Yen Plunges After Japan Wage-Growth Collapses, Crushing Hope For BOJ Hikes

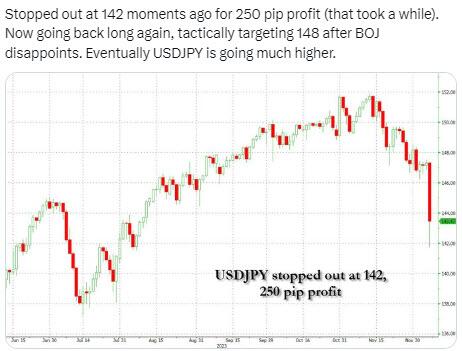

ZH premium subscribers who have access to our private twitter feed, are aware that one of our favorite trades of 2023 (besides the blockbuster USDTRY long which made our year in one trade) was to trade the USDJPY, which we first went long (successfully) at the start of the year, then shorted in August (also successfully), before once again turning long at the start of December when it dipped to 142 on the thesis that consensus was dead wrong in expecting the BOJ to normalize monetary policy just as the rest of the world was set to ease.

{kind=link}

And so far so good, because at a time when the dead wrong echo chamber of momentum chasing Wall Street penguins was recommending shorting the USDJPY to the 130s because the “BOJ would hike rates as soon as December, January, well, maybe some time in 2024… and if not 2024, then 2025… or later” (which we were confident would nothappen with the Fed and ECB both set to cut rates), overnight the yen tumbled after Japan’s labor ministry said that in November, headline wage growth for Japanese workers slowed sharply, effectively crushing any hope that the BOJ would hike rates at a time when Japan’s all important wage growth is once again tumbling. As a reminder, for the past decade the Bank of Japan has been seeking evidence of a virtuous cycle linking pay hikes to price increases as a prerequisite for normalizing monetary policy, which is why wage growth – or the lack thereof – has been so important.

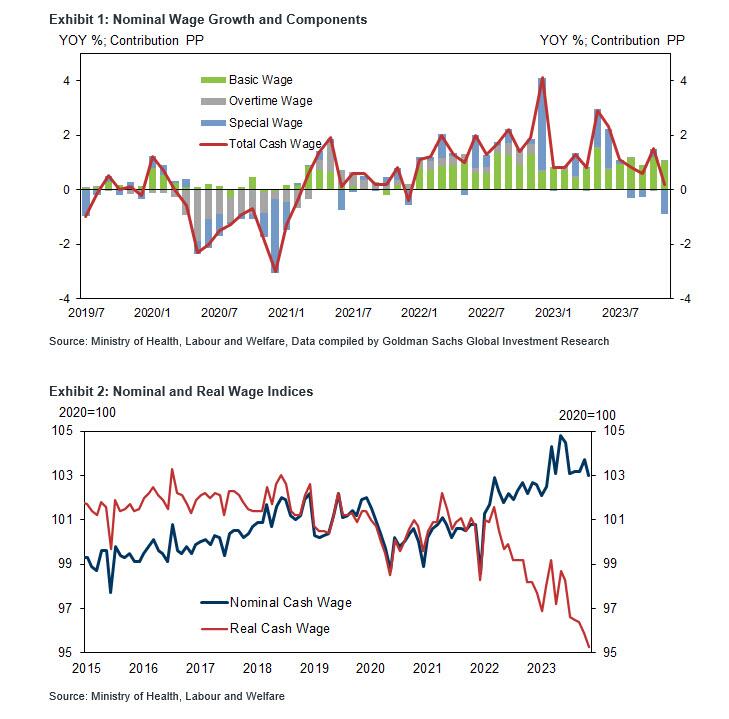

As shown in the chart below, nominal cash earnings for workers rose only 0.2% from the previous year, decelerating sharply from a 1.5% increase in October. Economists had expected the pace to hold steady. Here are the key numbers:

Nominal cash wage (yoy): November: +0.2%, October: +1.5%

On a seasonally adjusted basis (mom), nominal wage growth declined by -0.7% in November (October: +0.5%).

Basic wage (yoy): November: +1.2%, October: +1.3%

Part-timers’ basic wage per hour (yoy): November: +4.6%, October: +3.8%

Overtime wage (yoy): November: +0.9%, October: -0.7%

Special wage (yoy): November: -13.2%, October: +13.7%

Meanwhile, real wages crashed 3%, the biggest drop on record, and much deeper than the consensus call for a 2% drop, as well as a drop from October’s -2.3%.

{kind=link}

BOJ Governor Kazuo Ueda has been monitoring wage trends for signs there will be enough momentum for the bank to achieve its goal of 2% inflation on a sustainable basis. Clearly, the latest wage growth data, especially the nominal series, confirms that the air is rapidly exiting the balloon, and at this rate Japan may be forced to do even more easing and more QE by year end, steamrolling all those who expect the yen to jump. Ironically, as Bloomberg adds, “while Wednesday’s figures will back the rationale for keeping policy settings ultra-easy this month, they aren’t likely to deter economists from predicting a rate hike in coming months.” Which is to be expected; economists expected the USDJPY to explode even higher above 150 for much of late 2023, only to flip their script and now see it tumbling. They have been dead wrong on both occasions.

{kind=link}

That said, the BOJ is looking ahead to the state of play in annual wage negotiations expected to culminate in March. While Japan’s largest labor union federation is urging companies to raise wages by at least 5% in principle, the recent data suggests that any pressure for companies to hike wages is now gone.

Ueda told NHK late last month that it would be possible for authorities to make some decisions even if they don’t have the full results of pay discussions from smaller firms, which may not be available until summer. That remark spurred speculation that the likely timing of a BOJ hike would be the April monetary policy meeting. BOJ authorities next convene in two weeks at a gathering that concludes on Jan. 23, where in addition to setting policy they’ll release updated outlooks for prices and growth.

“The current situation is that wages haven’t caught up with prices,” said Harumi Taguchi, principal economist at S&P Global Market Intelligence. “Given the strong impacts of the base effect from the previous year and the weakness in some sectors, I don’t believe we are in a virtuous cycle yet.” She added that she still foresees an exit from negative rates in April at the earliest.

And now, judging by the latest labor data, Japan’s long overdue exit from negative may happen never… at the earliest.

Tyler Durden

Wed, 01/10/2024 – 09:40