Powell’s Pivot Adds $20 Trillion To Global Debt/Equity Markets In 2023; ‘Fiat Alternatives’ Fly

Global bond and stock markets added almost $20 trillion in capitalization during 2023…and all of that gain came in the last two months of the year after it had tested unchanged on Oct 28th! The gains were dominated by global stocks (which added $13.3TN) while global bonds rose by $6.1TN…

{kind=link}

Source: Bloomberg

Nasdaq soared to its best year since the peak of the dotcom bubble in 1999 (and the rest of the US major equity market indices all rallied).

{kind=link}

Source: Bloomberg

Bonds ended higher in price (lower in yield) on the year. Gold up, dollar down, oil down, NatGas collapsed as The Fed shocked the world, suddenly flipping from uber-hawk to full-dove-tard…

{kind=link}

But, but, but, The Fed is apolitical?

{kind=link}

{kind=link}

And they did all that with ‘hard’ economic data unchanged in 2023 – no real economic progress – as only ‘soft’ data (hopes and dreams) provided support for ‘goldilocks’ narratives…

{kind=link}

Source: Bloomberg

But, 2023 was dominated by a few themes:

The Magnificent 7 stocks dominated the price action and outsized index gains in 2023. Investors preferred the ‘safe haven’ of these mega-cap tech names over longer-duration profit-less tech… until The Fed unleashed hell at the start of November and everything exploded higher…

{kind=link}

Source: Bloomberg

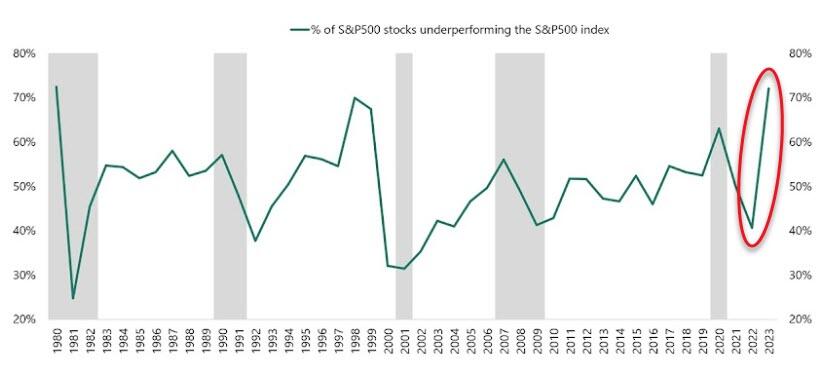

Which left a record 72% of stocks in the S&P 500 have under-performed the index this year

{kind=link}

Source: Bloomberg

AI – the apparent benefits of AI know no bounds when it comes to investment as Goldman’s basket of AI stocks soared over 90% this year (while businesses ‘at risk’ of AI’s impact rose 17% – helped by the everything rally in the last two months)…

{kind=link}

Source: Bloomberg

Anti-Obesity Drugs – losing weight the easy way appealed to investors in 2023 as the GLP-1 analogs sparked a surge in biotech/pharma (and hurt food/beer stocks)…

{kind=link}

Source: Bloomberg

Banks – SVB’s collapse in March sparked an exodus of deposits and demand for Fed bailouts. Regional bank stocks ended the year down just 8% having bounced back from being down around 40% in May (despite record usage of the Fed’s bailout facility)…

{kind=link}

Source: Bloomberg

Meme Stocks – Retail favorites had a wild year but ended up 25% in 2023, the best year since 2020’s chaos, thanks again to the last two months of panic-buying, dash-for-trash trading after The Fed folded…

