively unchanged for the year…

{kind=link}

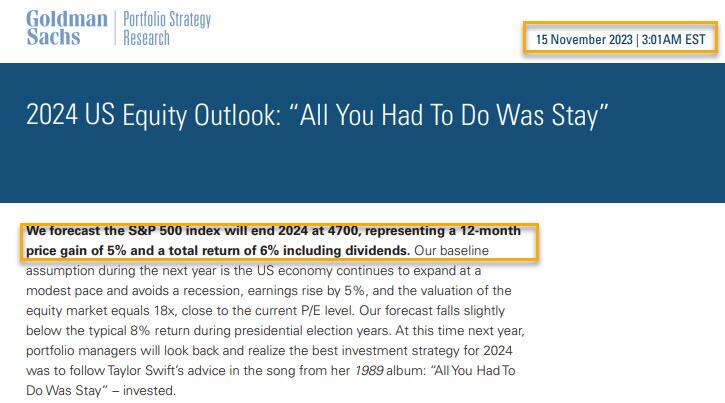

… Goldman’s chief equity strategist David Kostin scrambled to overcompensate in his next annual preview, first writing in his 2024 Equity Outlook note published in mid-November that he now expected the S&P to close at 4,700…

{kind=link}

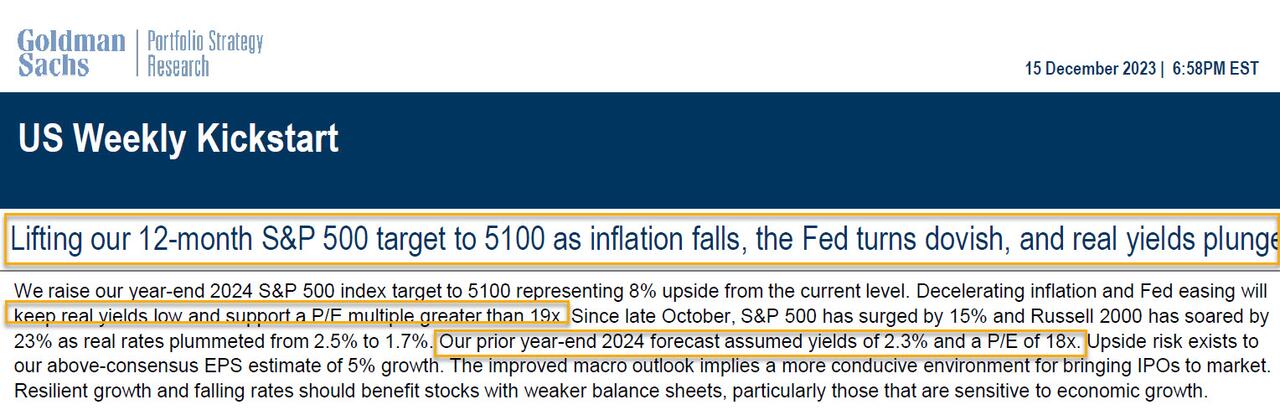

… only to change his mind exactly one month later when, in the middle of the biggest year-end meltup in decades, he revised his 2024 price target upward again this time to 5,100.

{kind=link}

While it would be easy – and correct – to be cynical and observe that all Kostin was doing was chasing both market price, andthe herd of other sellside analysts all of whom were suddenly outbulling each other like a waddle of penguins on meth, it is irrelevant what prompted Kostin to push the afterburners on his bullish take. Instead, what sparked our interest is what Goldman itself was doing during the time the bank was telling its clients to buy.

Because as we learned going through the bank’s latest quarterly investor presentation, we are confident that it will come as no surprise to regular readers (especially those who have read our previous notes on the matter such as “Goldman Quietly Sold Billions In Stocks In Q4 And 2021“, “Goldman Quietly Sells Billions In Stocks For The Third Quarter In A Row“. etc), Goldman was aggressively liquidating billionsin its “principal investments” throughout 2023.

