How To Navigate The Fed’s New Paradigm Shift

Authored by Simon White, Bloomberg macro strategist,

Will it come in March? Or the summer? When the Federal Reserve makes its first rate cut and when it tapers or ends quantitative tightening will in the first instance be a function of reserves, not the economy.It is through this prism that the Fed’s dovish conversion in December makes sense, and gives a practical framework for understanding its new de facto reaction function.

Liquidity is everything in markets.

At the base of the liquidity pyramid are central-bank reserves.

These have always been key to understanding market functioning, but in the post-GFC regime of many central banks their volume, velocity and the variation in their ownership now play a pivotal role in driving market dynamics.

To put it succinctly, the primary binding constraint on the Fed this year – and thus a key driver of the bank’s decision to pivot and when it cuts rates – is reserves.These are the frontline defense against a sharp drop in risk assets, dysfunctional funding markets, and thus a hard landing.

A cut in rates therefore need not require a significant worsening in the economy, leaving a March rate reduction on the table. With -18 bps currently priced in for that month, the risk-reward is not currently attractive, but at around -7 bps or more that calculus changes.

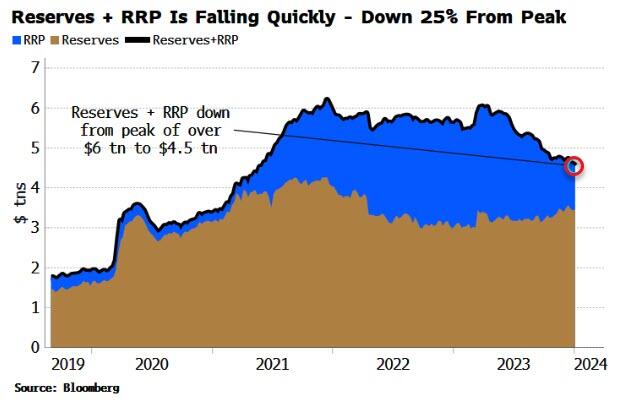

The liquidity backdrop for most of 2023 was benign as the Treasury skewed issuance towards bills which were scooped up by money market funds using idle liquidity parked at the Fed’s reverse repo facility (RRP).

But the RRP is falling rapidly and, unchecked, the liquidity environment this year is set to become much more hostile for risk assets and the economy.

{kind=link}

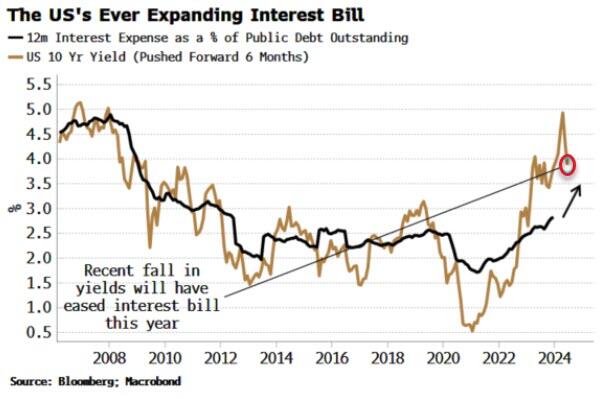

Further headwinds for liquidity this year are already baked in.As discussed last month, the government’s ballooning interest rate bill will become an increasing suck on reserves and their velocity.

{kind=link}

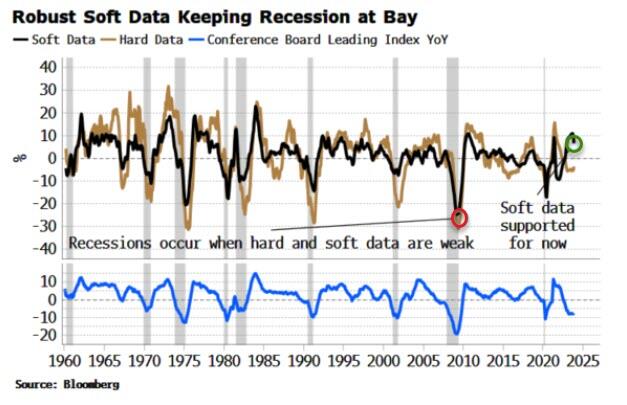

A more malign liquidity backdrop would endanger asset prices, and risks the formation of a negative feedback loop with the economy. Recessions occur when these feedback loops cascade, with falling markets denting economic confidence, and weakening economic data in turn pushing asset prices lower.