{kind=link}

Source: Bloomberg

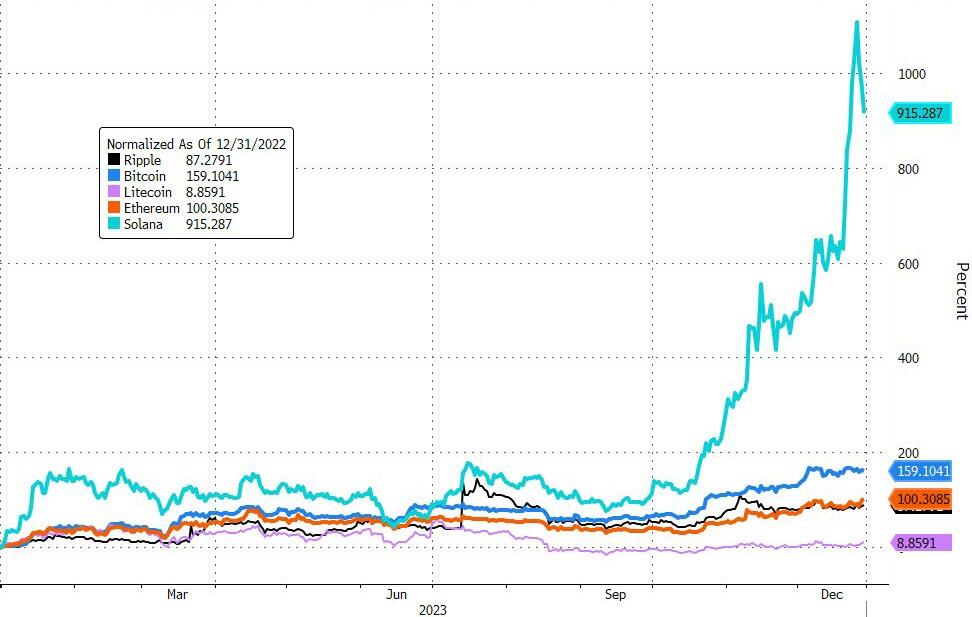

Cryptos – 2023 was a huge comeback year after 2022’s ‘existential threat’ moments from FTX to TerraUSD and so on. Of the larger coins, Solana massively outperformed – up around 1000% on the year – but bitcoin (+160%) and ethereum (+100%) also had big years…