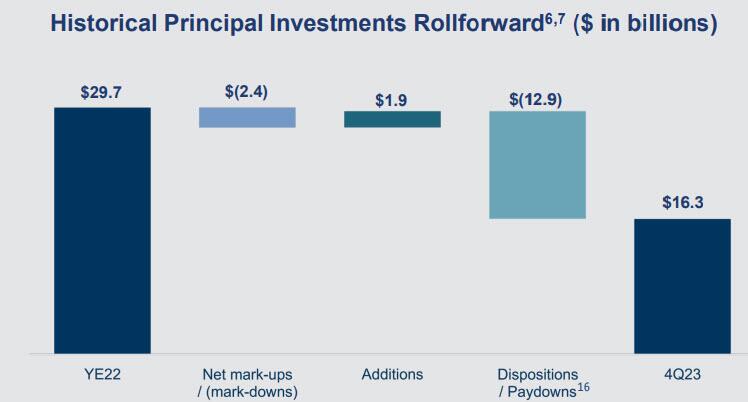

As the bank reveals in a chart on slide 16, revealing the details of its Asset & Wealth Management division, in a year when Goldman expected stocks to levitate modestly and, eventually, to soar higher, the bank was selling… and selling… and selling. Indeed, while the group, which was once better known as Goldman’s feared Prop Trading division, had “on-balance sheet alternative investments” of some $29.7 billion as of Dec 31, 2022, that number declined anywhere between $2 and $4 billion every quarter for the next four – with the bulk of sales taking place int he final quarter – before closing the year at just $16.3 billion!

{kind=link}

To be sure, while there was some changes in market values (i.e. mark-ups and mark-downs, and some modest additions), the bulk of the change was due to “dispositions”, i.e., sales, some $12.9 billion of it… and yes, all this at a time when Kostin was bullish on stocks, first tepidly, then euphorically!

{kind=link}

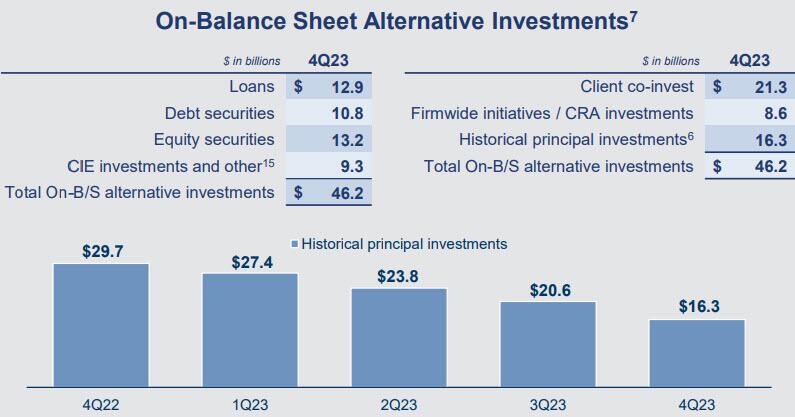

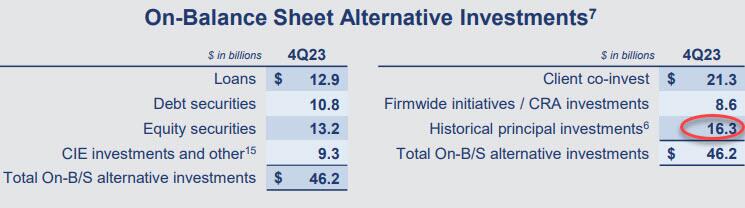

Question #2:How does this $16.3BN in principal investments fit into the bigger picture of the bank’s broader “alternative investments” portfolio? The answer: together with $21.3BN in client co-investments and $8.6BN in firmwide initiatives/CRA investments, it was a substantial portfion of the bank’s total On-balance sheet $46.2BN in alternative investments, which as shown in the next chart was comprised of loans, debt securities, equity securities and CIE Investments and other, as shown below.

{kind=link}

Question #3:what was the composition of these principal investments? What if it was all just office loans or some other toxic debt Goldman couldn’t wait to offload? The bank was kind enough to answer that question too, noting that in 2023, “historical principal investments declined by $13.4 billion to $16.3 billion and included $3.5 billion of loans, $3.6 billion of debt securities, $4.0 billion of equity securities and $5.2 billion of CIE investments and other.”