Currently still-robust soft (market and survey) data is countervailing weak but stable hard (economic) data. If the Fed can keep soft data aloft by supporting reserves, it can try to prevent a negative feedback loop from developing and delay the recession.

{kind=link}

One key way to do this is by mitigating headwinds from the government’s rising interest bill.The drop in the ten-year yield since the Fed’s pivot already translates into a significant saving for the US Treasury in bond-coupon payments. In numbers, the ~50 bps drop in the 10y since November translates into over $250 billion lower interest costs for the government, based on a simple regression. This will mean less stress on reserves.

The December pivot begins to make more sense viewed through this lens, and strongly indicates the Fed’s implicit primary reaction function is based on reserves, with inflation and employment secondary considerations.

If this supposition is correct, it means the Fed is deciding policy on variables that lead and not – as is usual – ones that heavily lag.

Investors should thus be more focused on reserves for gauging when the Fed cuts rates and when it tapers or ends QT, with the economy only a secondary driver (even though data releases will continue to influence market expectations).

Specifically, reserves’ volume, velocity and the variation in their ownership are key to monitor. As the RRP gets closer to zero, the total volume of reserves in the system will become a greater concern.Velocity will drop the more interest the government pays, as bank deposits are used to make tax payments, which in turn are used to pay interest. As these interest payments filter through the system, they are more likely to be held by those with a lower propensity to spend.

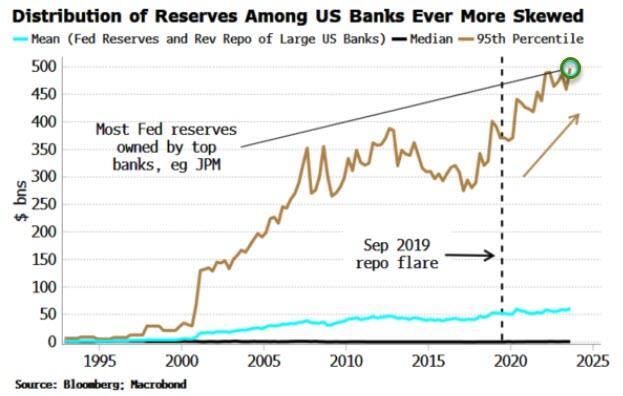

Then there is the variation in reserve ownership.

The distribution of ownership resembles a power law, with most of the reserves held by only a very few banks (with JP Morgan the largest holder). This likely played an important part in the repo funding crisis in September 2019, which struck even though there were still ~$2 trillion reserves in the system.

That skew in ownership is even more extreme now, with the top 5% largest US banks owning almost 40% of reserves.

{kind=link}

Thus even though reserves and the RRP are ~$4.5 trillion today, the Fed has begun to discuss the slowing of QT. It was mentioned at its December meeting, and then again in comments on Saturday from Dallas Fed president Lorie Logan, who explicitly referenced the distribution problem, stating individual banks can approach scarcity before the system as a whole. Several banks have mooted summer or as early as April for when the Fed starts to taper or end QT.

This imputed switch in focus to reserves is a big gamble for the Fed, as it assumes inflation will continue to moderate this year back towards the 2% target. But there’s an increasing litany of reasons why that might not happen, with, to name a only a few, supply constraints worsening again, leading indicators for wages climbing, and a still-large fiscal deficit.

In this paradigm of increasing fiscal dominance – where government borrowing and spending decisions overwhelm monetary policy – central-bank independence has been eaten away at, and instead has led to a form of “reserve dominance”, with decisions on rate cuts and QT – as well as the evolution of markets, the economy and Treasury funding – heavily intertwined.

Tyler Durden

Tue, 01/09/2024 – 14:05