{kind=link}

Source: Bloomberg

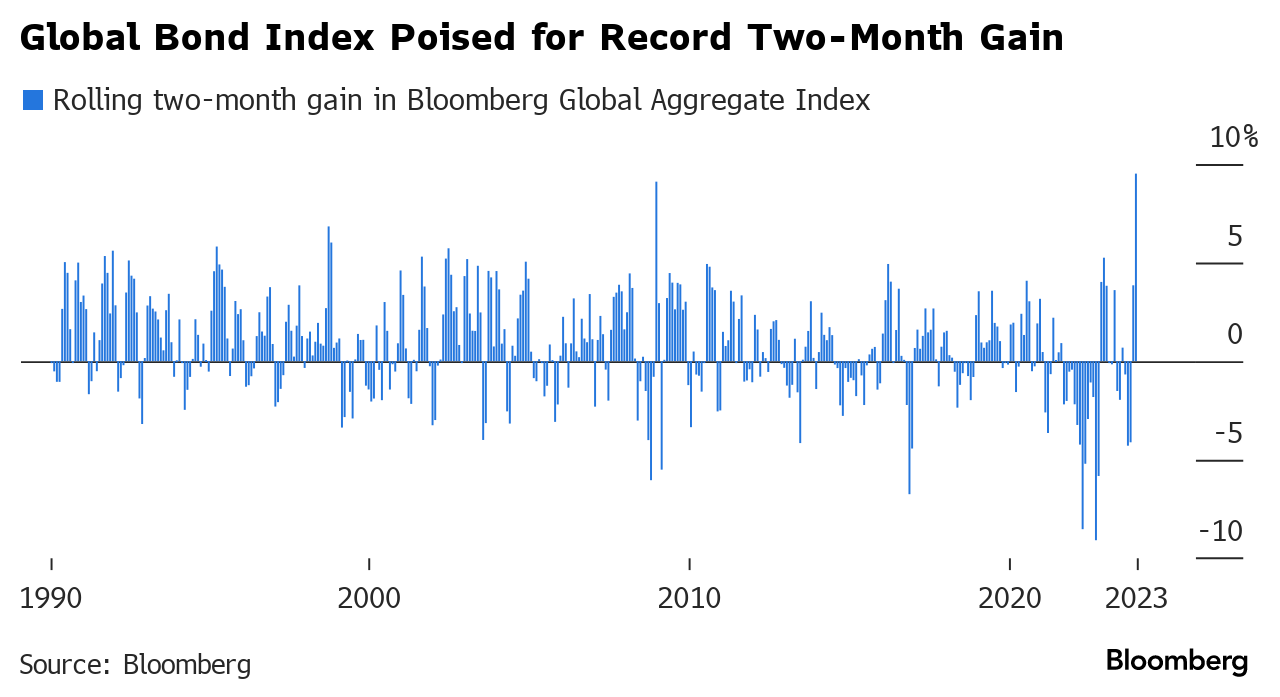

Bonds – Global bonds ended the year with the largest two-month gain in history…

{kind=link}

Source: Bloomberg

And that rally pulled the entire curve lower in yields on the year with the 5Y the biggest decliner, down 19bps on the year – after bloodbathing up around 100bps at its highs in October. Bear in mind that Fed Funds added 100bps this year and bond yields are all lower…

{kind=link}

Source: Bloomberg

Liquidity – stocks did what they do: follow the money. As macro data disappointed, stocks charged ahead on a re-emerging wave of global liquidity…

{kind=link}

Source: Bloomberg

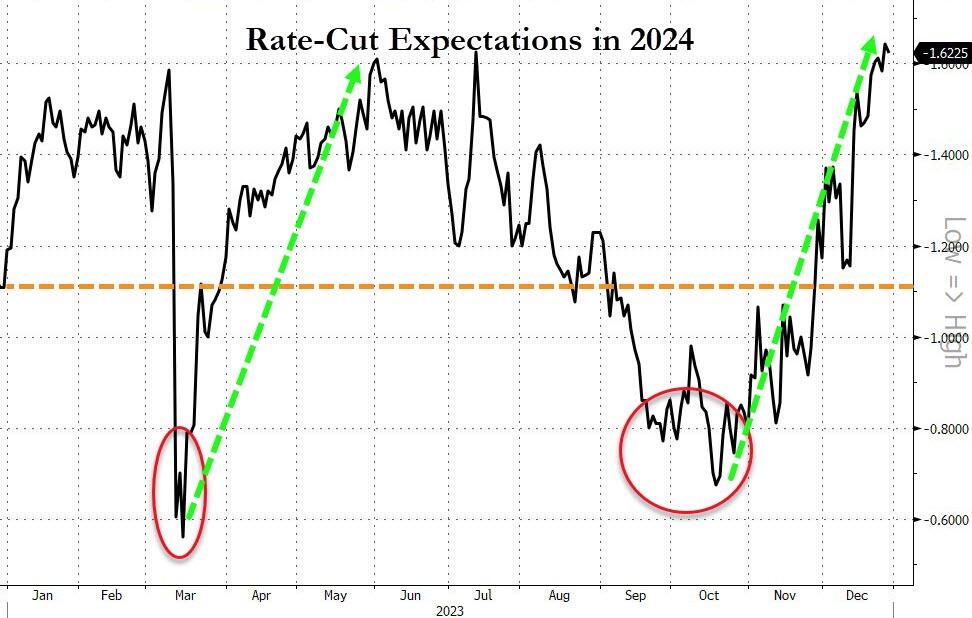

Rate-cuts– It was a very volatile, flip-floppy year for The Fed and Fed-watchers as rate-cut expectations swung wildly from 160bps to less than 60bps to more than 160bps to just 70bps and now back to highs above 160bps (more than 6 cuts, when The Fed ‘dots’ are calling for 3)…

