American Eagles

By Michael Every of Rabobank

There are many Eagles songs to start 2024 with. Contentious US politics?‘On The Border’.The Republican Iowa caucus Trump win(though we have to wait to see how large his margin was)? Certainly not ‘New Kid in Town’.The 2024 US election?‘The Last Resort’.

Yet the market’s view of what 2024 has in store from central banks? ‘Take It Easy’. Not only do we still see pricing for over 6 Fed rate cuts this year, starting imminently, but the Wall Street Journal’s FOMC Whisperer Timiraos just ran on from comments by Logan to say: “Fed Tiptoes Toward Dialling Back Key Channel of Monetary Tightening: By slowing the pace at which its balance sheet shrinks, the central bank aims to prevent a messy disruption to the financial system.”

In other words, QT may end soon too.This will naturally lead markets to bellow ‘Take It To The Limit’ one more time on stocks in anticipation of a flip from Fed QT to QE. With the Fed’s new core services CPI measure well above target and trending higher, unemployment at record lows, and fiscal deficits and debt both at record peace-time (non-Covid) highs. Which would of course also imply a smashed US dollar, which in turn means all assets going through the roof even further.

Like the ageing, balding, fattening rock stars still squeezing themselves into embarrassingly-tight denim, leather, or spandex on stage, because neoliberal capitalism has ensured there are no young bands to see, neoliberal markets are insistent on replaying the greatest monetary policy hits of the 80s, 90s, 2000s, and 2010s. Anything but the more recent material, please!

Yet it remains to be seen if central banks will sing along. The ECB’s Holzmann couldn’t have been clearer yesterday in saying “We shouldn’t count on rate cuts at all in 2024”: then again, who listens to Germanic pop vs. US rawk ‘n’ rewl? I’ve been saying “Rate hikes plus acronyms (like QE)” for a long time: but who listens to my Tibetan throat singing about new political-economy ‘-isms’ vs. US Timiraos ‘n’ rewl? More importantly, however, the real world isn’t singing along either.

Crucially, container traffic through the Red Sea and Suez Canal continues to redirect via the overloaded ports along the far longer Cape of Good Hope route. There have been further Houthi attacks on shipping, including a missile fired directly at a US warship, and Qatar –which hosts Hamas– is now avoiding sending its LNG cargoes via Suez too: whether due to backing for or fear of the Houthis, that is just as worrying. Back to The Eagles: ‘You Can’t Hide Your LNG Eyes’.

Indeed, if it weren’t for a collapse in European industrial production reducing energy demand, and the climate-change hit Panama Canal seeing a redirection of US LNG cargoes from Asia to the EU, Europe would be shivering in more than cold right now.

