Eroding Europe Profit Forecasts Are Risk For Stocks

By Heather Burke, Bloomberg markets live reporter and strategist

After a tepid start to the year, European stocks now face a tough earnings season amid a still-soft economic backdrop and a cautious consumer.

Earnings-per-share for the Stoxx 600 are expected to rise 6.5% in 2024, according to Bloomberg Intelligence data. Analysts have lowered consensus EPS by 2.1% in the past three months, led by materials, tech and energy. The chart below shows how profit downgrades have outpaced upgrades the past few months, even as stocks gained.

{kind=link}

European stocks’ profits partly hinge on the region’s economic growth, which looks to be picking up very slowly. Economic sentiment remains deeply negative, although improving, PMIs have contracted, and both economists and European Central Bank members are downbeat about the end of 2023. Executive Board member Isabel Schnabel said the near-term outlook looks soft, even if the worst of the downturn may be over.

While euro-area headline inflation is largely easing, margins are at risk if price pressures continue to fall. And many European companies’ profits depend on what’s happening outside the region. The Stoxx 600 only gets about 40% of its revenue from Europe, with 20% from the Asia-Pacific, according to Goldman Sachs. And China’s economic recovery has stumbled.

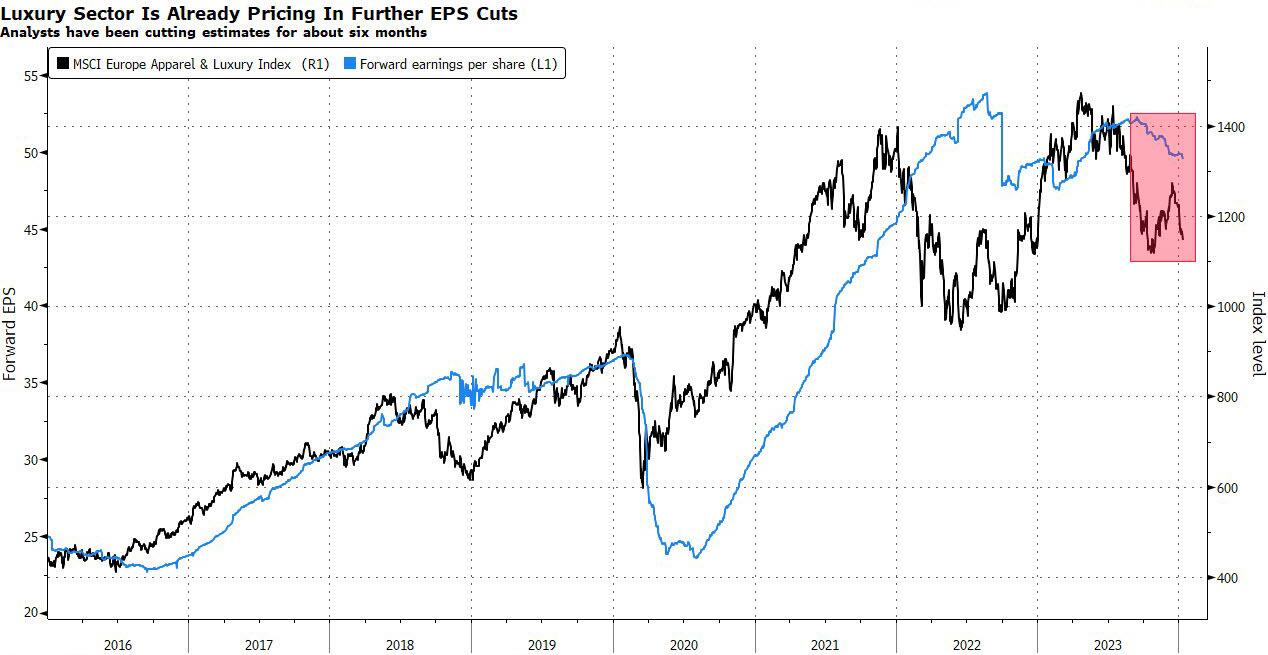

The luxury sector, often considered Europe’s version of high-growth tech, has emerged as a weak spot. Burberry dropped Friday after cutting its profit forecast. While some problems are company-specific, the warning underscores how luxury has underperformed amid slowing consumer demand.

In November, Richemont’s CEO said moderating demand was to be expected; the watchmaker reports Jan. 18. UBS had predicted a weak luxury earnings season amid softer China demand. Meanwhile, Goldman Sachs cut its 2024 forecast for global luxury growth but sees improvement in the second half. Earnings estimates have fallen in the past few months and investors have reduced exposure.

{kind=link}

German stocks, which tilt heavily toward cyclicals such as autos and industrials, could also be set for a difficult earnings season. DAX consensus index EPS fell 3.3% in the past three months, especially in autos and tech.

Autos look set for a challenging 2024 amid softer demand and competition in China. German car production is still below pre-pandemic levels; Porsche deliveries fell in China in 2023. Volkswagen plans cost cuts to boost returns at its underperforming namesake brand.

Retail, the best-performing European sector in 2023, may have a more subdued year. While Marks & Spencer’s holiday sales beat estimates, the department store chain didn’t raise its profit guidance and said the broader outlook for economic growth is “uncertain, with consumer and geopolitical risks;” shares fell. JD Sports slashed its profit forecast in part on cautious consumer spending.

Fresh headwinds could pressure earnings further into 2024. Shipping disruptions in the Red Sea may spur profit warnings from companies if the surge in container rates and supply-chain issues persist, according to Lazard Freres. Tesco said such disruptions could drive inflation on some consumer goods.

To be sure, companies can easily beat a low bar. Weakness in the Chinese and European economies may already be priced in to estimates. Other issues, such as inflation and central bank interest rate cuts, could overtake earnings.

But Burberry’s profit warning is unlikely to be isolated as the 4Q earnings season kicks off, easily derailing European stocks’ end-of-2023 rally.

Tyler Durden

Mon, 01/15/2024 – 08:45