{kind=link}

Source: Bloomberg

Additionally, the odds of a rate-cut as soon as March are now near 90% (up from less than 10% in September)…

{kind=link}

Source: Bloomberg

Financial Conditions – The rally in bonds, stocks, and credit – and collapse in the dollar – since The Fed signaled the end of hikes prompted the most aggressive easing of financial conditions ever. Financial conditions are now as easy as they were in May 2022 – when Fed Funds was 300bps below current levels…

{kind=link}

Source: Bloomberg

No Recession – expectations heading into 2023 was for a recession – it never came to pass on the backs of exponentially rising govt debt throughout the year and Fed jawboning that lifted macro data in the last month

{kind=link}

Source: Bloomberg

Cash Is King – Money-market funds saw their largest annual inflows ever…

{kind=link}

Source: Bloomberg

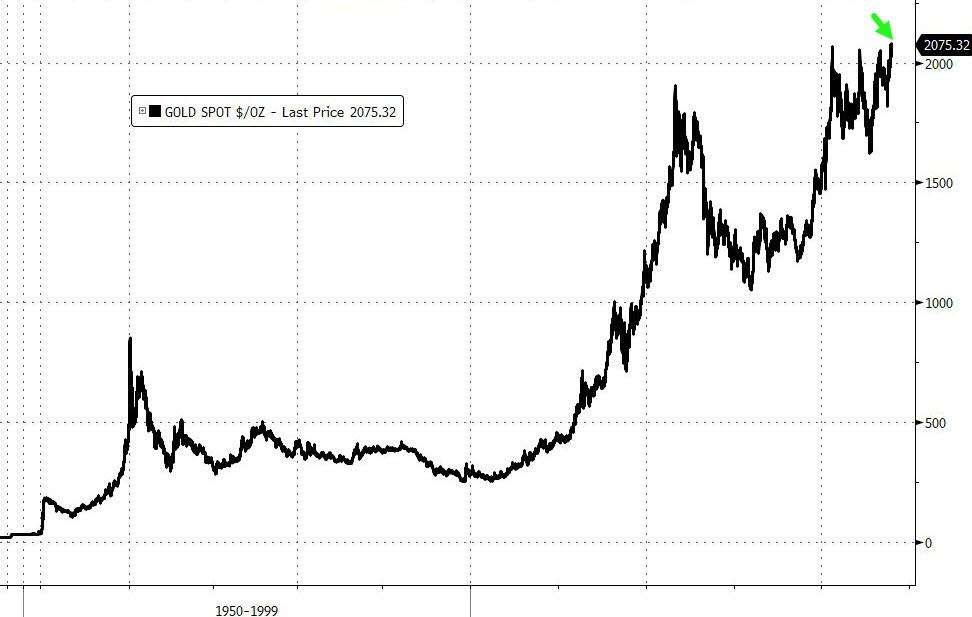

Gold – A weaker dollar, signals of loosening from The Fed, and a world on fire means no one should be surprised by gold’s great year, up almost 14% (best year since 2020) to a new all-time record high…

{kind=link}

Source: Bloomberg

* * *

Under the hood of the markets this year.

Equities

2023 ended on a down-note with all the US majors tumbling into the red for the week, erasing Santa Claus rally gains, but the afternoon saw dip-buyers return and rescue the weekly win-streak…

{kind=link}

Both ‘Most Shorted’ stocks and the MAG7 were also hit…

{kind=link}

{kind=link}

Source: Bloomberg

Tech and Consumer Discretionary dominated the performance this year with Staples and Utes the biggest losers (Energy was the other losing sector on the year)…

{kind=link}

Source: Bloomberg

Nvidia, Meta Platforms, and Royal Caribbean were the best-performing S&P 500 stocks in 2023 while FMC Corp, Enphase Energy, and Dollar General were the biggest losers…