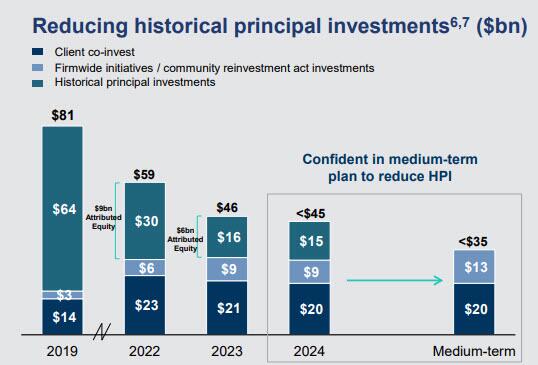

Now as an aside, none of this is a secret: we have repeatedly shown in previous years that Goldman has been gradually unwinding its principal investments business (which once upon a time would make billions quarterly on the bank’s Prop and Special Situations bets), and Goldman itself hasn’t been shy to telegraph its intention to unwind and reduce to zero its “historical principal investments“, selling billions more in various equities, debt and loans, until it is left with just low-risk (and low return) client co-investments and Community Reinvestment Act initiatives, as the following chart from today’s earnings presentation shows (more here).

{kind=link}

Still, the fact that there remains such a huge conflict of interest, where the bank still has at least another $16 billion in various legacy prop assets it has to liquidate to willing buyers (and whatever happened to the Volcker rule prohibiting banks from prop trading), including its own clients whose views on risk are molded by Goldman’s own sellside research, would surely be something that the SEC should pay close attention to… assuming of course that SEC wasn’t busy figuring out how its X/twitter account got hacked, and how Blackrock muscled the incompetent, porn-addicted agency into approving bitcoin ETFs.

In any event, the bottom line remains: throughout 2023 – and mostly in Q4 when the value of the bank’s principal investments dropped by over $4 billion, the same quarter when a suddenly “euphoric” David Kostin raised his 2024 price target first to 4,700 and then to 5,100 – Goldman was dumping billions in risk assets. And worse, Goldman’s own clients were buying anything and everything that Goldman had to sell.So the next time Goldman’s sellside research is telling you to buy stuff (not the bank’s S&T desk, those guys are actually legit which is why we focus so much more on their work), first and foremost ask: is Goldman the seller?

Appendix

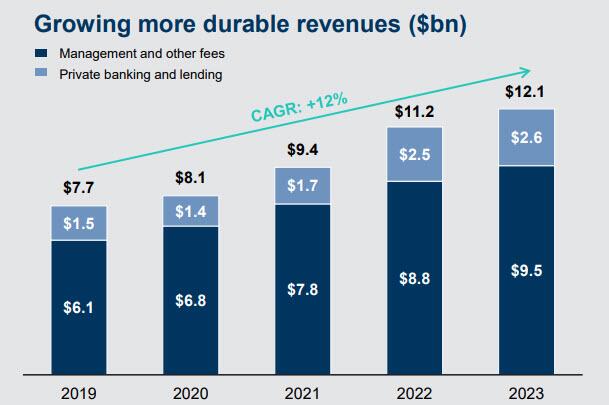

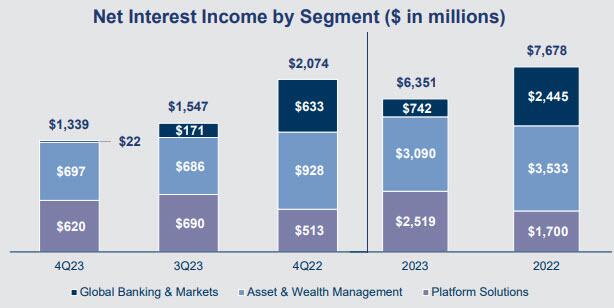

While not linked to the above, something else we found hilarious is how the bank spins the data it presents in its presentation to fit its own optimistic narrative. See if you can spot the amusing difference between these two charts both inserts in the same Q4 presentation slidebook:

First, here is a chart showing Goldman’s durable revenues. Up and to the right, just like everyone likes, right?

{kind=link}

And just a few pages later, here is the bank’s Net Interest Income, also up and to the right. Only… something is a little off. Try to spot what it is.

{kind=link}

Tyler Durden

Tue, 01/16/2024 – 15:39