And The Rest Is… ?

By Stefan Koopman, Senior Macro Strategist at Rabobank

It is a new year, the P&L’s are back at zero, and the financial punditocracy is once again invited to identify the risks in store for 2024. However, after a year in which most strategists were proven wrong, many are licking their wounds and only few are daring to make bold predictions.The consensus seems to be just a simple extrapolation of recent trends: yes, some slowdown in global growth, but no major recessions; yes, some pockets of stress here and there, but no macro-credit events; yes, some inflation hiccups, but an underlying trend of relatively pain-free disinflation, and, yes, a dovish shift by the central banks, so please, please buy those assets we’re selling.

While the Global Daily often highlights the global economy’s structural and intractable challenges, the new year does bring grounds for modest optimism. After all, the US avoided a recession and Europe probably experienced only a mild one in 2023. And inflation has not only confounded economists on the way up, but also on the way down, especially in core and services metrics. Moreover, labor markets held resilient through it all. These developments prompted central banks to pause tightening, and if markets dictate, rate cuts may soon follow. Of course, it is tempting for us strategists to balk at the foolishness of the crowd, but potential outcomes last year seemed a lot darker than this.

That said, we also believe that 2024 is likely to serve as a reminder that some of last years’ ‘once-in-a-lifetime’ events are not as rare as portrayed.The global security order is crumbling, with Iran projecting its power in the waters off Yemen and the Israeli strike in Lebanon as the two latest examples. Supply curves of commodities, inputs, intermediates, and final goods remains much more volatile than one would like. Furthermore, Western labor markets will remain structurally tight as demographic shifts, such as aging or outright population decline, accelerate, while increasing immigration is clearly not the panacea once thought. Lastly, but not least importantly, climate change may be progressing even faster than anticipated. These factors will have a greater impact on medium-term growth and inflation (and, therefore, on central bank rate decisions) than they have had for the past few decades.

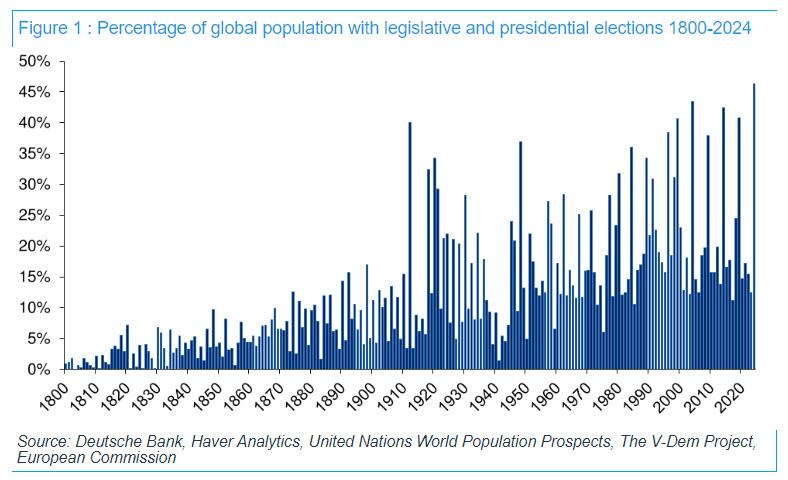

The year 2024 will also witness a global contest between democracy and autocracy, as countries that account for half of the world’s population go to the polls. This “biggest election year ever” kicks off with Bangladesh this Sunday, but the spotlight has already turned to Taiwan’s presidential vote on January 13. That election comes amid particularly tense Taiwan-China relations, with President Biden pledging to protect Taiwan should Xi’s vows for ”reunification” actually be a euphemism for “invasion”. President Biden will of course also face his own challenge from his predecessor Trump, who is seeking to return to the White House in an election that will have global implications, especially for the US-China rivalry in the Indo-Pacific. And on that note, what about the elections in Pakistan, India, Iran, or Indonesia? Or the numerous elections in Africa, where foreign powers are again competing for influence on the continent, with the United States and its Western allies trying to counter Russia’s and China’s economic and security ties.

{kind=link}

Europe will also undergo several political transitions in 2024, as some of its key leaders and parties face uncertain futures. The UK’s Tories look set to lose their long-held majority to the opposition Labour Party, as the public grows dissatisfied with the economy, the countless scandals, and the crisis in the National Health Service. Meanwhile, the Tories’ pet project Brexit has visibly downgraded the country’s standing in international relations and trade. Even though a Labour government will seek to align more closely with the European Union on a variety of levels and topics, don’t count on any big formal commitments.

The European Parliament will hold elections of its own in June. The polls suggest here that the far-right Identity and Democracy group, which includes Germany’s Alternative für Deutschland, France’s Rassemblement National and Italy’s Lega, will make significant gains. If Trump also returns to power in the US, this could again strain the transatlantic relations that have started to improve under Biden. It will certainly hamper EU-US cooperation on the war in Ukraine.

Speaking of which, the Russian presidential election may be the one with the most predictable outcome, but will still be worth watching. While Putin is set to win another term in March, the vote breakdown may reveal the level of his support and whether the Russian public still backs his war. Meanwhile, in Ukraine, it is unclear if the planned 2024 presidential vote will take place while the country is under martial law, though the current leader Volodymyr Zelenskyy has said he will run for another term.

So, rate cuts in 2024? Well, probably. The rest, however, is politics.

Tyler Durden

Wed, 01/03/2024 – 09:25