{kind=link}

Source: Bloomberg

While VIX was smashed to an 11 handle at its lows of the year (multi-year lows), it notably decoupled from stocks in the last few weeks

{kind=link}

Source: Bloomberg

Small Caps outperformed Nasdaq in the first few months of the year, then the AI boom struck and Nasdaq exploded higher relative to Small Caps (as the latter was hit harder by soaring rates). The last month has seen dramatic outperformance of Small Caps, dragging the NDX/RTY ratio lower…

{kind=link}

Source: Bloomberg

But, overall, Nasdaq’s dramatic outperformance this year lifted it to a new record high relative to Small Caps… and then fell back (as Small Caps outperformed) to the dotcom highs…

{kind=link}

Source: Bloomberg

Bonds

Only the 2Y yield and earlier remain above 4.00%, but the curve is massively inverted from Fed Funds…

{kind=link}

Source: Bloomberg

After 2022’s massive flattening/inversion of the yield curve, 2023 saw 2s30s actually end steeper(the first steepening year since 2020). The yield curve de-inverted a few times during the year but was unable to sustain it…

{kind=link}

Source: Bloomberg

Real yields ended the year basically unchanged – after soaring to their highest since 2008 in October. Since then 10Y real yields have plummeted almost 100bps…

{kind=link}

Source: Bloomberg

If S&P 500 valuations are to be believed, the market is expecting negative real yields again soon enough…

{kind=link}

Source: Bloomberg

FX

The dollar ended lower against its fiat peers in 2023(BBDXY -2.9%) – its biggest drop since 2020 back to pre-COVID-spike levels…

{kind=link}

Source: Bloomberg

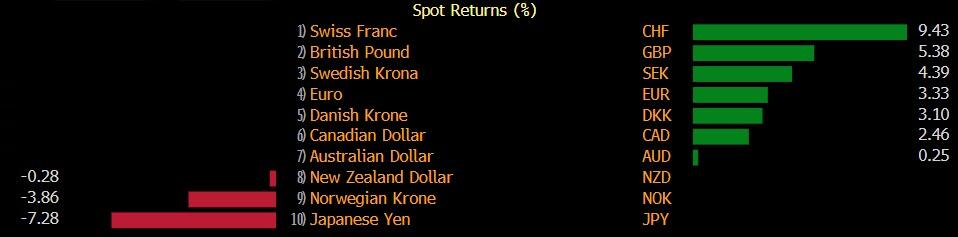

Swissy was the best performing currency(of the majors) against the dollar while Japan’s yen was the weakest.

{kind=link}

Source: Bloomberg

The Swiss Franc soared to its best year since 2010 and its highest since 2011 (in the middle of the EU crisis)…

{kind=link}

Source: Bloomberg

The Japanese Yen spent the first 10 months of 2023 plunging to its weakest against the dollar since 1990. Then as The Fed’s dovish pivot and BoJ’s hawkish jawboning picked up, the yen surged higher (finding support at Oct 2022 lows)…

{kind=link}

Source: Bloomberg

Emerging Market currencies plummeted to their weakest ever (on an indexed level) against the USdollar at the start of October, but the last two months have seen EM FX recover notably as The Fed pivoted…

{kind=link}

Source: Bloomberg

Cryptos

The big story of the year was the anticipation of a spot bitcoin ETF, and nowhere is that more clearly illustrated than in the collapse of the massive discount to NAV in GBTC…

{kind=link}

Source: Bloomberg

Bitcoin’s rally in 2023 erased all of the ‘existential’ crisis crash losses from 2022 (FTX/TerraUSD/3AC etc.), up to its highest level since April 2022…

{kind=link}

Source: Bloomberg

Ethereum did have a good year but only made it back to May 2022 highs…

{kind=link}

Source: Bloomberg

ETH underperformed BTC all year until the last week or so that saw ETH/BTC bounce significantly off June 2022 support…

{kind=link}

Source: Bloomberg

Commodities

The broad commodity landscape saw prices plunge in 2023 with Bloomberg’s Commodity Index down over 12% – its worst year since 2015…

{kind=link}

Source: Bloomberg

And that plunge in (growthy) commodities is in direct conflict with the large gains in (growthy) stocks.

