Logical Bullish View On US Stocks Is Flawed

Authored by Tatiana Darie, Bloomberg,

It’s valid to forecast that stocks will rally yet again in 2024. It’s also a deeply vulnerable view.

When formulating our S&P 500 outlook for 2024, the fraught debate among the Markets Live team has likely been echoed in trading rooms across the industry. A lot of the conflict ultimately boils down to the approach of a trader versus an investor.Sure, stocks can keep gaining from these already lofty levels. However, history suggests that the risk-reward to being bullish is poor at these valuations at this point in the cycle.

An optimistic stance may be the most logical base case, and that’s why Wall Street is confident.A good number of strategists are calling for the S&P 500 to top 5,000 this year, or even reach 6,000 by 2025. The MLIV team overall leans even more bullish than the Street median forecast of 4,850. And my colleagues observe that the bearish view hinges on “something” breaking, which is undermined by the principle of Occam’s Razor.

The issue is that there are quite a few “somethings” out there and the negative consequences will be large if any of them come to pass.

The clash in views is essentially because there’s a great probability of gaining a little versus the minority chance of losing an awful lot.

So I will lay out the bull case in earnest — and then also the key reasons why it could all go terribly wrong.

Here goes:

The Federal Reserve will pull off an elusive soft landing as powerful disinflationary impulses cause workers to reduce wage demands even though the labor market holds up just fine overall.

This is all aided by aggressive pre-emptive interest rate cuts, perfectly calibrated to restrain inflation even while easing economic stress.

Consumers, powered by positive real incomes, never fully erode their excess savings and hence equity earnings will return to double-digit growth after dropping an estimated 3% last year.

Buoyant liquidity conditions help further,and Fed Chair Jay Powell’s December pivot has validated an extraordinary loosening of financial conditions, which should be a boon to the economy.

Inflation has cooled significantly and core CPI has dropped below 3% on a six-month annualized basis.

The incredible fiscal tailwind won’t dissipate in an election yearand there’s the upside risk that artificial intelligence is transformative for US productivity.

There’s a tremendous amount of cash on the sidelines.

After a year where tech drove most of the gains, there are plenty of other pockets of the market for investors to jump on in 2024 and round out the rally. For example, small caps and the equal-weighted counterpart of the S&P 500 are trading at steep discounts relative to the main benchmark.

It’s a compelling picture.

However, hear me out:

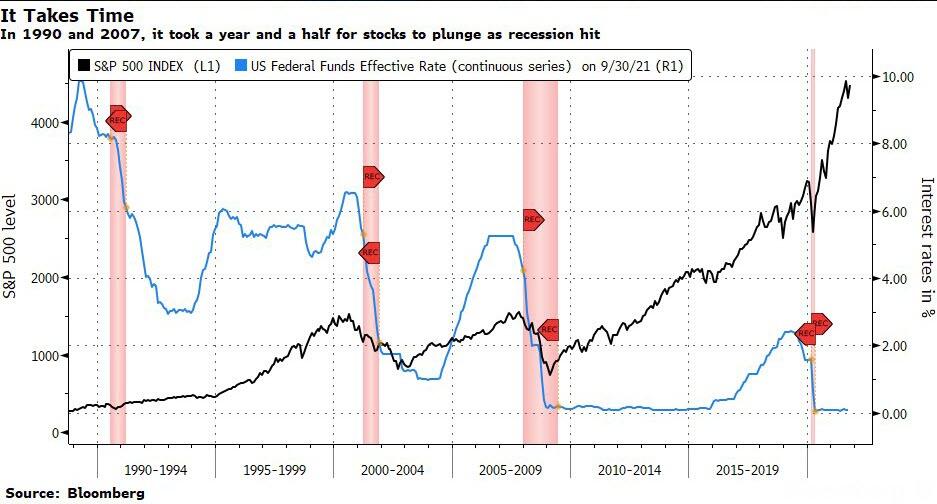

For a start, widespread economic complacency just isn’t justified once you consider the gloomy precedents on recession indicators.

The economy will eventually stall – if not slump hard – once higher borrowing costs bite households and corporates, which have largely been shielded from this tightening cycle by refinancing during the pandemic.

In fact, Bloomberg Economics argues that the US may already be in a recession as cracks in the labor market are widening despite strong payrolls numbers.

And history is very clear that economic contractions tend to hurt the stock market very badly indeed.

If a slowdown is averted, the Fed will keep rates elevated as the disinflation impulse fades amid robust economic activity.

The lagged effects of monetary policy will eventually matter for stocks – it’s not unprecedented for equities to start cratering more than a year after rates peak.

{kind=link}

And the risk is greatly exacerbated by valuations.

If the Fed were to cut rates now, or if the S&P 500 holds on to current levels when the central bank starts to move, it would be the second-most expensive stock market at the policy turn in almost 60 years. Small caps and the equal-weight benchmark may seem compelling alternatives at first glance but, outside of the Magnificent Seven, corporate America is mired in a profits contraction.

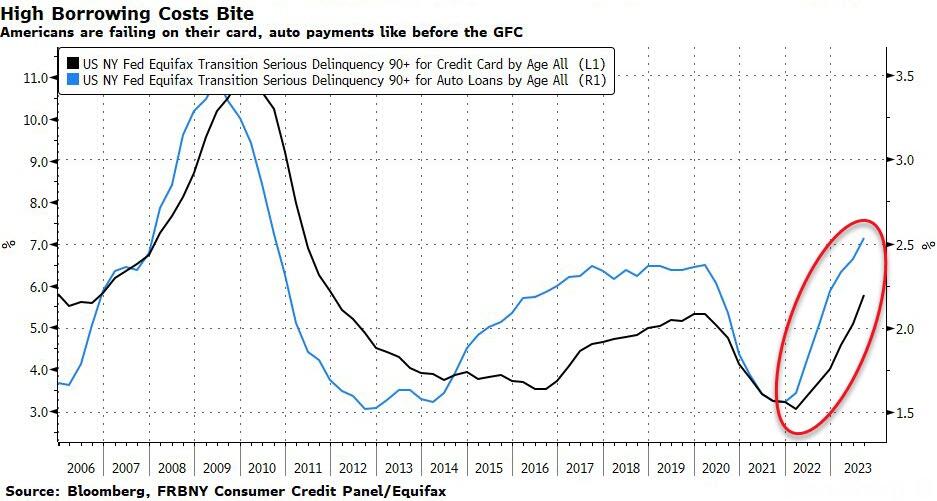

Meanwhile, default rates have been rising and refinancing pressures for vulnerable borrowers are building. Did someone say credit crunch?

To protect cash flows, companies will cut investments and turn to layoffs, sending the unemployment rate higher.

This is at a time when there’s clear evidence that pandemic savings are draining.

Increasingly more Americans are failing on important payments, like auto and credit card debt.

Consumer resilience has been mistaken for consumer invincibilityand the belated realization of that misapprehension will coincide with a severe reduction in profits.

{kind=link}

Hands up that I’ve been incorrectly bearish for a long time.

Like many, I underestimated the resilience of the US economy, while the AI-triggered euphoria was an outcome few anticipated. But history validates the idea that poor fundamentals will eventually matter.

Now you have both sides of the argument, I’ll leave you to decide which stance has greater merit – but if you’ve finished reading this piece marginally more nervous about US stocks than when you started, I’ll take that as a win.

Tyler Durden

Tue, 01/09/2024 – 08:35