Treasuries Face Further Downside Barring A Jobs Report Shock

By Ven Ram, Bloomberg Markets Live reporter and strategist

Unless we get a huge downside surprise from today’s jobs data, Treasuries will extend the losseswe have seen so far this week as the markets correct after their year-end exuberance.

Treasury two-year yields slumped some 80 basis points last quarter, a phenomenal move not usually seen except during crises times. Indeed, we haven’t seen that scale of move outside the financial crisis and, more recently, during the first wave of the pandemic.

In rallying too fast and too far, the markets were positioned as though the Fed would cut rates imminently, a notion that is now being challenged.

The correction we have seen so far has been rather mild, meaning there is more to come, with the jobs data providing another excuse for yields to head higher.

The headline number is forecast to show another decent print, with some 175k jobs being added in December. It matters little from the Fed’s perspective if the number bobs around that estimate so long as employers are still expanding their payrolls.

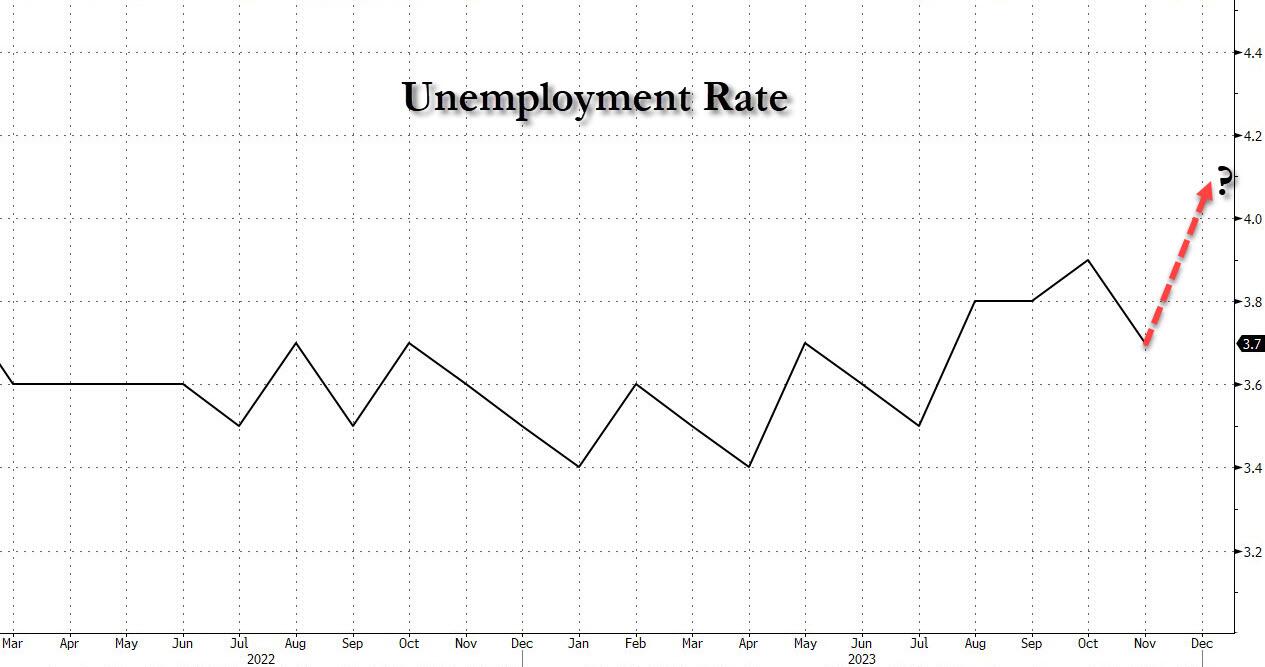

It is far more significant what the jobless rate does, and so far in this cycle, we have seen that number just move feebly around the expected number of 3.8%.

Given how strong the expansion has been since the pandemic, we need a number higher than 4% to clear the market — a state where demand and supply are in equilibrium.

{kind=link}

Sticky wage inflation also matters a whole lot and then some in today’s numbers.

Employees’ average hourly earnings is forecast to have slowed by a notch to 3.9% from a year earlier.

Even though a lower number would be welcomed by the Fed, an outcome that is in line with the median estimate would be incompatible with its inflation target.

Unless we see a materially higher-than-forecast jobless rate or a much weaker-than-expected hourly earnings number, Treasuries will extend their losses.

Tyler Durden

Fri, 01/05/2024 – 07:45