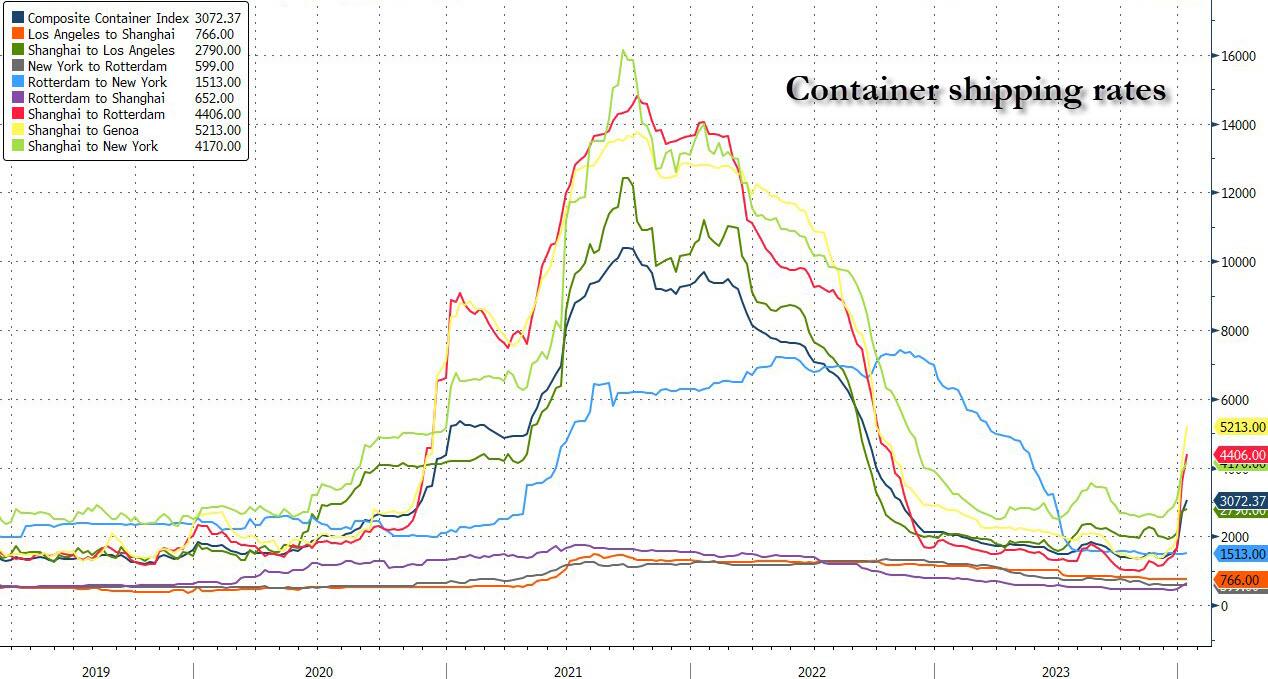

The market is overlooking this in the same way that it did the last supply-shock crisis on the view that: (i) the Fed’s Global Supply Chain Pressure Index chart is not as bad as then; (ii) the global container fleet has added supply; (iii) western demand is much weaker now; and (iv) “it will all be resolved soon.”

However: (i) Shanghai-Rotterdam spot freight rates are surging, and the longer this crisis goes on, the higher they will go; (ii) the container fleet has grown, but going round the Cape of Good Hope –if we get delays for bunkering services– will absorb that new capacity, while other chokepoints revealed in the last crisis are still there; (iii) demand is lower, but that can still mean stagflation; and (iv) there is no sign at all that this can be resolved soon. Indeed, the larger question is how it can be resolved at all, at least without things getting far worse first.

{kind=link}

First, the Israel-Hamas war is going to roll on all year according to Israel, with no clear political exit strategy to then dampen down violence; escalation to a full confrontation with Hezbollah is also worryingly close, and may be inevitable.

Second, shipping still avoiding the Suez Canal means the US Navy’s Operation Prosperity Guardian (OPG), costing $500m a month, is neither prosperous nor guarding much. Indeed, the US seems to be confused as to what it is trying to do and who it is up against.

Worryingly, the Houthis are not a powerful regional actor. They are a poor, Shiite jihadist, slave-taking, child-soldier-recruiting militiawho use starvation as a weapon, whose motto is “God is the Greatest, Death to America, Death to Israel, A Curse Upon the Jews, Victory to Islam”, whom the White House removed from the terrorist designation list in 2021 to send aid to, and now again unofficially “terrorists” in the eyes of President Biden. That they present such a challenge not just to the US but to the entire global economy is a lesson in asymmetric warfare.

Can the US speak with them? Hardly: they tried being friendlier in 2021, and it got nowhere. And while their motto might be popular at Harvard, it doesn’t leave room for policy negotiation.

Can the US deal with them? Only by seeing the regional reality in which they operate. The Houthis are not Iranian puppets – but they are funded and armed by Iran. The same Iran backing Hamas, Hezbollah, and the Shiite militias attacking the US across the Middle East; and the US consulate in Erbil, Iraq, was just hit by missile that appears to have been fired directly by Iran’s Revolutionary Guard’s Council. That’s as many in the US still day-dream about an Iran nuclear deal. (Back to The Eagles: ‘Wasted Time’.)

Notably, on 18 April 1988, President Reagan sank half of the Iranian fleet in one day in Operation Praying Mantis after an Iranian mine had struck a US warship in the Persian Gulf. The Atlantic now suggests ‘The Decatur Option’ to put an end to attacks on shipping, echoing how the US dealt with Barbary pirates in 1815: bombing Iranian targets that supply the Houthis.

However, a very understandable US fear of another draining Middle East war ahead of the 2024 election means this is very unlikely to happen. Even the recent US and UK airstrikes on Yemen had little real military effect and were mostly for (expensive) show: the Houthis, Hezbollah, and Iran have all stepped up their rhetorical threats in response.

In short, there is arguably no quick or easy resolution to this Red Sea crisis. So, ‘Desperado’, even if markets prefer to sing ‘Assets up, do-do-do-do-do-do, Assets up, do-do-do-do-do-do” to the tune of ‘Baby Shark’– or whatever the new mantra is at Davos this week.

Against that geopolitical backdrop, some might be able to join the dots to suggest where new US QE might be going, if we really are going to get it: and it likely won’t be aimed at financial assets as much as military ones, which are then aimed at other people.

Tyler Durden

Tue, 01/16/2024 – 13:00