The 10Y Yield Levels To Watch For After Payrolls

Authored by Simon White, Bloomberg macro strategist,

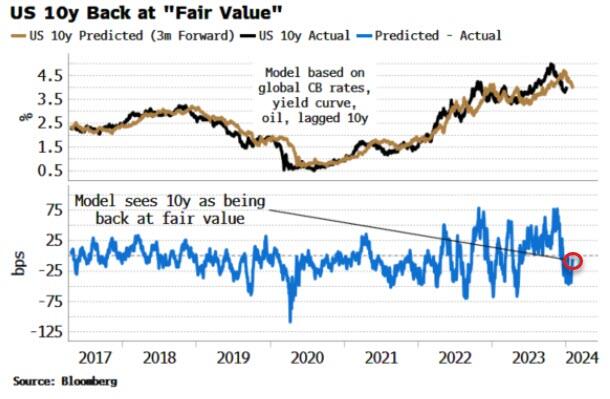

Despite leading data pointing to a positive skew for today’s jobs numbers, yields are back towards their “fair value,” meaning it would likely take a big miss in payrolls or unemployment to see a significant move higher.

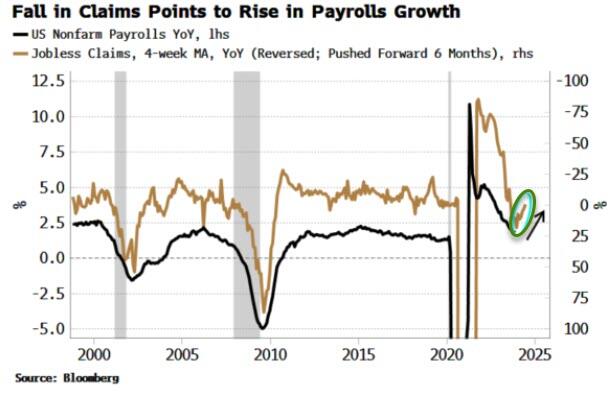

Recent labor-related data such as ADP and the employment component of the manufacturing ISM surprised to the upside, but it is unemployment claims that has the strongest leading relationship with payrolls.

The recent inflection lower in claims (inverted in the chart below) inversely leads payrolls growth by about three-to-six months.

{kind=link}

The annual growth in payrolls has been steadily falling, but the recent move in claims suggests at least a short-to-medium term bounce, which if it manifests should soon be reflected in the monthly payrolls numbers.

This would further challenge the five-plus rate cuts priced in for this year, and be supportive for longer-term yields. Nonetheless, after the assertive bond rally prompted by the Federal Reserve’s unexpected dovish backflip in December, bonds are back to trading to close to fair value.

This is based on a model for US 10-year yields which includes global central bank rates, the yield curve, oil prices and the lagged value of the 10-year yield.

The model initially had yields ~50 bps too low in the wake of the Fed’s pivot, but with the 10-year back to ~4.04%, that is very close to the model’s estimate of fair value.

{kind=link}

Stronger-than-expected jobs or earnings data today would likely prompt bond selling. This tallies with Ian Lyngen and Ben Jeffery of BMO’s payrolls survey of bond-market participants, which sees a bias to selling (if the market trades higher or lower after the data, more than average plan to sell).

However, if yields are close to some approximation of fair value, it could take significantly stronger or weaker data than expected to sustainably move the 10-year away from ~4%.

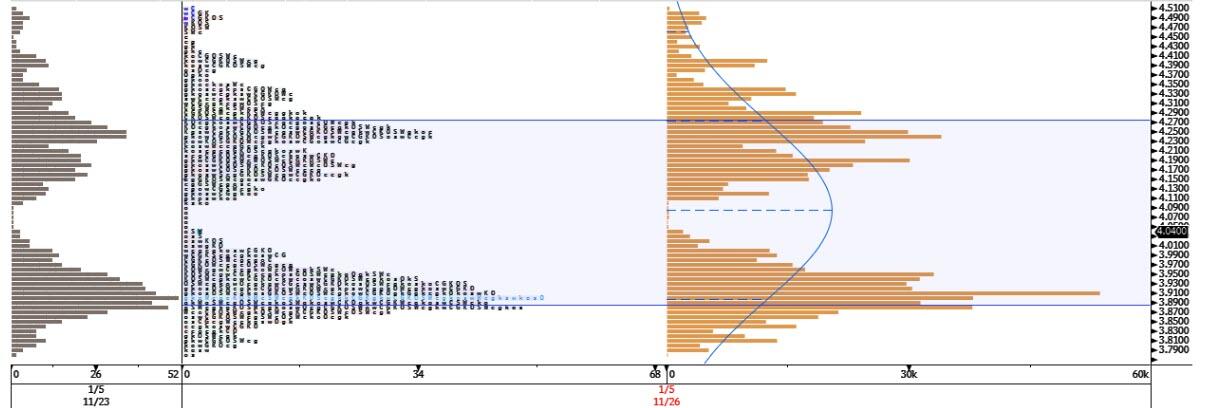

The market picture (MKTP on the terminal) gives another perspective. The diagram below (click to enlarge) shows the 10-year over the last 30 days. The blue bars show where it has traded most, with the two bulges around 3.90% and 4.20/4.25%. The thinking behind market picture is that markets tend to settle around where the bulges are, and not where the blue bars are smallest.

That would mean if the market can trade through 4.10%, then the next stop could be 4.20/4.25%. Or a lower move could see it settle back towards ~3.90%.

{kind=link}

Additionally, Goldman’s forecast reaction matrix for stocks is as follows:

>250k S&P sells off at least 150bps

200k – 250k S&P sells off 75 – 150bps

150k – 200 S&P + / – 50bps

50k – 150k S&P rallies 50 – 100 bps

That’s the theory anyway. Let’s see what January’s job jamboree actually brings.

Tyler Durden

Fri, 01/05/2024 – 08:25