Gold outperformed among the major commodities (best year since 2020 – after two unchanged years) while crude fell YoY for the first time since 2020. NatGas was clubbed like a baby seal to start the year and never recovered for its worst year since 2001…

{kind=link}

Source: Bloomberg

On an energy-equivalent basis, NatGas was systemically ‘cheap’ to WTI all yearafter the huge selloff in January…

{kind=link}

Source: Bloomberg

The big gains in gold over the last two months reversed the outperformance of oil in the prior quarter, bring the Oil-in-Gold ratio (how many oz of gold to buy a barrel of oil) back down to a key support level in recent years…

{kind=link}

Source: Bloomberg

And Finally…

If history rhymes, we can expect this buying-panic-gasm to continue into Q1 as it did in 2000…

{kind=link}

Source: Bloomberg

And if you want to know what the catalyst could be in March – it will be the next big banking crisis as The Fed is forced to shut down the BTFP (since it is spewing free-money via arbitrage).

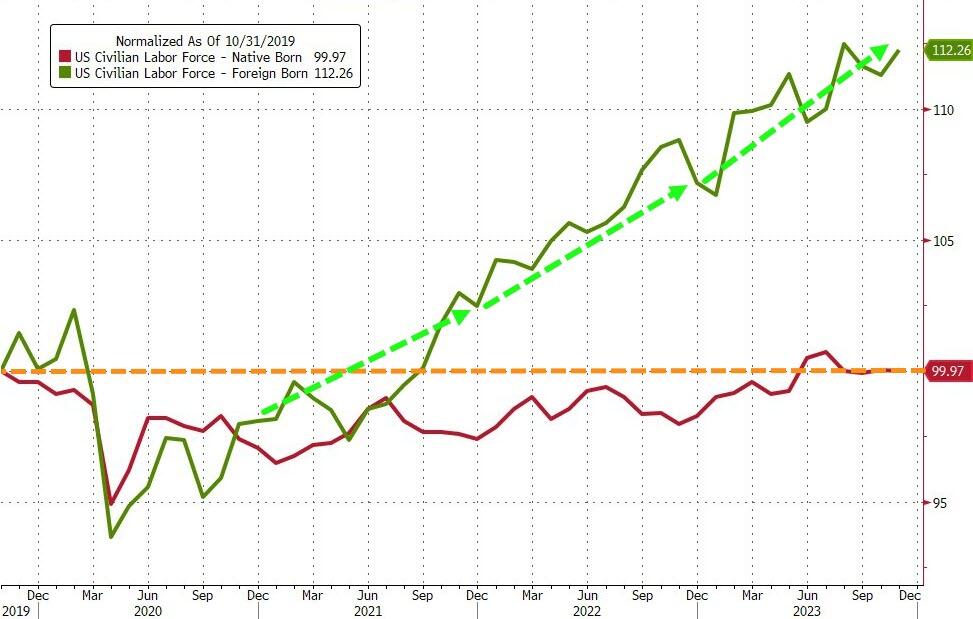

Politically, next year is a big one which makes it noteworthy that for the third year in a row, foreign-born workers dominated all job gains with the native-born American labor force basically unchanged since Biden’s election…

{kind=link}

Source: Bloomberg

This trend is not America’s friend…

{kind=link}

Source: Bloomberg

China and Russia are dumping Bonds and buying Bullion.

And the market is starting to sniff it out. 2023 saw the biggest rise in the market’s perception of USA’s sovereign credit risk since the Lehman crisis in 2008…

{kind=link}

Source: Bloomberg

Cloward, Piven, and Chomsky would be proud.

And on that note – happy new year!!

Tyler Durden

Fri, 12/29/2023 – 16:00