No Smoking Gun Yet To Justify Magnitude Of Fed Rate-Cuts

Authored by Simon White, Bloomberg macro strategist,

US data from last week were not enough, from the perspective of the economy, to endorse the amount of rate cuts from the Federal Reserve expected by the market.

Payrolls and the jobs data released last week demonstrated why the market – and the Fed – shouldn’t take it too seriously as a real-time snapshot of the labor market.

On the surface, the data was solid next to expectations, but if you go digging you will always find elements to back up a bullish or bearish case.

A more positive interpretation came from the headline data versus what was expected, while the negative view would point out that government played a big part in the rise of payrolls.

Moreover total downward revisions for 2023 are 443,000 (so far – payrolls is typically revised up to two years after the fact).

Either way, it really is not a good reflection of where the labor market is today. Nonetheless, traders love volatility, so it will continue to have market impact. In that case, it makes sense to pay more attention to the more leading aspects of the employment data.

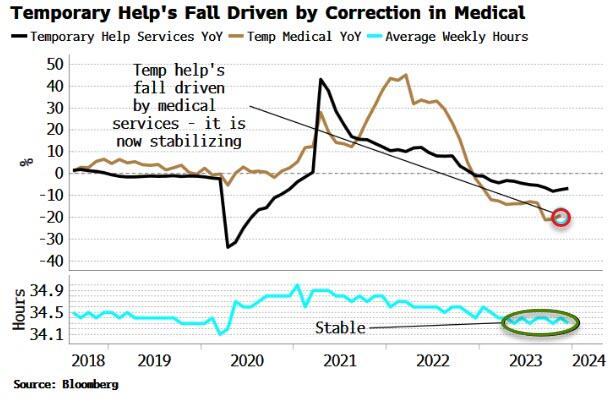

Temporary help services tends to lead the labor market as employers are more likely to hire and fire these people first.Temp help has been contracting since late 2022 but, as I pointed out on Friday, the drop was largely a function of temp help in medical services, and temp medical services is now stabilizing. Average weekly hours worked, also a leading indicator for the labor market, remained at the stable level it has been at for most of the last year.

{kind=link}

Overall, the message from the data is of a jobs market that is slowing, but not at an accelerating rate.

That on its own (nor the weaker-than-expected ISM services data on Friday) is not enough to justify the size of the Fed cuts expected by the market (from an economic perspective, however after the bank’s December pivot, there’s good chance its reaction function may have changed).

But higher rates will increasingly bite as the year goes on, increasing the odds of a recession.

{kind=link}

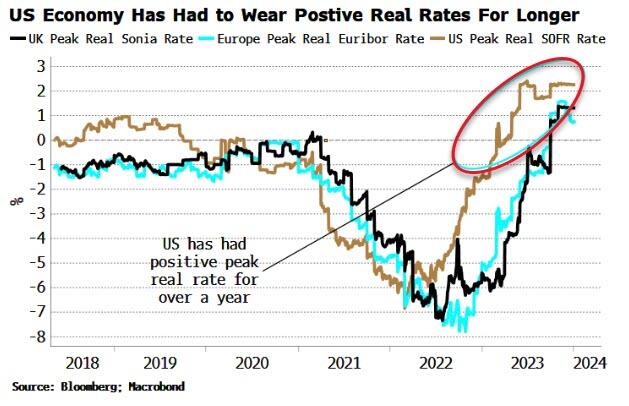

As the chart above shows, the US’s peak real rate has been positive from early last year, considerably longer than in Europe and the UK.

Tyler Durden

Mon, 01/08/2024 – 08:30